Your mortgage and credit reporting

Credit Reporting Basics

Read our tips for raising your credit score, and learn what factors into your credit report (including your payment history, errors on your report, good vs. bad credit and more).

Common questions about credit reporting

We send a range of account information including loan amount, account balance, scheduled monthly payment, payment history and status of your account to the four major credit bureaus (Equifax, Experian, TransUnion and Innovis).

The information we report to the major credit bureaus is required to be complete and accurate. Because of this, we don’t make goodwill or courtesy adjustments. We understand that you may be concerned about the potential impact of a late payment. Learn more about credit reporting information, including tips for raising your credit score.

A payment can be reported as past due if it’s received 30 or more days after the due date.

You’re entitled to a free credit report every 12 months from each of the four major credit reporting agencies (Equifax, Experian, TransUnion and Innovis). To get your free credit report or for more information, go to annualcreditreport.comOpens overlay.

If you think we’ve reported information incorrectly, you can dispute it with us and/or with the credit reporting agency.

Please send us detailed information indicating what you think is inaccurate and why. Include any documentation you have alongside your claim. This may include marked-up copies of the credit report specifying the information that's being disputed, front and back of a check, stop-payment confirmations or express mail receipts. Send it to:

Home Lending – Chase

Mail code LA4-6945

700 Kansas Lane

Monroe, LA 71203

You can also provide it directly to the credit reporting agency using the information below:

Equifax: 1-866-349-5191

Experian: 1-800-493-1058

TransUnion: 1-800-916-8800

Innovis: 1-800-540-2505

The way the account is reported to the four major credit bureaus can vary based on the type of assistance program you’re participating in and the status of your account before, during and after the program. Completing a payment assistance program doesn’t change any previously reported late payments. The impact on your credit score depends on your entire credit profile.

Program | During the Program | After Completing the Mortgage Assistance Program |

|---|---|---|

Mortgage Loan Modification | During the trial period, we'll report the account status as current and being paid under a partial payment agreement as long as payments are received on time. | If a loan modification is completed, we'll report the account status as modified and it'll show as current as long as payments are made on time. If a loan modification isn't completed and the account isn't current when the trial plan ends, it may be reported as past due. |

Repayment Plan | We'll report the account status as past due until the repayment plan is complete and the account is current. | We'll report the account status as current as long as payments are made on time. |

Forbearance Plan | We'll report the account status as current for a full forbearance plan. For a partial forbearance, we will report the account status as current if the payments are received on time. | At the end of the forbearance, we'll report the account status as current as long as payments are made on time. If the account isn't current when the forbearance ends, it may be reported as past due. |

Natural Disaster Forbearance Plan | We won't report any late payments during a natural disaster forbearance period. | At the end of the forbearance plan, we'll report the status of the account to the credit reporting agencies. If the account isn't current when the forbearance plan ends, it'll be reported as past due. |

Program | How It’s Reported |

|---|---|

Short Sale | We’ll report that the account was paid in full for less than the full balance. |

Deed-in-lieu | We’ll report that a deed in lieu of foreclosure occurred. |

A credit payment can be reported as past due if it’s received 30 or more days after your due date, even if you’re paying off your mortgage. It’s a good idea to make your payment as usual and we’ll send you a refund check if you overpay.

Here’s some other information to consider about mortgage payoffs:

- Your closing date may not be the day we receive your payoff. It may take additional time for your closing or title agent to send us your payoff funds.

- We'll apply the payoff funds on the day we receive them

- The good through date on your payoff quote is the expiration date on the amount indicated to completely pay off your loan. It doesn't provide an extended grace period to make your normal payment.

For more information about paying off your mortgage loan, go to our payoff quote page.

Once you pay your balance, we'll request an update to your credit report to reflect it paid. Since the account was paid after charge off, the charge off status will remain on your credit report.

The timing of when your credit report will reflect a recent update to your account is dependent on the credit reporting agencies (Equifax, Experian, TransUnion and Innovis).

If you have any additional questions about mortgages or credit scores, read our FAQs page for more information.

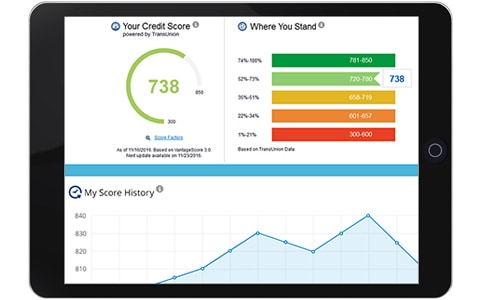

Credit Journey®

Get free access to your credit score and more, including alerts, weekly updates and a score simulator.