If oil backs off, risk reprices

As the conflict in Iran evolves, it’s worth considering the different channels through which sustained higher oil prices can ripple through the economy. The most immediate effects have been well telegraphed: higher prices at the pump, pressure on consumer spending and rising manufacturing costs. The magnitude of the impact ultimately comes down to duration – the higher the oil price, and the longer it stays there, the more persistent the inflationary impulse becomes.

There is, however, a less discussed scenario. If the conflict in Iran is resolved within months – as current market pricing assumes – how quickly do risk assets resume their upward march?

The key

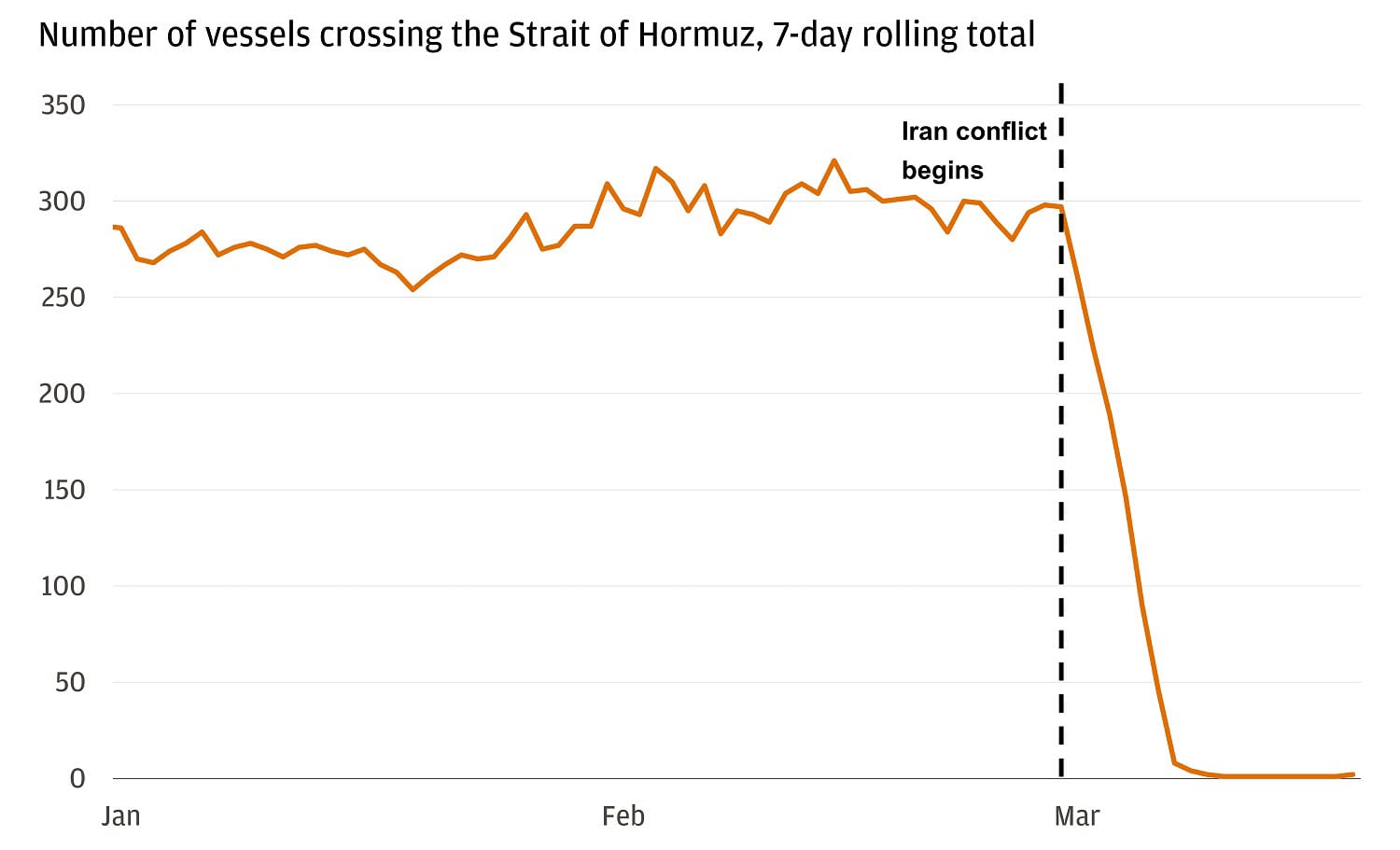

As the conflict remains ongoing, it’s challenging to map out what the future of Iran and the region looks like. But from an economic point of view, what matters most is the Strait of Hormuz. One-fifth of the world’s oil flows through the strait, making it a central flashpoint in the war. Reopening it would unlock lower oil prices, relief in the equity markets and reduced inflation expectations.

Traffic through the Strait of Hormuz has collapsed

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Limited sell-off

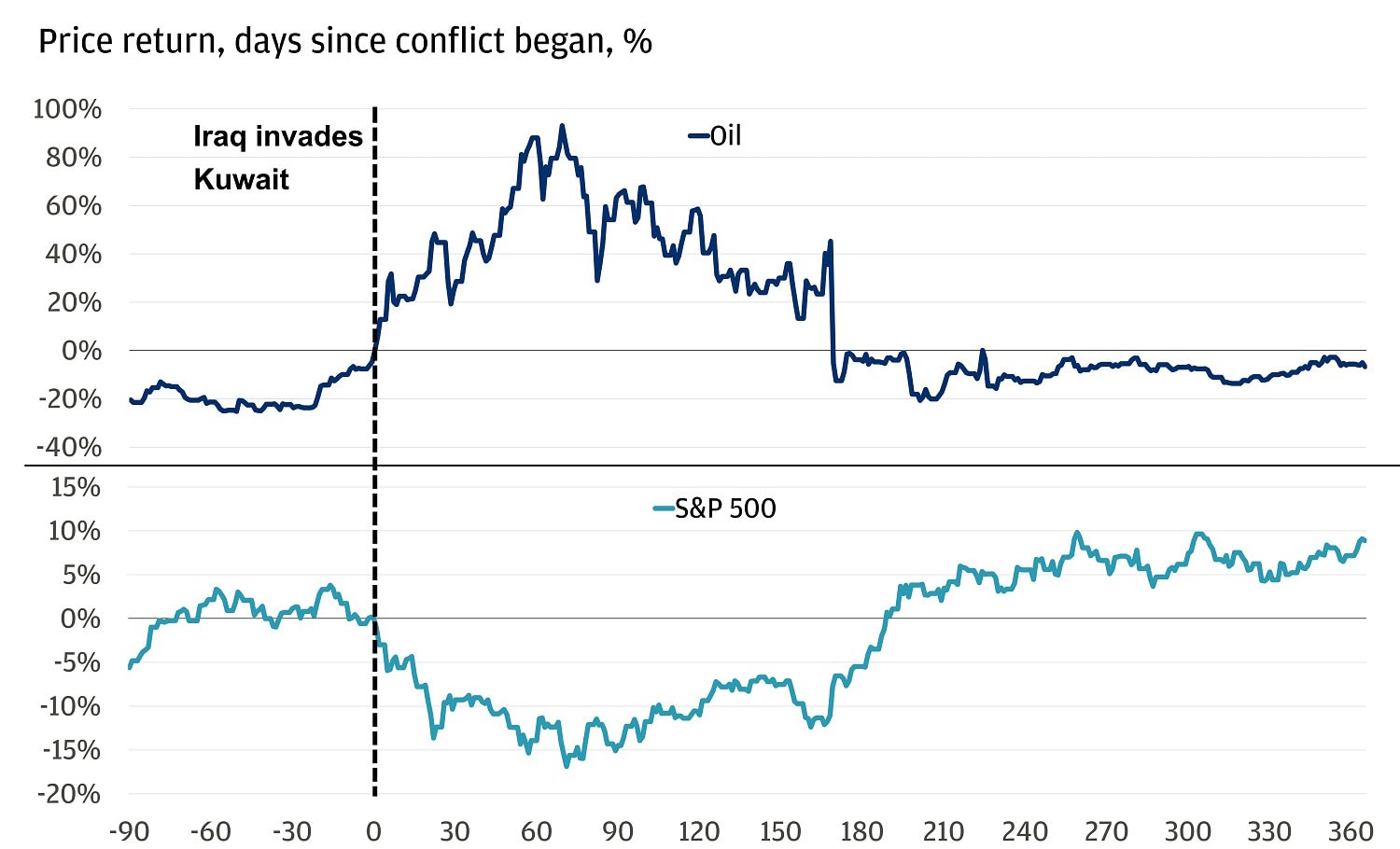

It’s no secret that equity markets tend to sell off in the face of oil spikes, driven by worries around higher input costs and demand destruction. It happened during the Gulf War of 1990-1991 and the war in Ukraine in 2022, both of which saw an oil spike lasting months and are perhaps the most convincing parallels to the conflict in Iran.

In 1990, the S&P 500 dropped over 15% sharply after the start of the Gulf War, but recovered as oil prices normalized. In 2022, a similar story. Equities sold off as crude surged 32%, but the market was ultimately shaped more by the supply chain-driven inflation shock and over 400 basis points of rate hikes from the Federal Reserve than by energy alone.

In the Gulf War, equities rallied when the oil spike faded

Past performance is not a guarantee of future results. It is not possible to invest directly in an index.

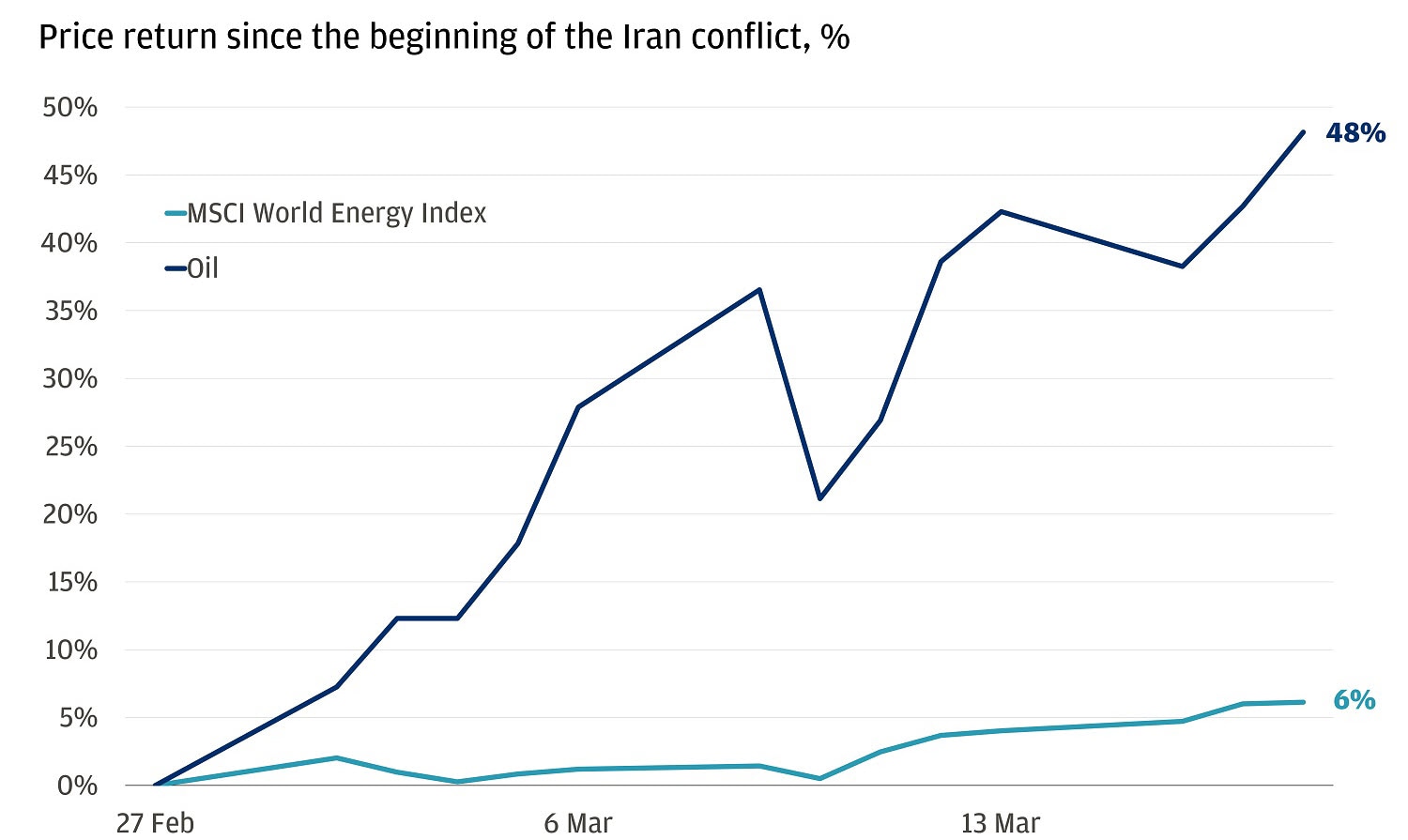

Whereas oil prices have risen over 40%, energy stocks around the world have risen only about 8%. That indicates that equity investors eyeing the sector may not be expecting significant changes to revenue streams over the long term. Given the energy sector is less than 4% of the index, any oil price readthrough doesn’t uplift enough of the benchmark. Compared to past oil-shock-related sell-offs, the current response seems mild on the surface.

Oil prices haven’t led to major gains in the energy sector

Past performance is not a guarantee of future results. It is not possible to invest directly in an index.

So, why does this time feel different?

For starters, the United States is largely viewed as energy independent and less affected by the supply shock than its international counterparts. Most of its oil imports come from its neighbors, Canada and Mexico. That isn’t true for most other countries in the world who feel the effects of the conflict more acutely. Europe and Asia, for example, get their energy supply from countries like Saudi Arabia and Qatar in addition to the U.S.

So far, that means European and emerging markets are selling off by a bigger margin. Since the conflict in Iran began, the S&P 500 has dropped about 4%, with international equity markets selling off roughly 8%. It marks a contrast to the start of the year when international equities were in the driver’s seat, encouraged by indications of global growth and risk appetite.

Now, add into the mix additional attacks on natural gas infrastructure like the world’s largest liquified natural gas plant in Qatar. Infrastructure like that could take longer to recover from even if the Strait of Hormuz were to reopen and energy flows were to resume.

If European assets are impacted most acutely, it stands to reason that when the conflict ends, Europe is poised to benefit the most, but prolonged issues like the attacks in Qatar further delays recovery time.

It’s a similar nuance in Latin America where crude exporters like Brazil and Mexico tend to benefit from stronger oil revenues, but the region has limited refining capacity. And through fiscal assistance, governments also face the cost of shielding consumers from increasing prices at the pump. That means any extra oil-related income, ultimately, leaks out.

Alongside Asian economies who are also largely oil-importing nations, this sets up emerging markets as the beneficiary alongside U.S. equities when the conflict sees a resolution.

History has shown that well-diversified investors have been rewarded for staying the course. It’s not clear when the conflict in Iran will end and volatility is likely to persist in the near-term, but some of the pain points are clear. For nervous investors, trimming exposure in Europe, where the epicenter of the pain is, might provide an opportunity to pull back on risk. And if higher energy prices persist with an upside shock to inflation, investments in infrastructure and gold offer long-term potential to diversify and offset geopolitical risk.

All market and economic data as of 03/20/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

Global Investment Strategist