Get your credit score for free with Chase Credit Journey.

Meet Credit Journey®, a tool that shows you why your credit score changed and by how many points. Anywhere, anytime for free. No Chase account required.

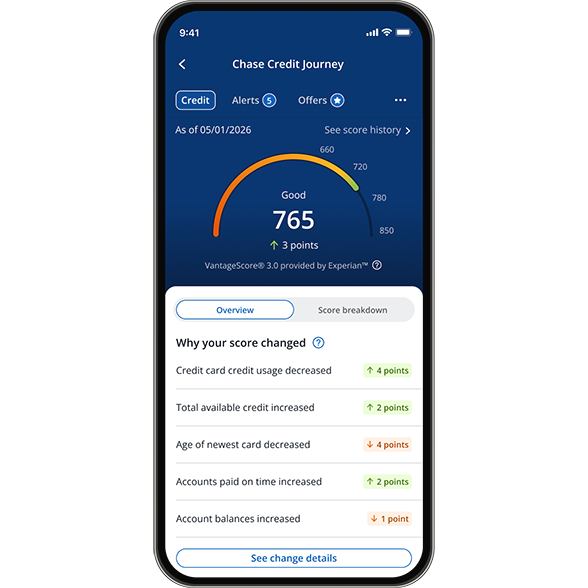

Find out why your score changed

A Chase Credit Journey® feature that shows you why your credit score changed and by how many points, exclusively available through Chase.

Get started with Credit Journey

Check your credit score

Monitor your credit score anytime without affecting it. Explore the credit score feature that helps you understand why your credit score went up or down and by how many points, exclusively provided by Experian™ for Chase Credit Journey.

Improve your score

Receive personalized plans from Experian™ to help enhance your score. Users who set and achieve their plan goal with Chase Credit Journey improve their score by an average of 35 points or more.

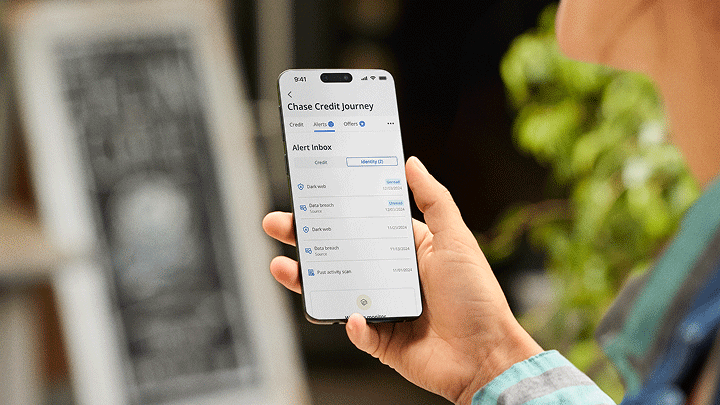

Get identity alerts

Receive alerts if your personal information is found on the dark web or involved in a data breach. If your information is stolen, we are ready to assist.

Start today without a Chase account

It’s so much more than just a credit score tool. With Credit Journey, you get customized plans from Experian™ made just for you on how you can help improve your score.

Know your score ahead of life’s big purchases

A good score can demonstrate financial responsibility to lenders. This means you may have a better chance of getting a lower interest rate from lenders and, in turn, lower monthly payments, when you’re ready to buy a car, home, or apply for a loan. See what your score is today.

Check your score from anywhere

Whether you’re on vacation or at home, if there are new updates to your credit usage and account status as well as any hard credit checks, Credit Journey will let you know.

Other products to help preserve your peace of mind

From creating a budget to getting alerts regarding your personal information, Chase has a variety of other tools to help you on your journey.

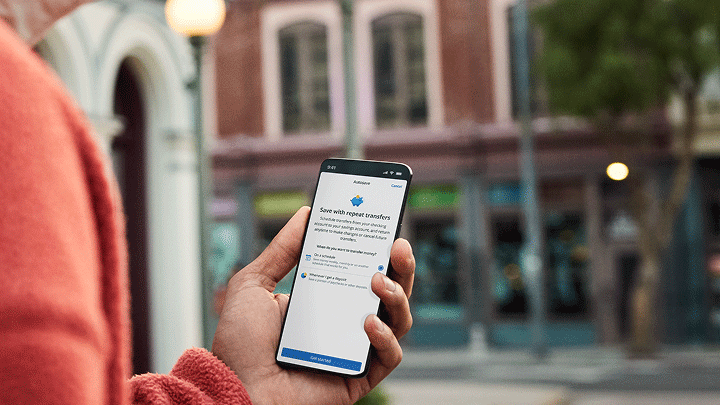

Autosave

Autosave let’s you automate transfers between your Chase checking and saving accounts. Whether you want to transfer money when your deposit hits or on a schedule, Autosave can help.

Identity monitoring

Identity monitoring provides alerts if your information is found on suspicious websites, is part of a data breach, or if there's activity associated with your social security number.

FAQs

Your credit score is a number that represents a snapshot in time of your credit history, which lenders use to help determine how likely you are to repay a loan in the future. In a typical scoring model, your score generally ranges from a low of 300 to a high of 850.

The higher the credit score, the better a borrower looks to potential lenders. There are different credit scoring models that may be used by lenders and insurers.

Credit Journey uses VantageScore® 3.0 by Experian™. Your lenders (including Chase) may not use VantageScore 3.0, so the score they evaluate may be different than the one you see in Credit Journey.

With Chase Credit Journey, you can see your VantageScore 3.0 credit score as often as you’d like with no impact to your credit. You can also receive your credit report directly.