How to get to 9,000 on the S&P 500

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

By Kriti Gupta and NIck Roberts

Near all-time highs following a roughly 16% rally from the March pullback, the S&P 500 has staged a historic rally driven by an earnings supercycle and pricing in an artificial intelligence (AI) revolution. For investors who’ve enjoyed the returns, it’s natural to wonder: How much better can stock market returns get from here, especially with a bond market in tumult?

While not the base case, the S&P 500 could reach as high as 9,000 by mid-2027. An approximately 22% gain from current levels may seem optimistic but remains entirely plausible. Here’s how.

A bigger, broader AI supercycle

The AI revolution is already driving earnings growth – and by extension the stock market – at a record clip. There hasn’t been a streak of six consecutive quarters of double-digit earnings growth since the aftermath of the global financial crisis (GFC).

Global earnings growth is booming, accelerating from 15.3% year-over-year in the fourth quarter of 2025 to 22.6% in the first quarter of this year. That’s the highest in over four years. This is an impressive showing but even more extraordinary given it’s not a rebound from a cyclical downturn like after the GFC, but rather an acceleration from an already high base.

For now, it’s being driven by the tech sector. That’s both a concentration risk and an opportunity. The path to 9,000 extends beyond the tech sector. It relies on broader AI adoption across sectors that increases productivity and bolsters margins across the board.

It’s no secret that the macro narrative in the United States centers on AI. But the market is now transitioning its focus from infrastructure to adoption. While the hardware layer continues to print extraordinary profits, the secular earnings story is moving downstream.

The largest cloud giants are deploying over $800 billion in AI capital spending annually, scaling to an estimated $1.16 trillion by 2027. This acts as a massive fiscal stimulus for the private sector, flowing directly into semiconductors, specialized hardware, advanced cooling, power grids and commercial construction, among other adjacent areas.

For companies to sustain midteens earnings growth without igniting inflation, productivity growth needs to accelerate. We’ve seen it before. Productivity boomed in the late ‘90s, annualizing around 2.8%. Meanwhile, the index delivered five consecutive years of over 20% returns between 1995 and 2000. It can happen again.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Digesting a bond market selloff

What gets in the way? The narrative feels unstoppable, but in any bull case, it’s prudent to entertain the risks – especially ones that come from other asset classes. While the Federal Reserve is most likely to take a wait-and-see approach to energy-led increases in headline inflation, the bond market isn’t always as patient.

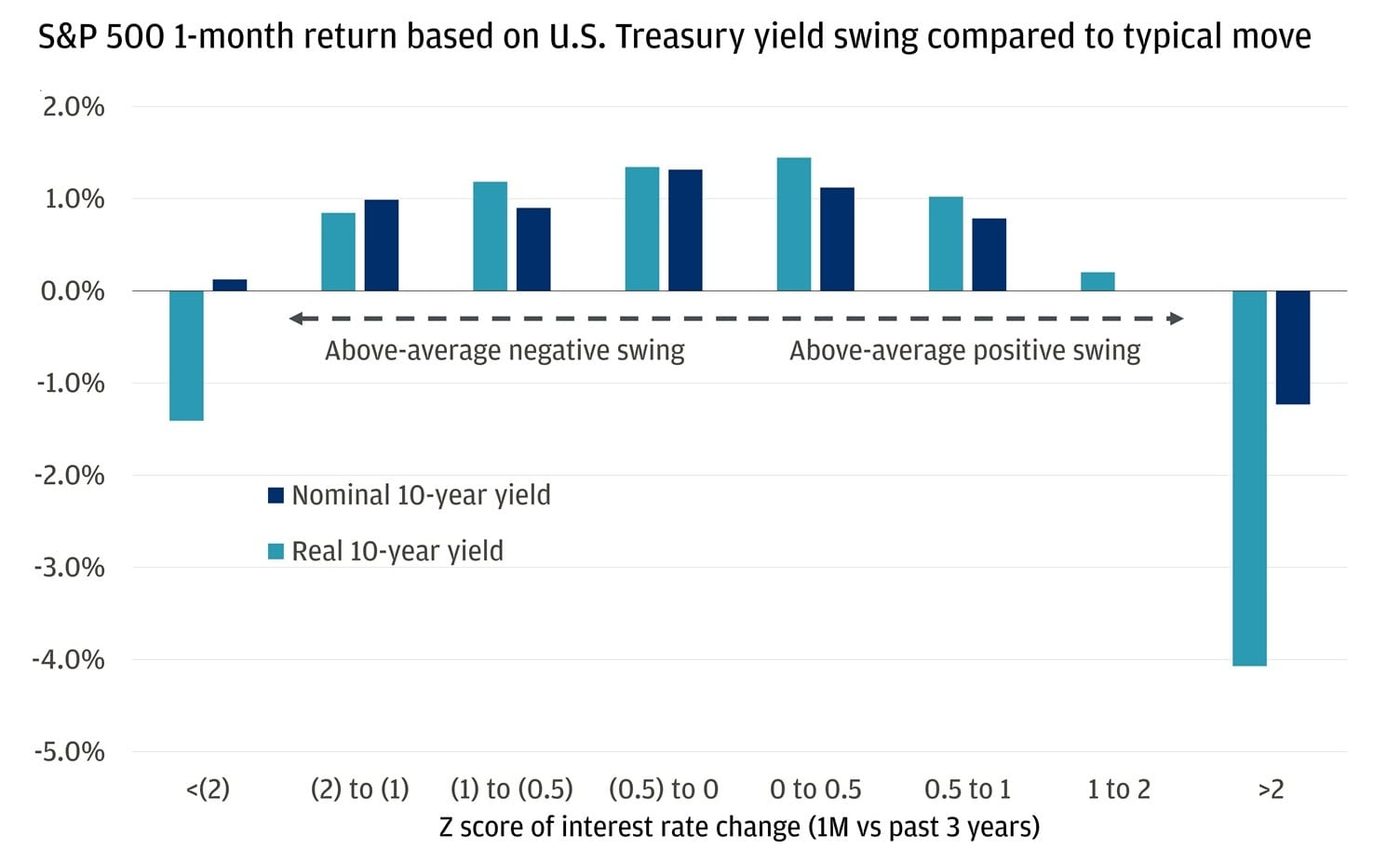

U.S. 10-year yields rose by over 40 basis points over the last four weeks. Across the Atlantic, U.K. gilt yields, German bunds and Japanese government bonds (JGBs) experienced similar moves around the same time frames driven by a repricing of central bank policy expectations.

Naturally, the rise in bond yields has spooked equity markets. Investors are asking one key question: Can a stock market near all-time highs digest a level of rates that in some parts of the yield curve was last seen in 2007?

It’s not the level of rates itself but the magnitude of the move that matters more. An over 40 basis point move in 10-year Treasury yields isn’t uncommon. Similar moves of this margin have happened six times in the past five years, notably in the wake of Liberation Day and after the 2024 U.S. presidential election. But this broad-based selloff in rates hasn’t happened in over a year. Perhaps that’s why the move feels so acute this time around in equities.

Stocks tend to fall when rates move more than average

Risk assets do not always go up in a straight line. The current unwind in momentum stocks like semiconductors and other AI bottleneck trades in reaction to higher bond yields is entirely healthy. It sets the stage for the next leg up, with cleaner investor positioning.

Equities can digest higher yields if the move is driven by higher nominal growth expectations. Take Japan as an example. The current rally in Japanese stocks is taking place despite a major selloff in JGBs. On the other hand, higher bond volatility and a rapid repricing predicated on inflationary concerns could be more troubling. And that line is what the U.S. market is grappling with as the timeline shifts around a resolution to the conflict in Iran.

Hormuz hangover

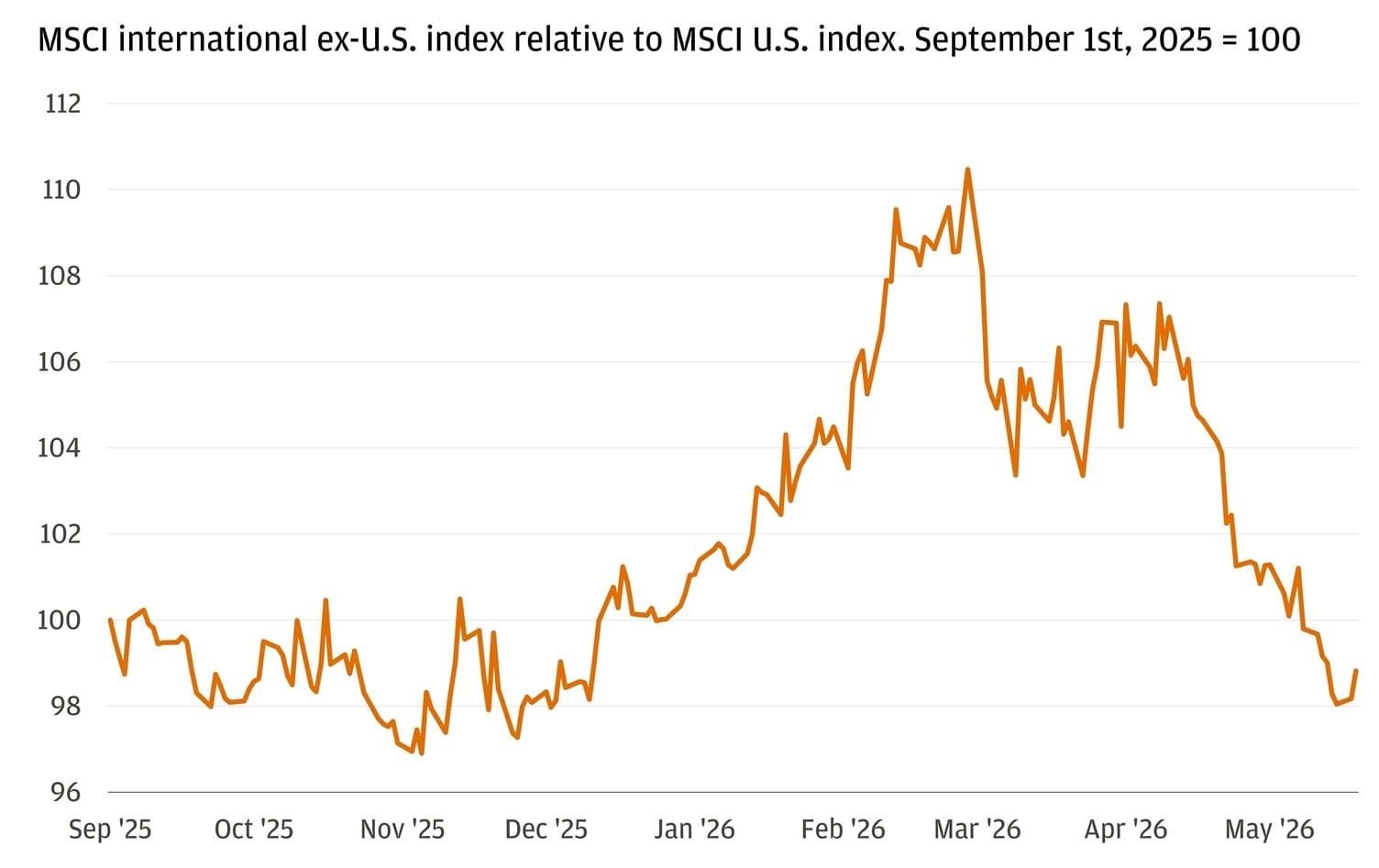

Nearly halfway through the year, global equity drivers look vastly different compared to when the year started. 2026 began with investors flocking to international markets. U.S. stocks, although rallying, were underperforming their global counterparts.

Positive global growth signals – including strong U.S. economic data, fears of lofty mega-cap tech valuations in the United States, a series of AI-related disruptions and multiple geopolitical events from Venezuela to Greenland fed the dynamic. But the conflict in Iran bucked the trend.

Suddenly, the world was awash with uncertainty and an energy shock that for some parts of the world rivaled the one seen in 2022 after the war in Ukraine began. And American stocks were back in the driver’s seat, especially as the length of the conflict and blockade in the Strait of Hormuz extends.

A return to normal around the Strait of Hormuz that returns over 14 million barrels of oil per day to the global economy could – in theory – reverse the effect, at least temporarily. In other words, in the short term, the regions that have suffered most from higher energy costs and a negative terms-of-trade shock (like Europe or Japan, where the energy hit has been the hardest and the rates repricing the most aggressive) could see a boost.

International equities’ outperformance has unwound

All market and economic data as of 05/21/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank