Federal Reserve cuts rates as global equities and gold lead markets in December

Global Investment Strategist

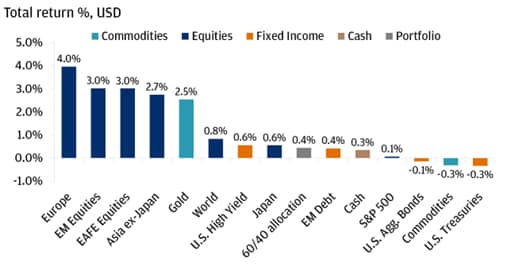

December wrapped up an eventful year in financial markets. Halfway through the month, the S&P 500 reached fresh all-time highs, but the so-called “Santa Claus rally” (i.e., the period when stock market prices historically rise between the last five trading days of December and the first two trading days of January) lost momentum, and U.S. equities ended the month up just 0.1%. However, global assets delivered strong gains in December, with international equities and gold posting positive returns (i.e., +3% and +2.5%, respectively). Additionally, the equity market rally was especially pronounced in Europe, which led all major regions for the month (+4%).

Quite a grab bag for the markets – but how did it happen? Below, we dive into what moved portfolios in December: shifting Fed expectations, international equity outperformance and gold finishing off a stellar year of performance.

International equities outperform in December

2026 Fed outlook relatively cautious after December rate cut, shaping market sentiment

The December Federal Open Market Committee (FOMC) meeting was a focal point for markets – not because the rate cut itself was a surprise, but because investors were searching for clarity on the Federal Reserve’s (Fed) policy direction heading into 2026. The Fed delivered its third consecutive 0.25% rate cut, lowering its benchmark rate to a range of 3.25%–3.50%.

However, Fed Chair Jerome Powell’s remarks made it clear that going forward, there will be a higher bar for additional cuts. He emphasized numerous times that following three consecutive “risk management” cuts, the Fed would need to see continued deterioration in the labor market to do much more. The Fed’s updated Summary of Economic Projections reflected this outlook, which now shows most officials expect only one more cut in 2026, aligning with our view.

For U.S. equity markets, the Fed’s stance helped set the tone for December: Early in the month, optimism around supportive policy contributed to the S&P 500 reaching new highs. However, the rally soon faded as investors digested the Fed’s more measured outlook and the reality that cuts could be limited moving forward.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

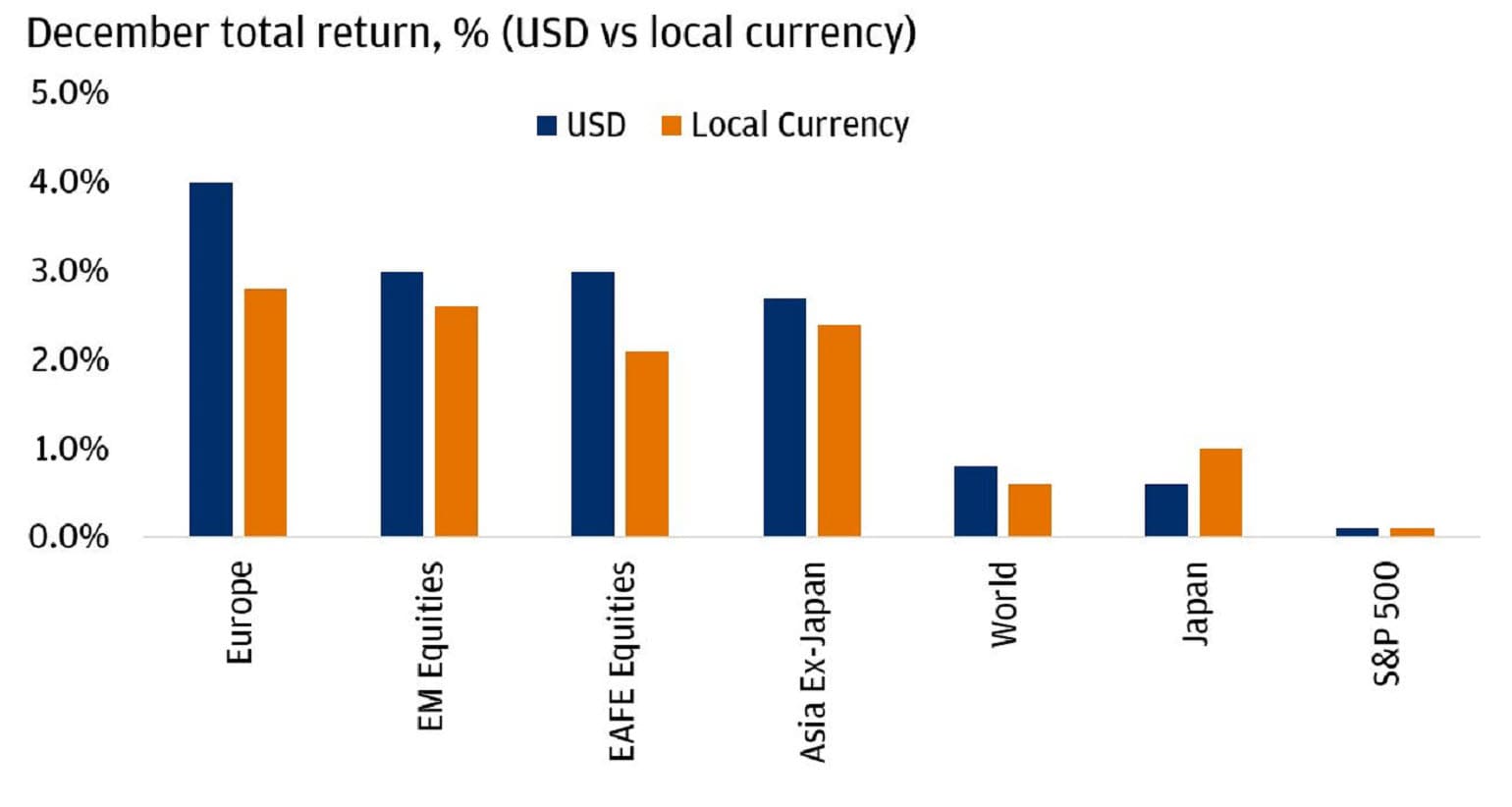

International equities deliver strongest returns since 2009 as a weaker US dollar boosts performance

2025 marked the best year for international equity performance since 2009: Investors saw the MSCI All Country World ex-US index rally nearly 30%, exceeding the S&P 500’s still-impressive 18% gain for the year. December was no exception, either, as foreign equities continued to outperform their U.S. counterparts.

Part of this outperformance was driven by a weaker U.S. dollar, which fell 1% in December. A weaker U.S. dollar can help boost returns when international stock gains are translated back into U.S. dollars, potentially enhancing the performance of international holdings for U.S. investors. The chart below shows how this dynamic has played out: When comparing returns of indices in local currency versus U.S. dollars, those based on the U.S. dollar have generally outperformed.

The modest decline in the U.S. Dollar added a boost for international equity market returns

However, we do not expect the U.S. dollar to keep falling in 2026. 2025’s dollar weakness was primarily driven by stronger growth outside the U.S. relative to initial expectations, but we think that trend has mostly run its course. We believe the U.S. economy can stay resilient this year, and as mentioned above, we don’t see many more Fed cuts on the horizon. As a result, we think the dollar will be steadier in 2026, even though currency moves typically can be unpredictable. This means that international stock returns may not get as much of a boost from currency effects as they did last year. Even so, a combination of relatively lower equity market valuations, strong earnings growth potential and increased defense spending keeps us positive on international markets as we move into the new year.

December surge, Fed cuts and a geopolitical hedge drive gold’s largest annual gain since 1979

In the spirit of strong returns, gold continued its rally in December (+2.5%) and posted gains in 11 out of 12 months, resulting in its largest annual gain since 1979. This formidable performance was fueled partially by persistent demand from both investors and central banks. Since the Fed resumed its latest cutting cycle in August 2024, the federal funds rate has been cut by a total of 1.75%, causing some investors to consider moving into gold, as yields on cash-like products fell simultaneously.

According to the World Gold Council, gold exchange-traded fund (ETF) holdings have increased by 23.5% since then, while the metal’s price itself has soared more than 73%. Investors haven’t been the only buyers, though – throughout 2025, central banks across the world have steadily increased their gold reserves. To illustrate, the People’s Bank of China added to its gold reserves for a 13th consecutive month in November.

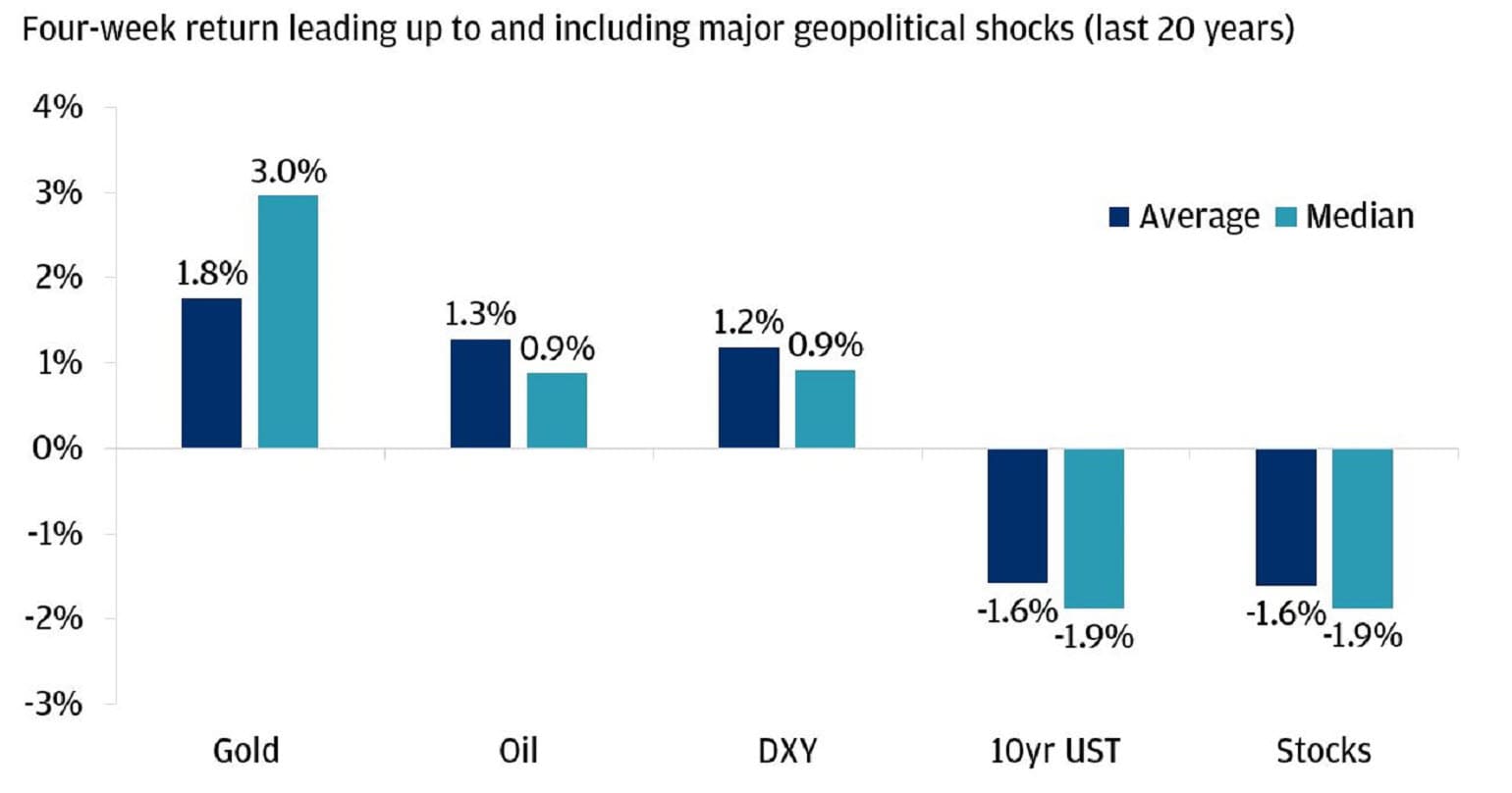

Gold may also be an attractive option for investors given its history as a top-performing hedge against geopolitical shocks, which contrasts with other asset classes that have experienced volatility in the wake of such turmoil. Looking at median four-week returns leading up to (and including) major geopolitical shocks over the last 20 years, gold has returned +3% compared to a median -1.9% total return for 10-year U.S. Treasuries and U.S. equities.

Gold is a top performer as a tactical portfolio hedge against geopolitical risk

December saw geopolitical pressures rise as the Russia-Ukraine war continued with military strikes and operations throughout the month – and seemingly no substantial progress made toward a peace deal or ceasefire agreement. Additionally, U.S. strikes on alleged drug trafficking boats around Venezuela – as well as a blockade of sanctioned oil tankers leaving and entering Venezuela – also focused U.S. investors on tensions closer to home. However, gold’s strong December performance was a keen reminder for investors of the potential benefits of diversifying across asset classes, especially during times of elevated geopolitical risk.

The bottom line

December’s flurry of market activity helps reinforce several portfolio construction principles for investors to consider in 2026: The combination of the S&P 500 surging to new highs and then reversing – along with strong performances from international equities and gold – highlights the possible benefits of having a portfolio that’s diversified across regions and asset classes and built to weather volatility. As the new year kicks off, though, we maintain a positive outlook on markets, and our 2026 Outlook: Promise and Pressure can be a helpful resource for those looking for actionable ways to potentially enhance portfolios in the coming year. Happy New Year!

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist