U.S. presidents over the years: A timeline of financial events

Editorial staff, J.P. Morgan Wealth Management

The United States’ financial system has seen plenty of interesting happenings over the years – from the creation of the first U.S. currency to the introduction of online banking. The navigation of these events has often fallen on the shoulders of our nation’s leaders, who have braved unchartered waters and left a mark on both money and history.

In honor of our nation’s presidents, we put together a timeline of some of the watershed financial moments through history and the U.S. presidents under which they occurred.

U.S. currency

America’s first President, George Washington, signed the Coinage Act of 1792 into law, paving the way for U.S. currency. Also known as the Mint Act, this legislation established the United States Mint in Philadelphia and made the U.S. dollar the country’s standard unit of currency.

The U.S. Treasury

The constitution was ratified in 1788, and with it came the subsequent creation of the U.S. Treasury in 1789, which was tasked with handling the growing national debt. Alexander Hamilton, who had been handpicked by President Washington to lead the effort, quickly devised a plan to pay back the country’s war debt and improve its public credit.

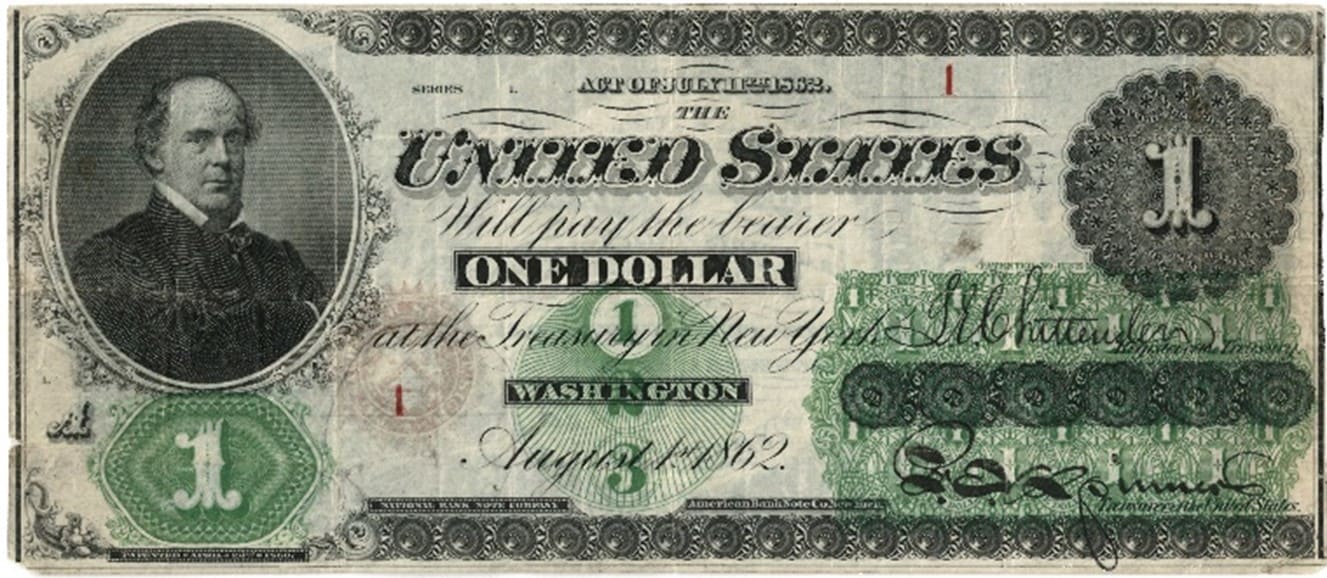

However, it was not until the Civil War that the U.S. government began printing paper money. Salmon P. Chase, the namesake (and not the founder!) of Chase National Bank, served as the U.S. Treasury secretary under President Abraham Lincoln. The Legal Tender Act of 1862 is perhaps the Treasury’s most notable legislation, as it created what would come to be known as the paper dollar (known as “greenbacks” then thanks to their green ink), which was a step toward a more uniform paper currency.

Get up to $1,000

When you open a J.P. Morgan Self-Directed Investing account, you get a trading experience that puts you in control and up to $1,000 in cash bonus.

The Federal Reserve

Aiming to address consumer panic, bank failures and hard-to-come-by credit, President Woodrow Wilson signed the Federal Reserve Act into law on December 23, 1913, which created and established the Federal Reserve System as the U.S. central bank.

The Great Depression

The Roaring Twenties came to a screeching halt in October 1929, when the stock market crashed and billions of dollars were lost, kicking off an economic depression that would last several years. The start of the Great Depression came just a few months after President Herbert Hoover’s first term began. During his first and only term, Hoover took several steps to improve economic conditions, but unfortunately found little success.

Federal Deposit Insurance Corporation (FDIC)

Just days after taking office in March 1933, President Franklin D. Roosevelt signed the Banking Act of 1933 into law, creating the FDIC in the process. The organization’s initial mission was to restore people’s confidence in banks throughout the Great Depression by insuring customer deposits. Today, it continues to play a critical role in protecting consumers' money.

Social Security

Vowing to protect Americans from the “hazards and vicissitudes of life,” President Franklin D. Roosevelt signed the Social Security Bill into law on August 14, 1935, which created a social insurance program designed to pay retirees age 65 or older post-retirement income. In the years since, this tax-funded program has dramatically reduced poverty among older adults and is a source of income many Americans rely on while in retirement.

Credit cards

Consumers today probably can’t conceive of a world without credit cards. But before 1950, that was the case – until the Diners Club Card launched. At first, consumers could only use this card in local restaurants and were required to pay the balance in full every month. The Diners Club card came out when Harry S. Truman was in office, but this novel payment form really took off under President Dwight D. Eisenhower’s administration. The credit card company eventually expanded to other retailers and countries, and it was also the first company in the industry to offer a rewards program in 1984.

In 1958, Chase Manhattan Bank introduced the Chase Manhattan Charge Plan (CMCP), becoming the first major New York City bank – and one of the first banks in the United States – to offer customers a single retail charge account. Chase was the first bank to offer customers credit at a citywide network of stores, replacing the need to open charge accounts with individual stores. The card was renamed the Uni-Card in 1969 before joining the BankAmericard System in 1972, which is known as Visa today.

ATMs

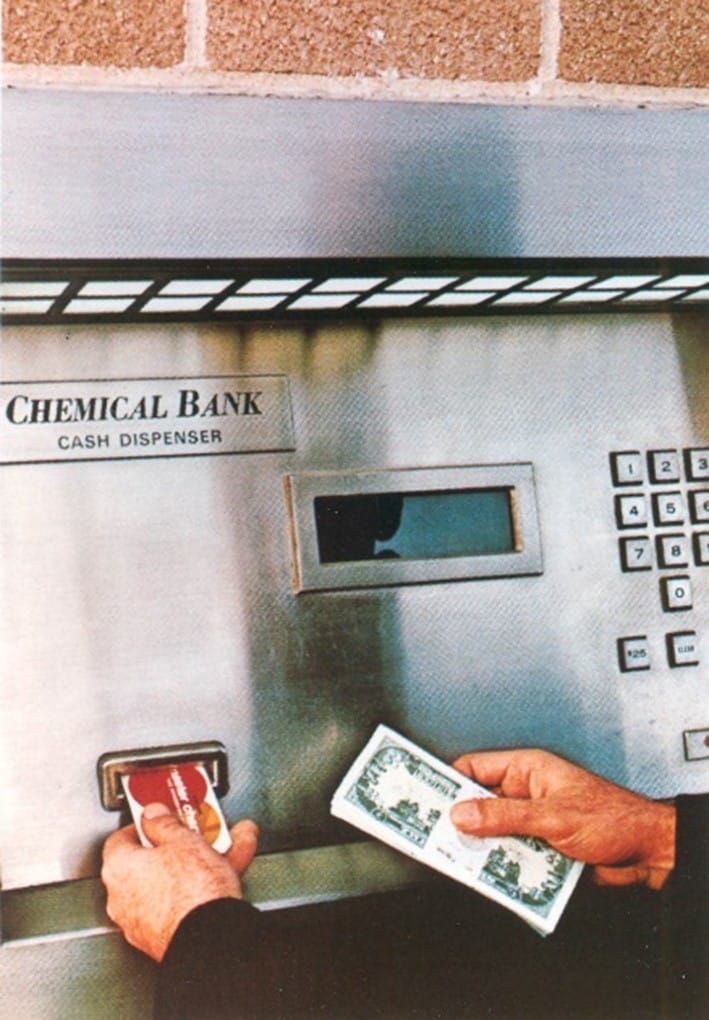

Getting cash outside of banking hours was unheard of until Chemical Bank installed a prototype cash dispensing machine, the precursor to the ATM, in the U.S. in 1969.

Manufactured by Docutel, this prototype, known as the Chemical Cash Machine, could only be used by bank customers and at first only dispensed $25 or $50. It’s hard to imagine life without this everyday convenience now, and it’s even harder to fathom that it’s only been around since President Richard Nixon’s administration.

Online banking

The early 1980s saw the advent of home banking, with Bank One’s Channel 2000 being one of the first to enjoy widespread use. From the comfort of their home, bank customers could view their account balances, transfer money and even pay bills over the phone while viewing everything on their TV. Three years later, Chemical Bank introduced Pronto, its first fully online banking service, followed by Chase Manhattan Bank’s three-tiered home banking service, named Spectrum, in 1985.

By the mid-1990s, many households had Internet access and were growing more comfortable doing business online. While at first limited to simply reviewing account activity, over the years these features and functions have expanded, to the point where some banks today operate solely online. But this growth may have never happened had President Bill Clinton not enacted the Telecommunications Act of 1996, which relaxed federal regulations that allowed smaller companies – and banks – to enter the telecommunications and broadcasting markets.

The Great Recession

Nearly 75 years after the Great Depression, the U.S. economy fell into another significant economic downturn, spurred by the collapse of the housing market, the closing of several major Wall Street firms and government bailouts of major companies like Ford, General Motors and AIG. The Great Recession spanned two presidential administrations, starting in December 2007 under President George W. Bush and ending in June 2009 during President Barack Obama’s first term. In response, the Obama administration passed the Dodd-Frank Act, which significantly tightened federal oversight regulations for banks – particularly larger, systemic institutions.

Cryptocurrency

Cryptocurrencies have been capturing headlines for a while now, even though they have only been around for about 16 years. The digital currency first made waves in 2009, right at the start of President Obama’s first term, but it wasn’t until 2020 under President Donald Trump’s first administration that the government started regulating these digital currencies. President Joe Biden’s administration worked to address crypto’s risks and identify its potential benefits, as evidenced by his Executive Order on Ensuring Responsible Development of Digital Assets, which was enacted on March 9, 2022.

Bottom line

Presidents Day isn’t just another chance to sleep in, but a day to remember our nation’s presidents and all they have done to make America what it is today. As our country continues to evolve, we hope to continue seeing financial breakthroughs that will make every American’s life a little easier – and we hope our leaders will continue to guide these advancements and their surrounding events with wisdom and fortitude.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management