Oil shock jolts American stocks into driver’s seat … for now

The biggest conflict in the Middle East in decades, a $10 spike in the price of oil, a dramatic drop in global equities and a rush to safe-haven assets. So, why has the U.S. stock market appeared resilient at a moment when international equities have been outperforming year-to-date?

This isn’t 2019 when drones attacked Saudi Aramco’s oil fields – or even 2022 when Russia invaded Ukraine, pushing oil prices higher by roughly 45% to $140 per barrel. It’s not about oil supply risk. It’s about price risk. The United States is the largest consumer of oil in the world. So, at first glance, it may seem obvious that higher oil prices hurt Americans first and foremost. But the nuance is in the source of the risk.

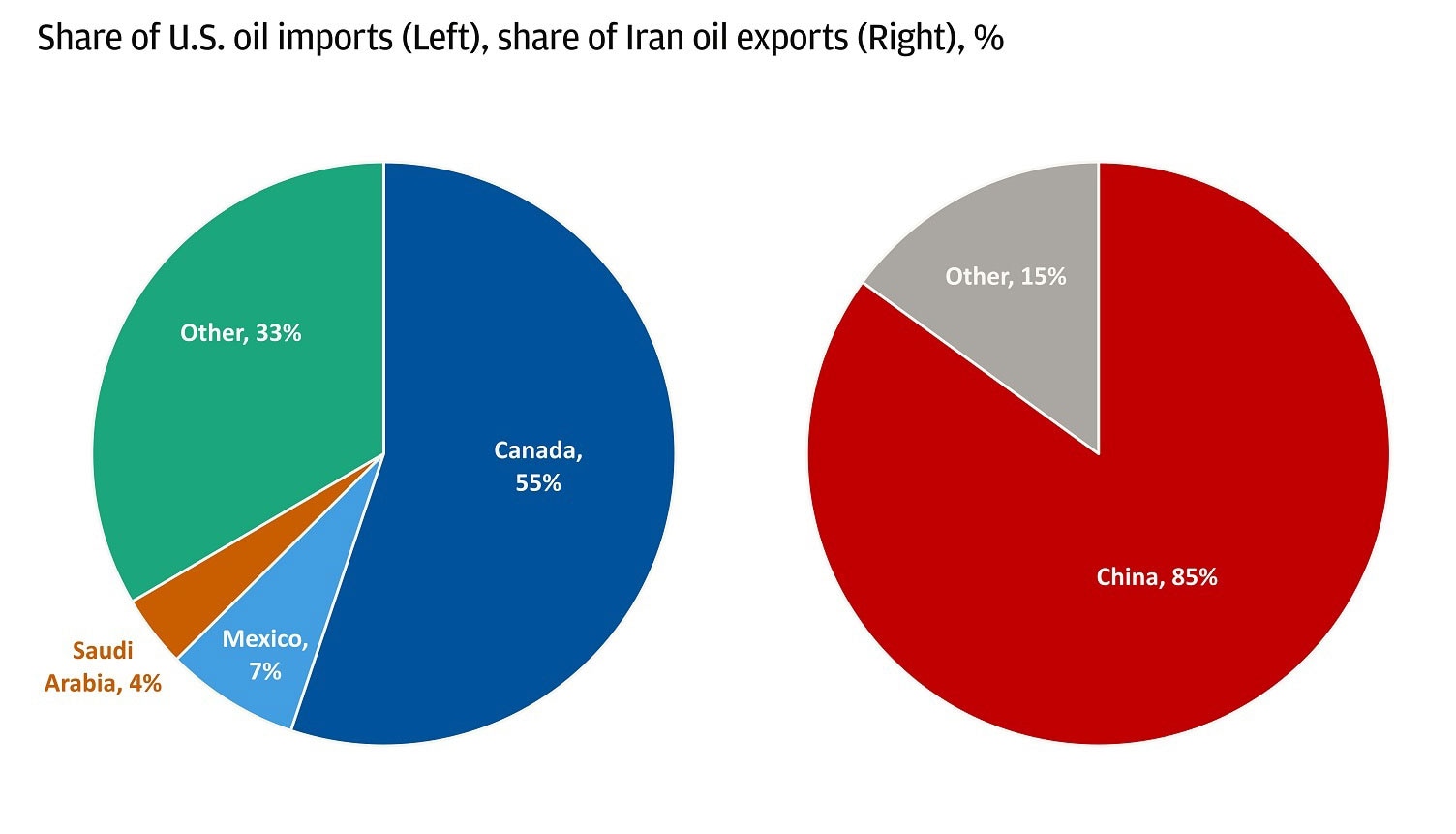

The United States is not meaningfully exposed to oil from Iran, or more broadly the Middle East. It sources the vast majority of its oil imports from Canada and Mexico, with 4% coming from Saudi Arabia, and is now the world's largest net exporter of oil. Meanwhile, 85% of Iran’s exports have been going to China via transportation meant to evade international sanctions, otherwise known as shadow fleets.

Where oil comes and goes

That doesn’t mean Americans are insulated from higher gasoline prices. After all, oil prices are subject to global supply dynamics. But energy independence means there is a lag before it shows up in prices at the pump, which makes it easier to weather short-term volatility.

In prior geopolitical shocks, the fear was scarcity. Would the barrels arrive at all? Today, the risk premium is embedded in the price, driven less by lost production and more by transit route uncertainty. One of the largest fears after the United States launched its military operation in Iran is the fate of the Strait of Hormuz, which sees roughly 20% of globally traded oil.

That’s how the stock market can very quickly take its cue from oil, likely on worries that eventually, should the price shock sustain, it can feed into the cost of manufacturing goods and transportation. Eventually, those costs may need to be passed onto the consumer, which could result in demand destruction. It’s an extreme scenario, but geopolitical conflict has proven to spur inflation in the past – for example, in 2022, when energy prices, driven by the fallout of the war in Ukraine and ensuing sanctions, made up one-third of the peak 9% inflation rate.

Jitters

A good way to measure the fear is through the correlation between oil and stocks. As risk assets trade on global growth, the default is to rise together. If Americans are making a good wage, spending, driving their cars and investing, then in theory, both oil prices and the stock market should gradually rally.

But when oil price increases are driven by geopolitical risk, rather than demand, they have a disproportionately negative impact on equities and economic confidence. And that’s when the traditional relationship breaks down. Since the U.S. military operation in Iran began, the correlation has already turned negative, reflecting the spike in oil prices and pressure on global stocks.

At the end of the day though, the breakdown is episodic, not structural.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

U-turn

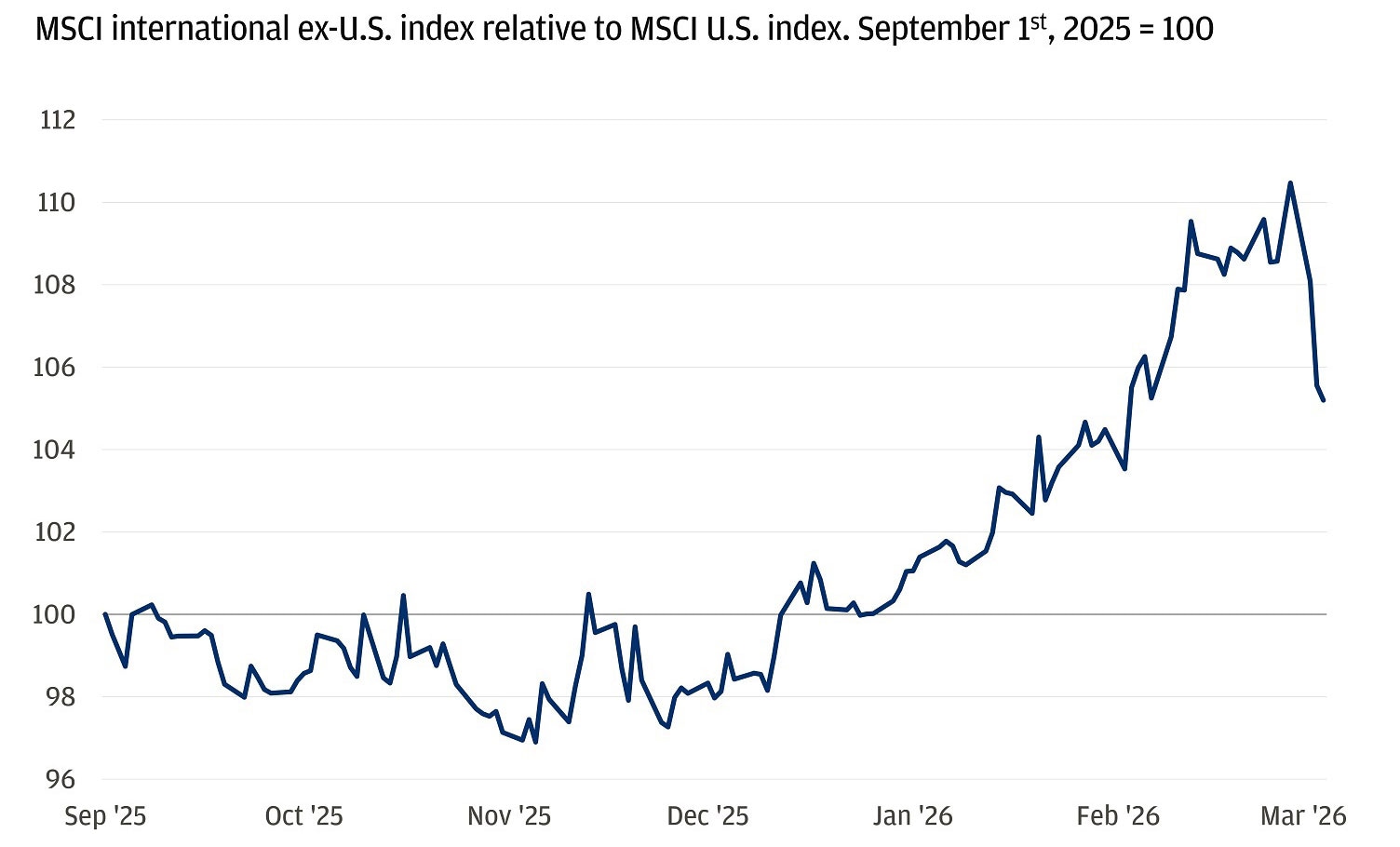

Driven by encouraging global growth signals, fears of lofty megacap tech valuations, artificial intelligence (AI) disruption concerns and American foreign policy, investors have flocked to international markets since the start of 2026. But the conflict in Iran could buck the trend. In the week following the military operation, U.S. equities have outperformed their international peers, reversing the year-to-date trend.

U.S. stocks have underperformed world benchmarks

Geopolitically driven oil shocks don’t reward global equity markets evenly. They tend to weigh more heavily on regions that are net energy importers and structurally exposed to Middle Eastern supply – like Europe and parts of Asia.

By contrast, the United States – now a net energy exporter – sits in a fundamentally different position given its physical distance from the conflict, North American energy sources and defensive nature of its stock market. Plus, a prolonged conflict that affects the Strait of Hormuz could have real consequences for global growth, endangering one of the key drivers in the bid for international equities. That doesn’t guarantee immediate U.S. stock market outperformance, but it does suggest the conflict could work against the markets abroad that have rallied since the start of the year.

All market and economic data as of 03/06/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

Global Investment Strategist