Recasting for homebuyers

Selling your home doesn’t have to delay buying a new one.

Watch to learn what recasting can do for you.

Buying your dream home, but have a home you need to sell? With us, you don't have to wait.

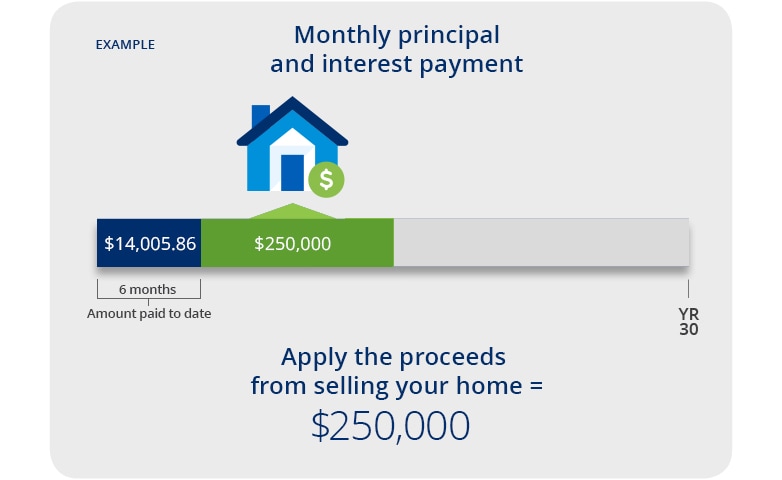

You may be able to take advantage of our mortgage recast service. This means that after you sell your current home, you can apply the proceeds to the new mortgage and we'll calculate your monthly payments based on the new balance.

We make it easy to start benefiting from a recast.

- No appraisal required

- No credit check

- Minimal paperwork

- Just more room in your monthly budget

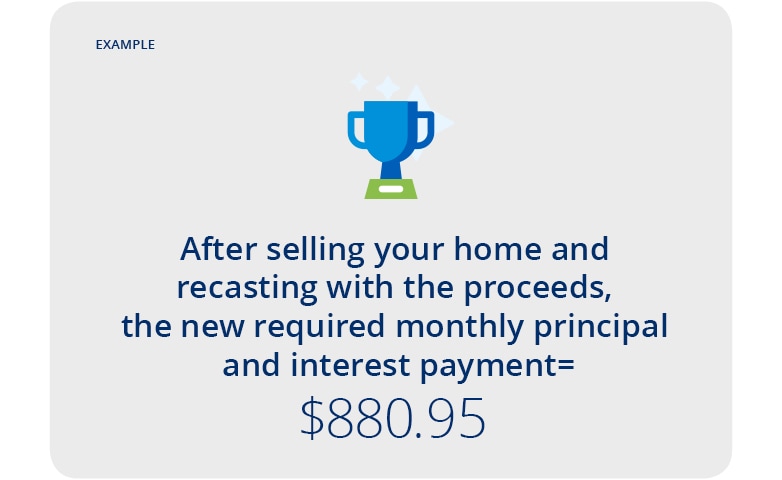

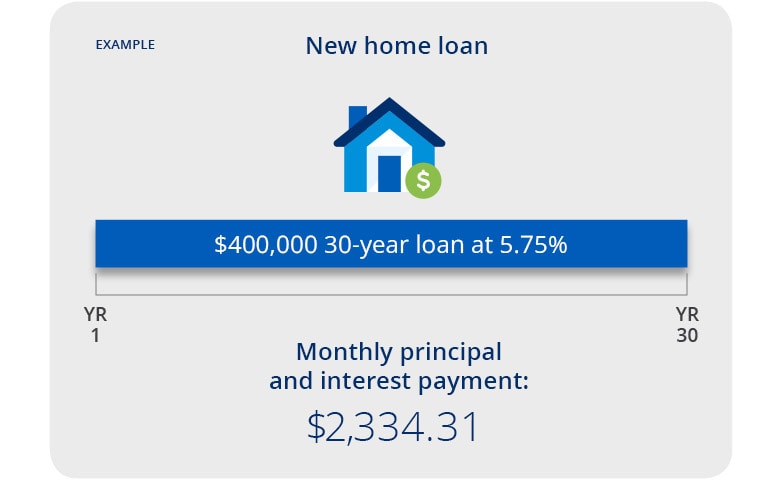

Mortgage recast in action

Answers to your most common questions

No, you will not be required to submit any documentation other than signing the recast agreement.

No, completing a recast on your loan will not require a credit check. However, your loan must be in good standing.

A mortgage recast does not increase the total interest planned when the loan was originated, but It does reduce or eliminate interest savings gained from making extra principal payments. The main benefit of a recast is lower monthly payments, not interest savings.

The principal and interest portion of your payment will remain the same. Your monthly payment could change based on changes to the escrow portion of your payment.

Yes. You can continue to pay additional principal payments at any time and pay your loan off early.

Yes, if you pay down the principal balance ahead of schedule, you could be eligible to recast your loan again.

No, there is no minimum amount required. However, a recast after a small principal reduction will not significantly lower your payment.

No. All loans are not eligible. FHA, VA and USDA loans are not eligible for a recast. The availability of a recast is based on investor guidelines and can change without notice.