The global rates repricing: will central banks actually hike?

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

By Kriti Gupta and Alex Wolf

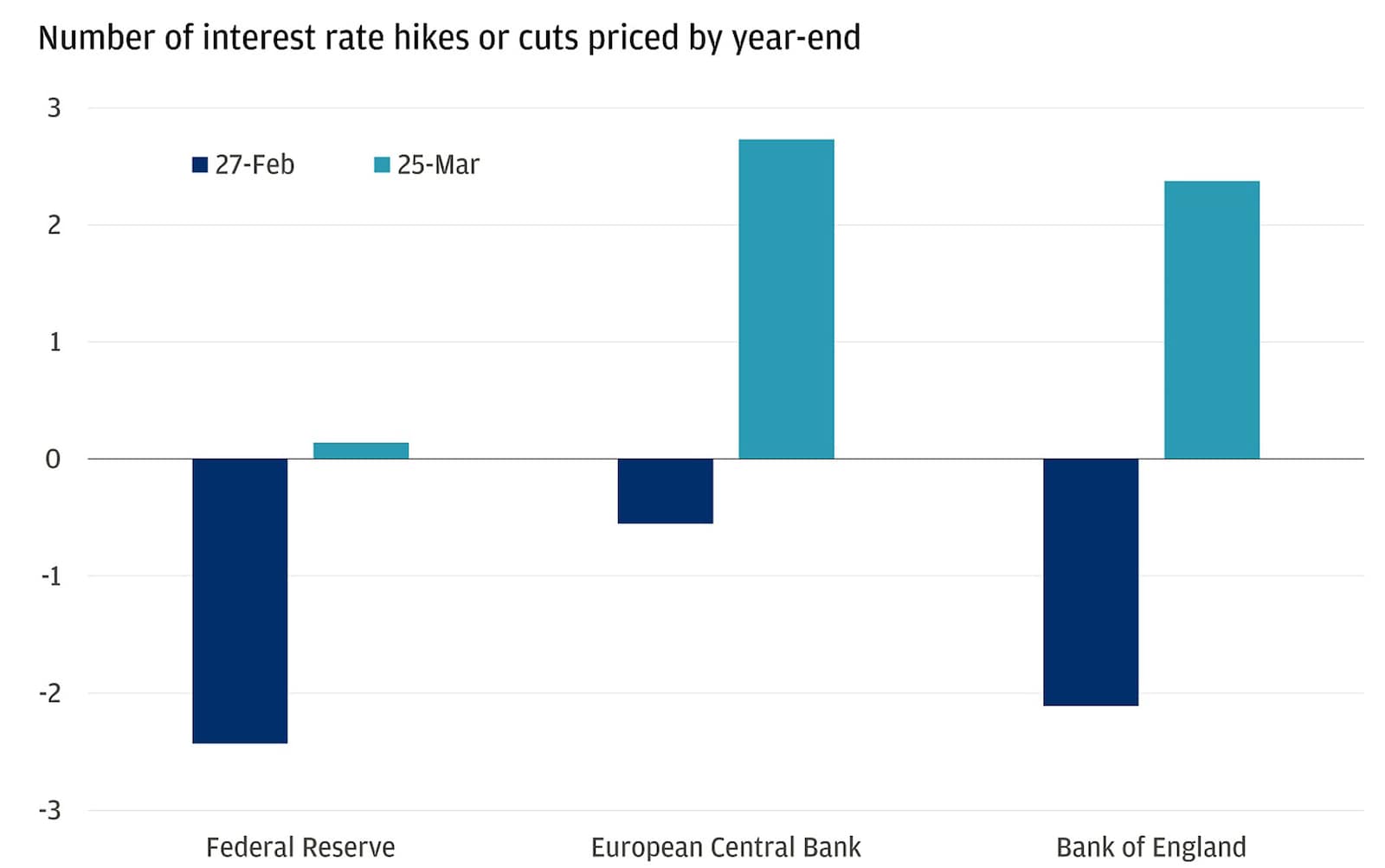

A surge in oil and natural gas prices around the world has invoked a rapid repricing in the global rates market. In what feels like a sudden and knee-jerk reaction to not-so-distant memories of 2022, investors are not only no longer expecting rate cuts from the Federal Reserve in 2026, but they are going as far as expecting a rate hike by the end of the year. Rest assured; this seems unlikely.

With an inflation-focused mandate and a high level of exposure to energy prices, European central banks are battling a different dynamic. But when it comes to the Federal Reserve, a sustained higher oil price would likely lead to a prolonged hold on interest rates, but not a hike. If energy prices climb to the point of becoming a recessionary risk, the Fed would more likely tilt toward its labor mandate. That means rate cuts in the extreme scenario. We are not there yet.

In short, rates curves are pricing a monetary policy response that is unlikely to come to fruition.

The global rates repricing

So, what would it take for the Federal Reserve to hike? The bar is high.

Markets are pricing in the possibility that the energy price shock could be more prolonged, given the recent escalation and significant damage done to natural gas and other energy infrastructure. With inflationary effects likely to be felt throughout the summer from recent gas and oil price hikes alone, and futures repricing higher, it is rational to see rate curves shifting.

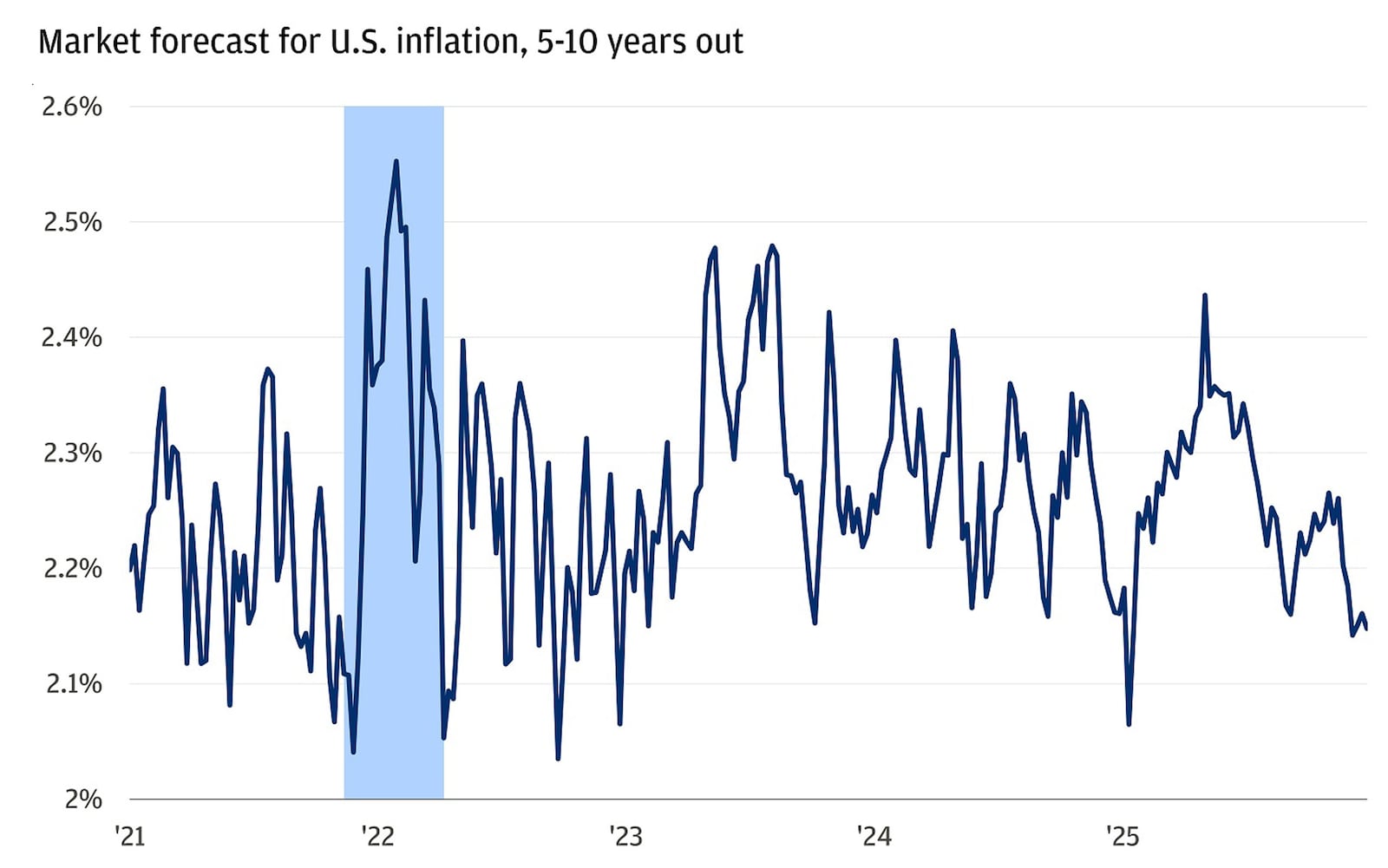

But the key lies in inflation expectations. If investors start believing prices will be higher in 5 to 10 years by a larger margin than the Federal Reserve’s long-term target of 2%, it could prompt action. After all, the paradox of expecting higher prices can inadvertently lead to a higher tolerance – and ultimately higher prices themselves. It’s a feedback loop that can quickly spiral. So far, there is no such evidence. And without that nudge, the Fed is far more likely to hold.

Future inflation expectations are below the 2022 spike

There is also very little precedent for the Federal Reserve to raise interest rates in the face of an oil shock. Historically, the central bank has done the opposite. The rate-hiking cycle of 2022 marks a notable exception as supply chain shocks, the war in Ukraine and government stimulus sent inflation well above 9%.

A similar fiscal policy response could raise the risk of an interest rate hike. But low appetite to fund stimulus from the federal budget from both the long end of the bond market and deficit hawks in Congress makes that unlikely.

As a consequence, the most significant repricing of the curve has been on the front end, which now offers the best starting yield since 2023. If the hawkish pricing reverts as a function of de-escalation or more economic certainty, the front end of the curve would also capture price appreciation.

Short-term yields: most attractive since 2023

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

The value of duration in Europe

Across the Atlantic, it’s a slightly different story. To illustrate just how large the repricing was, take the Bank of England. In a span of a few days, investors went from pricing in two rate cuts to over three rate hikes. In response to surging commodity prices, European and UK bond yields are trading near levels last seen in 2023 when global inflation was running near 10%.

It was also when central banks were aggressively hiking rates in an attempt to bring down those prices. To avoid a sense of 2022 déjà vu, both the European Central Bank and the Bank of England are likely to respond given their single inflation-focused mandate.

In a more severe scenario where recession risks rise from a prolonged conflict, having exposure to duration could offer some portfolio protection. But it also benefits in a de-escalatory scenario, which is still the most likely outcome.

By extension, that means energy prices would ultimately trend lower, and commodities markets would eventually return to the oversupplied status that they began the year with. As the rates market in Europe digests the developments, yields are already providing some compensation. And as an inevitable relief rally or a more extreme but unlikely recessionary scenario ensues, yields can be locked in at a higher level.

All market and economic data as of 03/27/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank