After the rate cut: Investing beyond U.S. markets

Global Investment Strategist

Fed moves, optimistic corporate outlook could point to rebounding economy in 2026

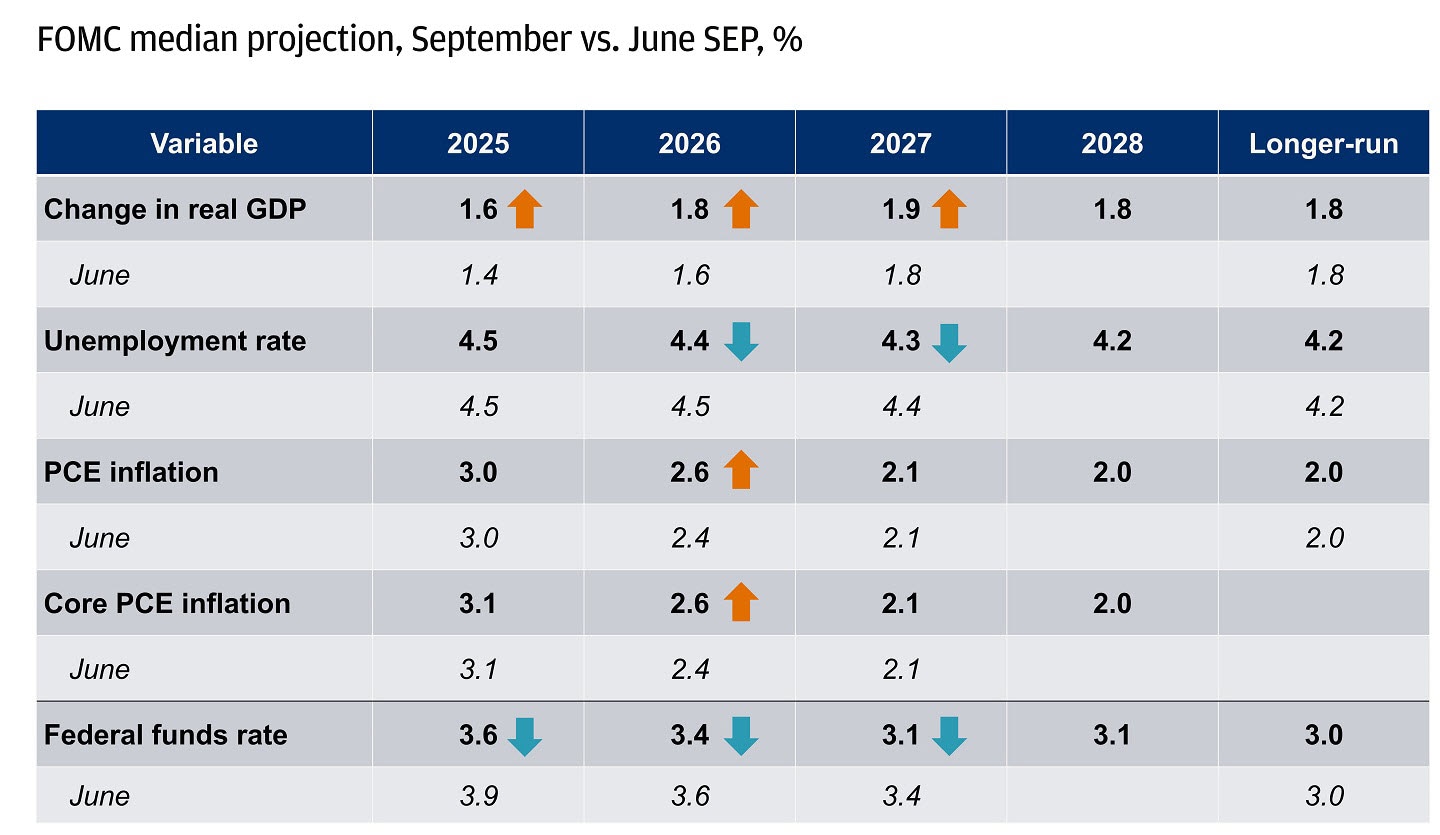

The Federal Reserve (Fed) cut rates by 25 basis points to 4%–4.25%, marking the first cut since December.

Here are the details that mattered: Most officials now pencil in one to two more cuts this year; there was one dissent (new member Stephen Miran favored a 50-basis-point move); and the projections point to firmer growth, slightly lower unemployment and a touch more inflation.

The Fed projects stronger growth, lower unemployment, and higher inflation

Markets cheered. After a muted first reaction, the message took hold: The S&P 500 pushed to new highs (its 26th all-time high this year), small-cap companies hit new highs for the first time since 2021, the U.S. dollar edged higher and U.S. Treasury bonds sold off – animal spirits are running high.

Two leading indicators also point to a rebounding economy in 2026: Corporate margins are near historical highs and, according to the Chicago Fed Survey of Business Conditions, companies are increasingly optimistic about the next six to 12 months.

It’s worth noting this is a rate cut during a slowdown, not a slump – which usually loosens financial conditions and supports global risk assets. What does that mean for investors? As discussed over the past two weeks, the Fed rate-cutting playbook is in motion:

- seek income in fixed income,

- position for risk-asset outperformance and

- diversify internationally.

Today we focus on international diversification.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

So, why look to invest beyond the U.S.?

Three key points come to mind:

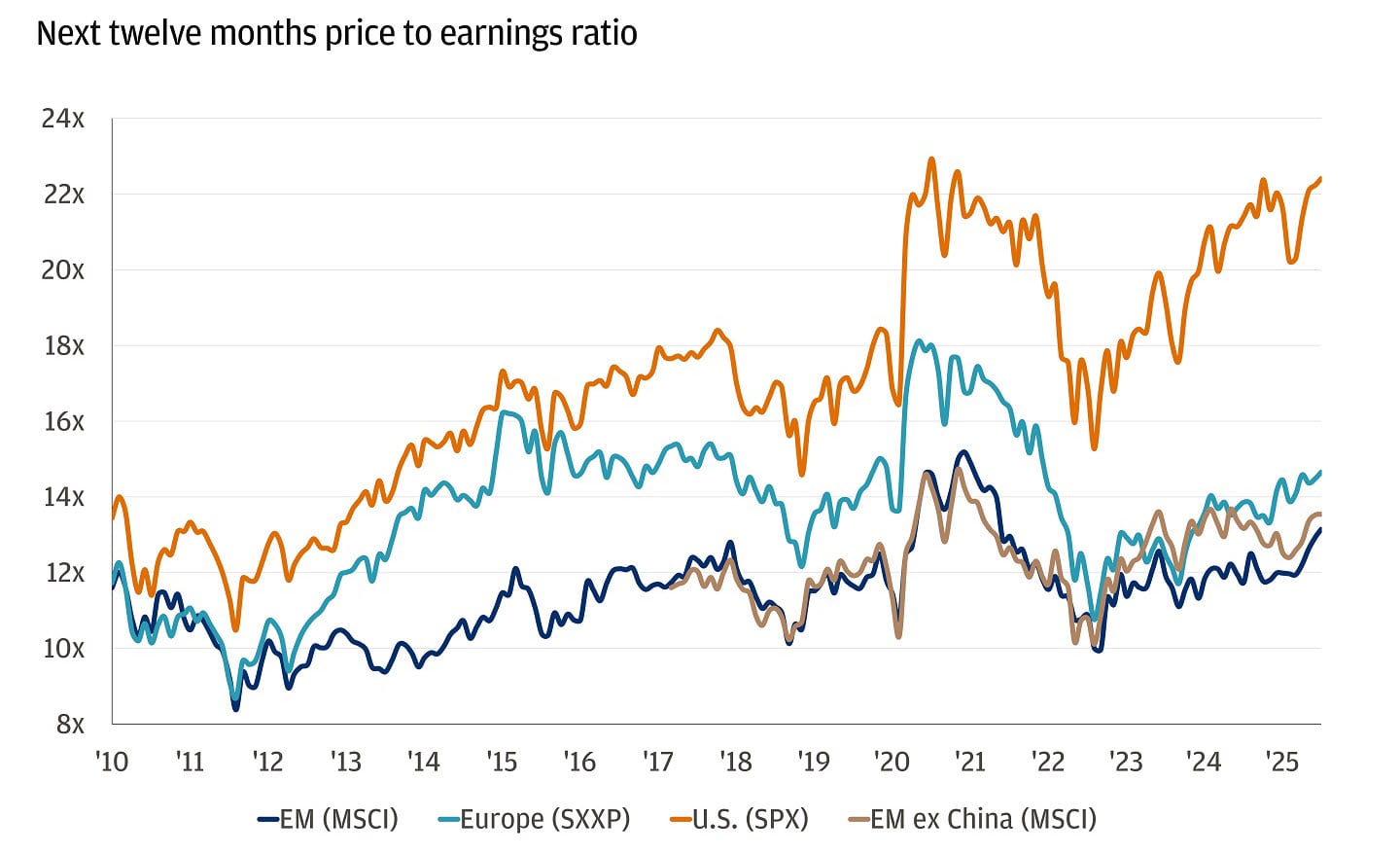

- High valuations. While we think it’s justified, the S&P 500 trades at about 22.5 times next-12-months (NTM) earnings, levels last seen in the late 1990s and 2000. Europe and emerging markets trade at about 15 times NTM earnings, a roughly 40% discount.

- Leadership is narrow. The top 10 stocks make up about 40% of the S&P 500 and 35% of earnings. The index looks very different than it did 20 years ago – with Tech and Communication Services now making up a much bigger share of market cap and profits. This shift means looking outside the U.S. is increasingly important for proper diversification.

- A softer U.S. dollar. Non-U.S.-dollar assets have often matched or outperformed U.S. assets during rate-cutting cycles outside recessions.

Next, how much diversification makes sense?

The U.S. remains the top destination for global capital, but starting with about 15% of a stock-bond portfolio in international markets is a reasonable baseline – adjusted for mandate, liquidity and risk. This allocation could help smooth returns and lower overall risk, especially if U.S. markets face headwinds.

In the multi-asset portfolios we manage, we remain overweight the U.S., but we also have high-conviction ideas internationally. Staying globally diversified helped protect our Chief Investment Office portfolios during the drawdown in April.

Europe and EM trade at a discount to the U.S.

Here’s how we’re thinking about the key regions:

Europe’s progress sets the stage for 2026

If you haven’t been following, the picture has improved: Growth has steadied, inflation is nearing 2%, unemployment is near cycle lows, housing loan demand is picking up and the European Central Bank (ECB) has moved to neutral – so monetary policy isn’t a headwind. While a stronger euro and politics add some noise, investors are focusing on fundamentals: The STOXX 600 is up about 10% year-to-date in local terms (22% in U.S. dollars). Valuations have moved up as well with Europe now trading at about 15 times forward earnings – above its longer-term average. We think this premium is justified and likely to persist, given the ongoing domestic recovery story.

Looking deeper, Germany-led fiscal programs and “Made in Germany” initiatives are channeling funds into semiconductors, clean energy, power grids and manufacturing. Defense budgets are set for multi-year increases, with European members committing to raise spending to 5% (3.5% for core defense, 1.5% for infrastructure). Many projects are set to ramp up in 2026, so most earnings gains are likely ahead. Trade tensions are calmer, with U.S. tariffs capped at about 15%.

Our view: Germany’s 500 billion euros in public support and 631 billion euros in planned corporate investment, plus rising defense spending, should support growth into 2026. We favor banks returning cash to shareholders, industrial suppliers, automation, materials and utilities tied to energy, while managing exporter exposure due to currency and tariff risks.

In the multi-asset portfolios we manage, we’re leaning into the trend of increased defense spending.

Emerging Markets (EM) are getting interesting

Emerging markets are a big slice of the real economy: roughly 86% of the world’s people and labor force, 77% of land, 59% of global gross domestic product (GDP) and 44% of exports – plus most of the key resources (about 87% of proven oil, about 83% of copper, about 77% of nickel and about 69% of lithium). In short, they’re worth knowing.

The sector has been doing well this year with the MSCI EM up about 25% so far. The Fed is easing, the U.S. dollar is softer, valuations are attractive, and trade clarity is improving – conditions that usually boost local earnings and unhedged USD returns.

Within EM, we favor:

- Taiwan: The central bank just raised its 2025 GDP forecast to about 4.6%, while exports hit a record in August ($58.5 billion, +34% year-over-year). We have a positive view on the artificial intelligence (AI) and semiconductor sector, supported by strong cash flow and clean balance sheets. TSMC holds a 70% global foundry share, and Taiwan is expected to build 90% of the world’s AI servers through original design manufacturers, capturing not just the chips but the systems.

- South Korea: Chip exports are at record highs, memory prices are firming and Purchasing Managers Indexes (PMIs) are stabilizing. Chip exports hit an all-time monthly high in August ($15.1 billion, +27% year-over-year), helping push total exports toward record territory despite tariff noise. Governance efforts are also nudging buybacks and dividends higher.

- India: This is a domestic-demand engine story with ongoing infrastructure and manufacturing build-outs. After underperforming year-to-date due to negative earnings revisions, we think India is through the worst of it. Looking ahead, both consumption and investment should pick up as looser monetary policy takes hold. The Internation Monetary Fund (IMF) projects 6.4% growth in 2025 – the fastest among major economies – and the manufacturing PMI signals firm expansion.

Our view: Emerging markets look attractive alongside the U.S. and Europe. The valuation gap and softer dollar help, while long-term growth stories add support.

China – Macro still soft; Constructive on tech

The macro picture remains weak. August net new loans rebounded but were still well below forecast, signaling struggling private credit demand. The economy remains in deflation, with inflation running at -0.4% – prices have been modestly declining for a couple of years. Home prices continue to fall, industrial output is at its lowest level since August 2024 and manufacturing PMIs remain below 50. On the positive side, exports have been more resilient and are the most important contributor to GDP growth this year, helping keep the full-year growth target within reach.

Policy has been about nudges, not a bazooka – focused on targeted measures and relying more on fiscal support to steady confidence. For now, Beijing is holding back on major stimulus, instead prioritizing steps like social welfare programs and urban upgrades. Under the current five-year plan, the aim is to shift from property-led growth to “high-quality” growth: steady the housing market, stabilize local government finances, keep bank credit moving, and channel capital into chips, clean energy and electric vehicle (EV) supply chains and digital infrastructure. With exports holding up and the growth target in sight, broad stimulus is unlikely before next year. Equities have rallied on stimulus hopes and clearer tariff rules, but the macro picture hasn’t improved decisively.

Our view: China is a two-speed story – external strength and domestic weakness. On the macro side, what would turn us more positive are: 1) stronger consumption data, 2) a clean move away from deflation and 3) better corporate earnings and revisions breadth. Still, we see opportunity in China’s innovation space as regulation has stabilized and the domestic AI sector continues to advance. While large-cap tech names have rallied, we’re focused on a broader set of innovative companies – including both large and mid-sized names – tied to themes like AI and super apps, new energy vehicles and autonomous driving and semiconductor localization. Considering the sharp rally, using structured products may offer a way to find better entry points and take advantage of volatility.

The bottom line

All in all, our rate-cutting playbook encourages seeking opportunities both within and outside the U.S.

All market and economic data as of 09/19/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist