Shop for homes with a Chase mortgage preapproval

Get a head start on homebuying.

A mortgage preapproval equips you with a digital letter to let you know the loan amount and interest rate you may qualify for — so you can shop for homes knowing what you could afford.

Although a mortgage preapproval is not a guarantee of a loan approval, having a preapproval letter shows sellers you're a serious buyer, and puts you a step ahead.

Apply for preapproval online in minutes

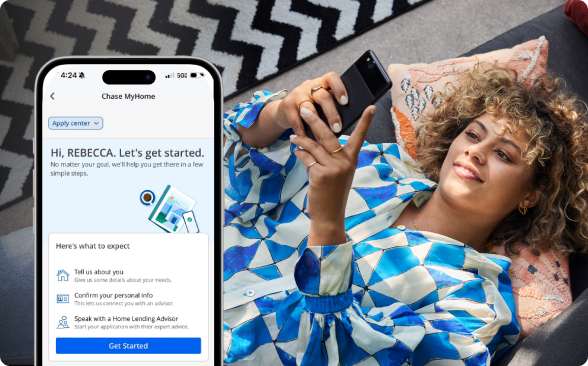

Step One

Answer a few questions about yourself, your mortgage needs and your finances, with no impact to your credit score.

Step Two

After you submit your preapproval, we’ll connect you with a Home Lending Advisor to discuss your customized preapproval, with no commitment necessary.

Step Three

Once you have your digital preapproval letter, you can start making offers with a competitive advantage.

We help make homeownership possible

- On time closing or get $5,000, if you qualify

- Rate discounts from .05% to 1%

- Down payments as low as 3%

- Homebuyer grants up to $5,000 in select areas, if you qualify

- On average, homebuyers save more in mortgage fees with Chase compared to a non bank

Mortgage preapproval FAQs

A mortgage preapproval is a document from a mortgage lender stating their preliminary willingness to lend a certain amount of money for a home loan. The document is typically based on criteria provided by the borrower and is not always a guaranteed offer or letter of approval.

While not required, a mortgage preapproval could potentially be a smart step to take before putting an offer on a home. Often, sellers require a buyer to provide a mortgage preapproval. It helps ensure that the buyer will likely obtain financing, and the seller doesn’t have to worry that the offer may fall through.

Since preapproval letters are only valid for one or two months, it’s recommended to obtain the preapproval prior to submitting an offer, but not too far out from when you plan to submit.

A mortgage preapproval typically lasts between 30 and 60 days, but may depend on the loan provider. Changes in the housing market or lender policies could also impact the duration of your preapproval. The general length is based on timely factors that affect mortgage loan terms, like changes in the borrower’s financial situation, interest rate fluctuations and real estate market conditions

These two terms are often used interchangeably. The main differences between a mortgage preapproval and a mortgage prequalification are:

- The purpose of each

- What you need to provide for each

- How much weight they hold in the mortgage application process

Both preapproval and prequalification offer the same result of being conditionally approved for a loan, with an estimate of what interest rate and loan amount you may qualify for. However, prequalification is usually a simple snapshot of your financial situation and potential borrowing ability, while a preapproval is an actual step toward securing a mortgage and is, therefore, more valuable to sellers.

Chase only offers mortgage preapproval, which is as close as you can get to establishing your creditworthiness prior to the purchase contract. It's a more detailed examination of your financial background, including a thorough check of your credit report, proof of income and assets.

A mortgage preapproval shouldn't change the status of your credit.