Why the U.S. economy and S&P 500 are diverging

Tech sector wavers despite signals of increased economic activity

Tech stocks came under pressure this week as investors took a closer look at artificial intelligence (AI) following several high-profile investment announcements. At the same time, jobs and services data surprised to the upside, signaling a pickup in economic activity compared with last month.

On the political front, we had a few significant elections this week – most notably, Zohran Mamdani won the race for mayor of New York City. His leadership brings fresh ideas, as well as some questions about fiscal discipline. Our take: While the new mayor has some material powers, most major changes will require cooperation with the City Council and state government. In other words, dramatic shifts are unlikely in the near term.

Interpreting the disparity between equities markets and the U.S. economy

One of the biggest contrasts this year has been the widening gap between Main Street and Wall Street. Wage growth has cooled (the Federal Reserve Bank of Atlanta’s tracker is around 4% lately), and everyday sentiment has slid (the University of Michigan's monthly Survey of Consumers, which tracks consumer sentiment, is at 53.6 in October, down from 70.5 a year ago), while S&P 500 earnings and margins have marched higher (blended net margin is about 12.9% in Q3, above the five-year average). Hence the cliché: Markets are not the economy.

But what does that really mean? Stocks tend to move with company profits, while the broader economy is driven by paychecks and consumer spending. That’s why the S&P 500 can keep climbing even when everyday sentiment feels soft.

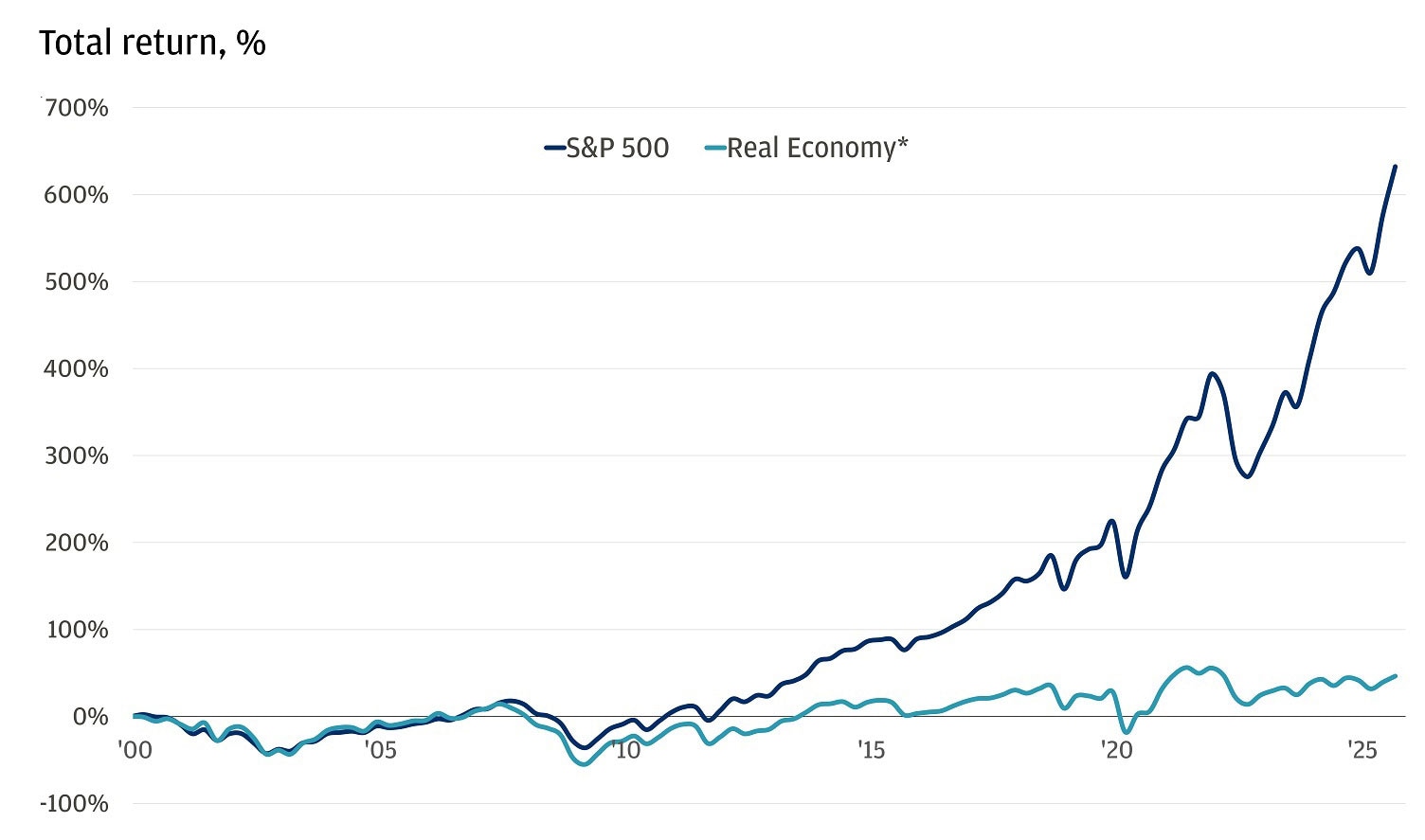

Looking at the numbers since 2000, S&P 500 earnings per share (EPS) are up about 356%, and the total return is up roughly 632%. By comparison, nominal gross domestic product (GDP) has grown around 200%, and the “average company” (as measured by the Value Line Geometric Index) is up just 47%. That gap in growth and returns is what really sets the market apart from the economy.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

The S&P 500 has far outpaced the real economy

We’d make three key points that highlight the difference:

The U.S. economy runs on services – about two-thirds of household spending – while the S&P 500 is weighted toward goods and platform businesses.

Most of what households spend goes to services – about two-thirds of personal consumption expenditures (PCE) – so people feel the economy through things like rent, health care, dining and travel.

By contrast, the S&P 500 leans toward products and platform businesses. Technology alone makes up roughly a third of the index today (around 36%), and other goods-linked sectors – such as branded goods, industrial equipment, energy and materials – account for a significant share of market capitalization (using today’s sector weights, goods-linked sectors account for approximately 25% of the S&P 500’s market cap). Overall, this greater technology/goods mix helps explain why stocks can rally even when Main Street feels soft: Large, listed firms tend to run with high margins and scale globally.

The U.S. economy is mostly domestic, but the S&P 500 generates about 30% of its sales overseas.

The U.S. is relatively closed – exports make up only about 11% of GDP – so most economic growth comes from within the country. By contrast, the S&P 500 earns roughly 28%–30% of its revenue abroad, and in the Technology sector, it’s closer to 55%. This means foreign demand and currency movements can impact the index, even when U.S. economic data feels soft.

A weaker dollar also boosts translated earnings for these companies; recent estimates suggest a 10% drop in the U.S. dollar can provide about a 2% tailwind to S&P 500 EPS.

The US economy tends to follow wages, while the S&P 500 is driven by profits per share.

Start with the basics. GDP runs through paychecks and household spending. When wages grow and hours rise, the economy usually grows faster.

Markets are different. Stock prices lean on profits per share – that’s earnings, margins and how those profits are spread over fewer shares when companies buy back stock. So, what’s been happening lately?

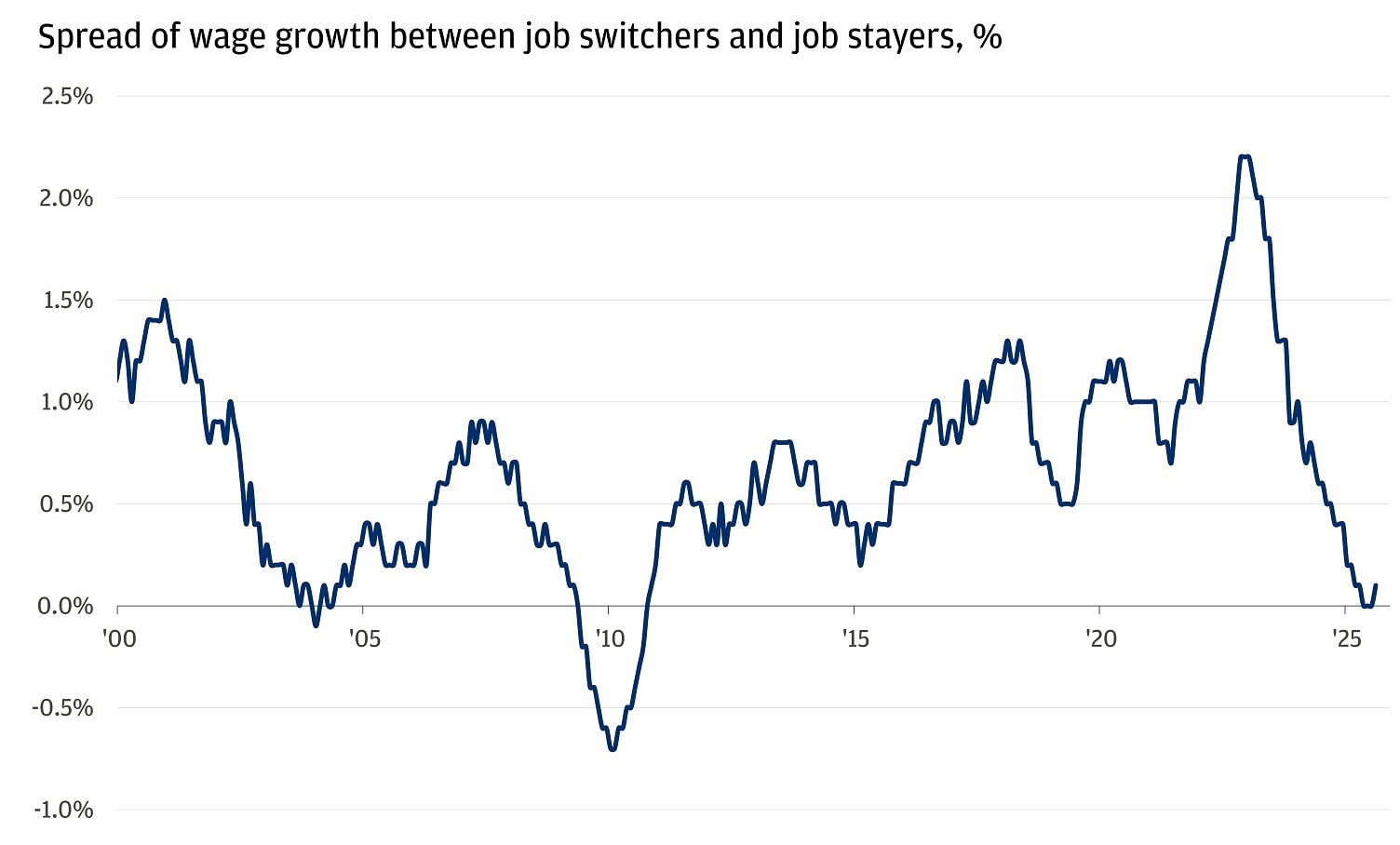

Wages have cooled.

The extra pay from switching jobs has narrowed, and quits are lower than in 2022–2023 – less wage heat.

The pay boost for switching jobs has faded

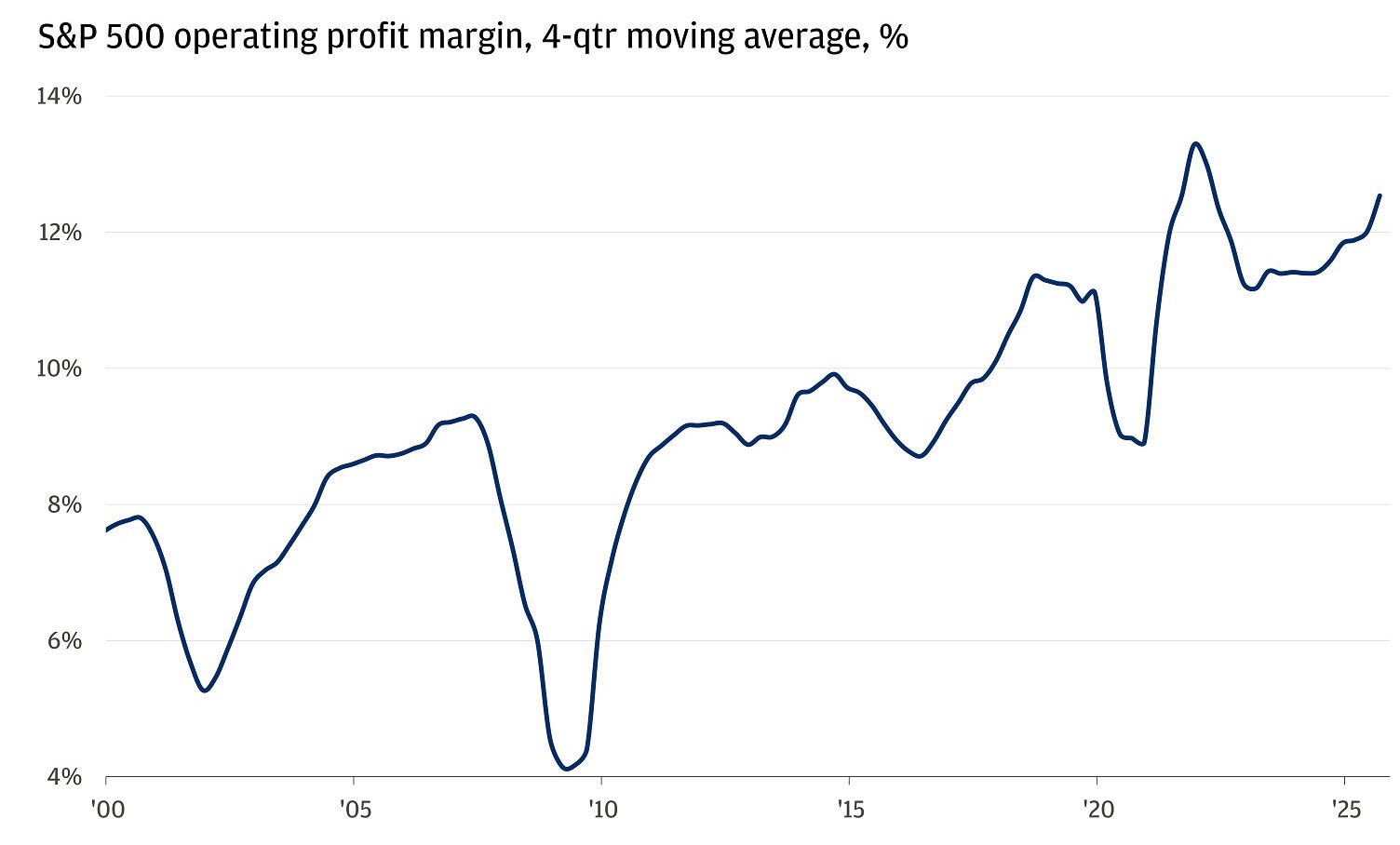

Profits have firmed.

Corporate margins have rebuilt from the 2022 dip, and many large caps keep returning cash via dividends and buybacks. In fact, profit margins for goods industries are about 60% higher today than they were back in 2018–2019, according to National Income and Product Accounts (NIPA) data. That kind of strength helps support EPS even as wage growth slows.

Profit margins are rising after their decline in 2022

The bottom line

In this phase, capital-heavy growth is beating payroll growth. The AI buildout is a prime example – there is heavy investment in data centers and equipment, not a hiring surge. That setup lifts profits more than payrolls, so the index can outpace GDP even when the labor market downshifts.

In all, there’s been a lot of talk about the gap between the economy and the market – uncertainty on the ground alongside indexes near record highs. It’s uncomfortable, but it makes sense. Markets are profit-oriented. They price in earnings, margins and per-share growth, not the day-to-day of wages or sentiment. And in this cycle, our three drivers point the same way.

We’re also living through a structural shift – more political risk, louder populism and choppier headlines. Markets can look past that when profits hold up, as they have done this year. That’s why the gap can persist: The index rewards scalable businesses that keep growing earnings, even when growth slows in the broader economy.

All market and economic data as of 11/07/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist