The U.S.-China relationship: A new equilibrium

Global Investment Strategist

The United States-China summit is not about a reset. It is about whether the world’s two largest economies can make a fragile relationship more manageable. Leader-level engagement of this kind has been rare – the last U.S. presidential visit to China was in 2017 – and since then the relationship has been marked by on-and-off confrontation, decoupling pressure and the pursuit of economic leverage.

As trade flows have declined and supply chains have shifted, both sides have become more willing to test each other’s vulnerabilities. But the links remain large enough that unmanaged escalation would still matter for growth, inflation, supply chains and markets.

The key question is what a new U.S.-China equilibrium looks like. Engagement for the sake of engagement brings few benefits. Even during the Cold War, rivals cooperated when the cost of no cooperation was too high. For markets, less policy uncertainty would be a constructive signal – especially for global trade, China and broader emerging markets.

Here are five forces we think will shape that equilibrium.

1. The relationship has been damaged, but not replaced

The U.S.-China trade link has weakened, but it has not disappeared. U.S. goods exports to China fell 25.8% in 2025, while U.S. goods imports from China fell 29.7%. Even so, bilateral goods trade still totaled $414.7 billion last year, including $308.4 billion of U.S. imports from China and $106.3 billion of U.S. exports to China.

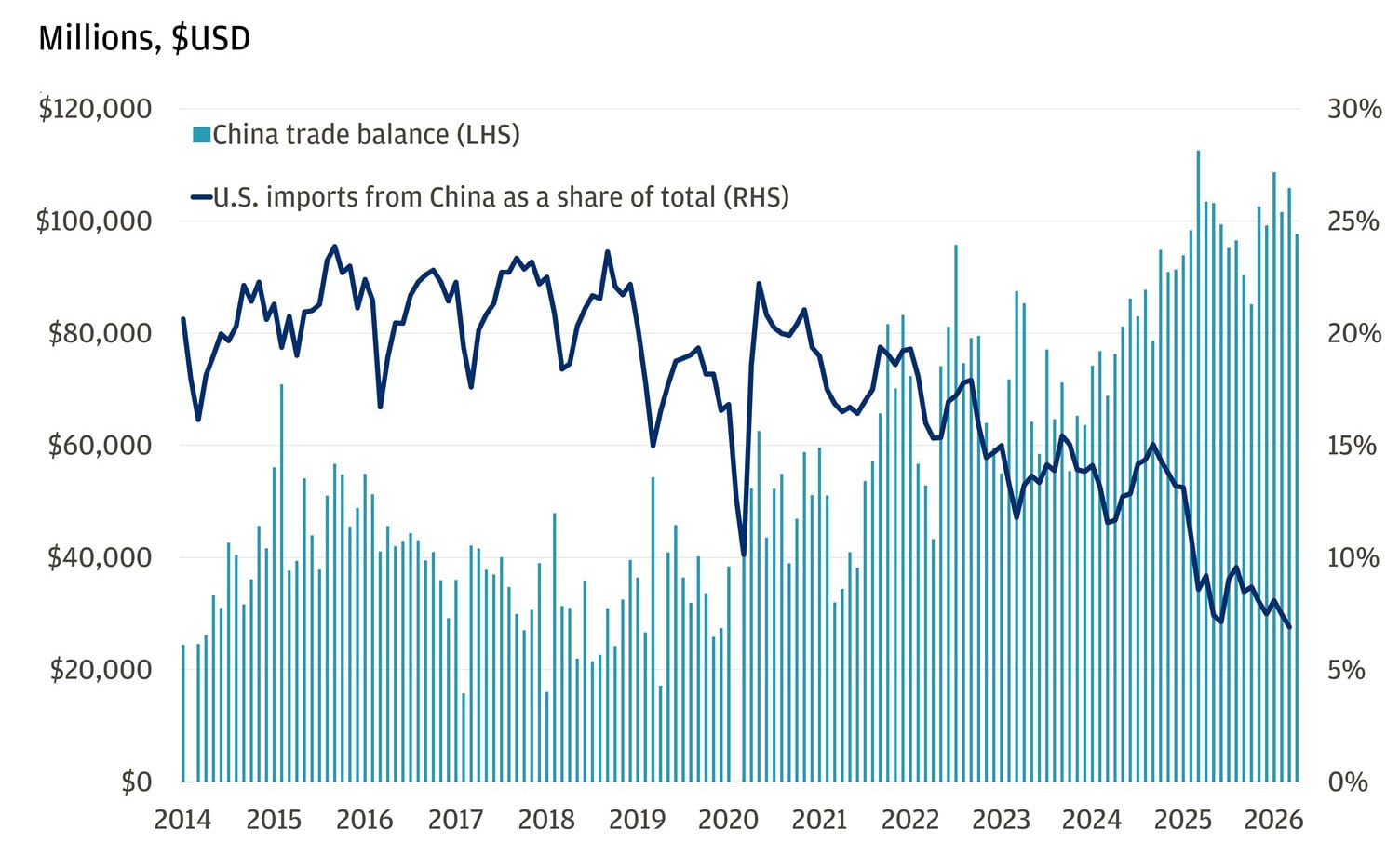

China is as trade dependent as ever… just not on the U.S.

China is still trade-dependent – just less U.S.-dependent. U.S. imports from China have fallen as a share of total imports, but China’s overall trade balance remains historically large. Decoupling is occurring, but there is likely significant trade rerouting through other markets.

2. The chokepoints now run both ways

Tariffs are the most visible pressure point. Average U.S. effective tariffs on Chinese exports have risen to about 24%, while China’s average effective tariffs on U.S. exports stand at roughly 32%. Both now cover essentially all bilateral goods trade.

But tariffs are only one part of the leverage map. The U.S. can pressure China through the dollar-based financial system, semiconductor export controls and investment restrictions. China has its own pressure points: rare earths, manufacturing supply chains, market access and purchases of U.S. goods.

The rare-earth supply chain is especially important. China accounts for roughly 70% of rare-earth mining, 90% of separation and processing and 93% of magnet manufacturing, according to the Center for Strategic and International Studies (CSIS). For magnet rare earths specifically, the International Energy Agency (IEA) notes that China exported enough rare-earth magnets in 2024 to support components for millions of cars, industrial motors or aircraft – or thousands of strategic military systems, data centers or wind turbines. That concentration turns critical minerals into a macro issue, not just a supply-chain footnote.

Both sides now know the pressure points. The goal is to manage them before they become shocks.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

3. The Taiwan issue remains central to the relationship

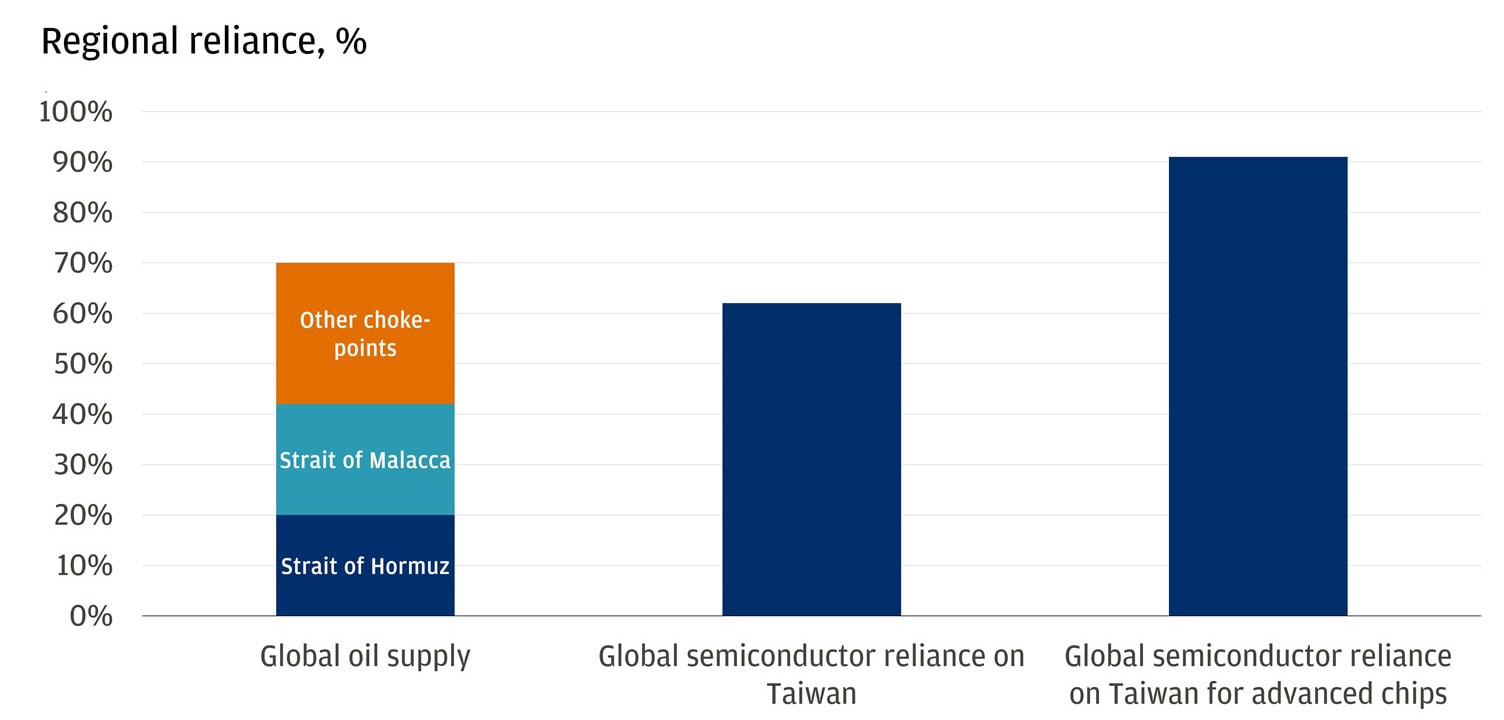

Taiwan remains the structural flashpoint in U.S.-China relations, especially because it sits at the intersection of security, technology and semiconductor supply chains. The issue remains a central focus for China – it’s no surprise the meeting kicked off with a stern statement from the Chinese leader. The economic stakes are large on both sides: One estimate suggests a Taiwan blockade could reduce U.S. gross domestic product (GDP) by 5% and China’s GDP by 9%. That underscores why neither side benefits from an unmanaged crisis.

Iran is the near-term complication. China buys more than 80% of Iran’s shipped oil, according to Kpler data. In other words, Iran is an energy-security issue for China and an inflation-risk issue for global markets – in the U.S., gas prices spiked 20% in the month of March.

Oil and semiconductor trade is reliant on chokepoints

Economic stabilization can still occur even when geopolitical issues remain unresolved.

4. The relationship is global, not just bilateral

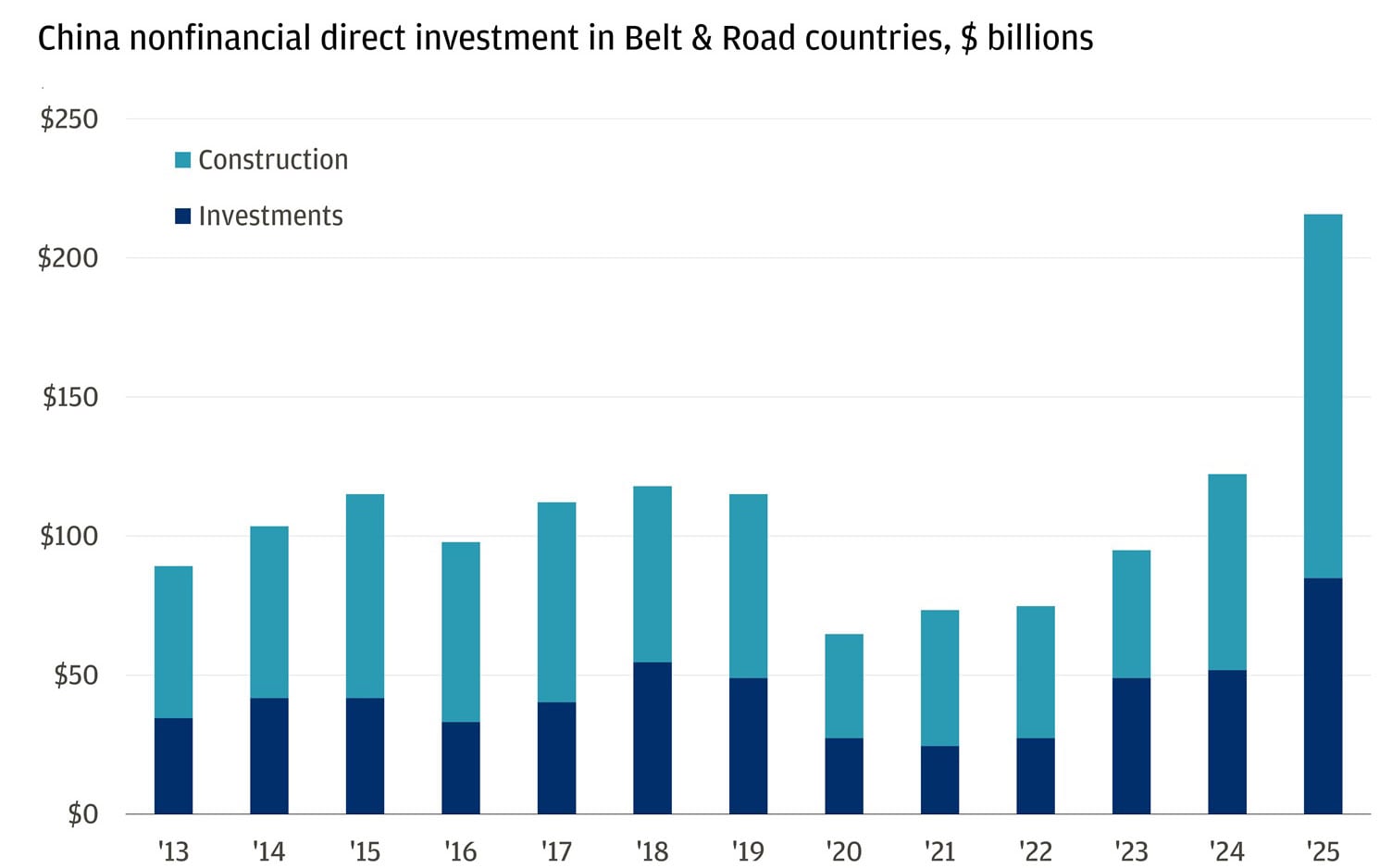

U.S.-China tensions no longer stop at the bilateral trade channel. China’s Belt and Road Initiative spans roughly 150 countries, giving Beijing a broad platform for trade, infrastructure and influence across emerging markets. Recent activity underscores the scale: Chinese engagement across Belt and Road countries reached record levels in 2025, including $128.4 billion in construction contracts and $85.2 billion in investment.

The largest year of Belt and Road investment yet?

The U.S. is responding through its own strategic lens. The competition is increasingly about infrastructure, supply chains, commodities, technology standards and strategic alignment. For many countries, the challenge is not choosing one side on every issue; it is managing the costs of operating in a more fragmented global system, where investment, trade access and security relationships are increasingly linked.

The U.S.-China equilibrium will be felt well beyond the U.S. and China.

5. A dialogue could signal stabilization

This is not the last time the presidents of the U.S. and China could meet. There are several potential touchpoints that could take place over the next year. That makes the latest summit less of a one-off and more of a prelude to prolonging détente. It’s less about the dialogue and more about whether future engagement produces mechanisms to help manage disputes on things like trade and investment channels, purchase commitments, artificial intelligence (AI) dialogue, tariff language and working-level forum.

That’s the key to reducing the risk of economic frictions becoming broader disruptions.

For markets, the constructive signal is lower uncertainty. Fewer chances of abrupt policy shocks could support sentiment toward global trade, China and broader emerging markets – especially as fragmentation and AI remain key drivers of the broader investment landscape. Dialogue does not mean a reset, but rather a test of whether the world’s two largest economies can make a fragile relationship more predictable.

All market and economic data as of 05/15/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist