Checking vs. Savings Account: What should I choose?

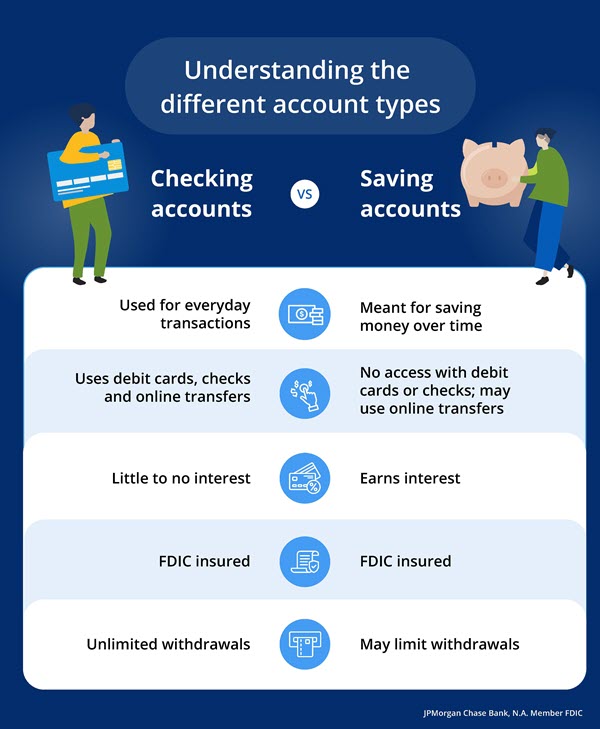

Checking accounts are held through a financial institution, like a bank or credit union, and are a place to deposit money, make transfers, write checks, withdraw cash, pay bills, and take care of other day-to-day banking transactions. In most cases, they earn little to no interest.

Savings accounts are ideal for depositing and saving money. These accounts typically earn interest that may help the account grow. Most savings accounts have either withdrawal limits, usually up to six per month, or associated fees when making a withdrawal, which can encourage you to save. Contact your financial institution for more information.

There are a number of differences between checking and savings accounts, as well as pros and cons to each, and understanding these features may help you determine which type of account is right for you.

Checking vs. savings account features

Before opening an account, it’s important to understand the difference between checking accounts and savings accounts.

Checking account benefits

The primary benefit of checking accounts is the ability to store money you intend on spending, either through debit card transactions, checks, or cash withdrawals. However, the downside is they typically don’t pay interest.

Typical checking account features include:

- Debit card

- Paper checks

- Direct deposit

- Overdraft protection

- Access to ATMs

- Online and mobile banking services, including bill pay, transfers, account alerts and mobile check deposit

A great benefit to having a checking account is that you can use it for paying bills or day-to-day purchases. You have access to your funds through a debit card or checks. Sometimes, you may even get a checking bonus for opening a new checking account with qualifying activities.

Potential downsides to most types of checking accounts can include:

- Usually does not earn interest

- Monthly service fees

- Overdraft fees

- Out-of-network ATM fees

- Foreign transaction fees

Benefits of a savings account

On the other hand, the primary benefit of a savings account is that you can use it to save money for emergencies or large purchases. You can also withdraw funds from a savings account for any reason, large or small.

Typical features of traditional savings accounts include:

- Earned interest

- Access to branches

- Direct deposit

- Online and mobile banking services, such as transfers, account alerts and mobile check deposit

Primary benefits for having a savings account include building an emergency fund and saving for a large purchase, like education, a vacation, vehicle or down payment for a house. Sometimes, you may even get a bonus for opening a new account, which can give you a great start on saving.

Potential downsides to savings accounts can include:

- Limits on the amount and frequency you withdraw from the account

- Monthly service fees

- Savings withdrawal limit fees

Contact your bank or credit union for more information on fees and limitations.

Checking account vs. savings account types

These are some of the most common types of checking accounts offered at banks and credit unions. They are not the only types of accounts available, but knowing the differences between each can help you know how to find the right one for you.

Traditional checking account

- Common type of checking account in which you use checks and a debit or ATM card to withdraw money or make transactions, and they typically offer online bill pay options

- Offered at most banks and credit unions

- May offer overdraft protection to help a payment or withdrawal be approved; by linking your savings account to your checking account for Overdraft Protection, your savings account funds will cover the transaction, if there are sufficient funds available

- Usually pay little or no interest on your balance

Premium checking account

- Typically earns or offers perks such as lower or no fees on safe deposit accounts, personal checks, official checks, money orders or out-of-network ATM fees

- Some banks offer additional perks, such as lower mortgage interest rates and financial guidance

- Most require a higher minimum balance

Interest-bearing checking account

- Earns interest on your account balance

- Most have requirements in order to earn interest, like a minimum account balance

- Potential fees include monthly service fees and overdraft fees

Online/checkless account

- Don’t offer checks, so transactions are made with a debit card

- Some traditional banks offer online-only accounts, though most are available through online banks that don’t have a physical location or branch, so all transactions are done online or over the phone

Rewards checking account

- Earn points or cash back on debit card purchases, though there are typically strict requirements you must meet

- Many of these accounts offer interest options

- May receive preferred interest rates on new loans or discounts on fees

There are primarily four types of savings accounts: traditional, money market and certificate of deposit.

Traditional savings account

- Earns interest

- Offers quick access to funds

- FDIC Insured (if the bank is a member)

- Can set up a direct deposit with your employer, use a debit card, withdraw cash from an ATM, pay bills online and send an electronic or wire transfer

Money market account

- Typically pay higher interest rates than regular savings accounts

- Have a higher balance requirement to avoid monthly fees

- Can come with a debit card or checkbook

- FDIC Insured (if the bank is a member)

Certificate of deposit (CD) account

- Offer fixed interest rates that can be higher than rates on other bank accounts

- Must agree not to withdraw the money for a certain amount of time, called a “term,” or pay early withdrawal fees

- Typically range six months to five years, and the longer the term, usually, the better the interest rate

- FDIC Insured (if the bank is a member)

What are the benefits of having both a checking and a savings account?

While you can have a checking and savings account separately — because each serves a different purpose — they can both be helpful for long term financial health and reaching your financial goals.

A great benefit of having both a checking and savings account, specifically with the same bank or financial institution, is that you can often manage both accounts through online banking and mobile apps, and transfer funds between accounts.