Shutdowns and market highs: The top 3 questions investors are asking now

Global Investment Strategist

Stock market pushes higher, despite government shutdown and labor market pressure

Relentless. Softer labor reports and a federal shutdown… and yet stocks keep ripping. The S&P 500, Nasdaq-100 and Dow Jones Industrial Average all notched fresh records. Talk about a dichotomy.

On the data side, hiring softened and early signs point to easing shelter inflation. In Washington, the shutdown matters for how the government operates: Shutdowns impact programs funded by congressional appropriations, also known as discretionary spending. Meanwhile, programs funded outside the appropriations process – known as mandatory spending – continue, like Medicare, Medicaid and Social Security.

Much of the market’s momentum this week came from artificial intelligence (AI). Meta and Microsoft announced large, multiyear commitments to secure more computing capacity – more chips and more data-center buildouts – lifting the AI ecosystem and the platform leaders. That wave helped pull the major equities indexes to fresh highs.

All in all, markets are leaning into the cooling-but-not-collapsing narrative. Investors price in a 99% chance of another interest rate cut this month, equities made all-time highs across the board, U.S. Treasury yields declined across the curve and the U.S. dollar weakened. Private markets sang the same song – after OpenAI’s latest secondary transaction, the company is now valued at $500 billion, making it the most valuable startup and surpassing SpaceX. This keeps AI front and center for risk appetite.

With that backdrop, three questions are top of mind:

What does the government shutdown actually mean for markets and growth?

About 25% of total federal spending is affected by the shutdown, and around 40% of federal civilian employees are furloughed. Two things come to mind:

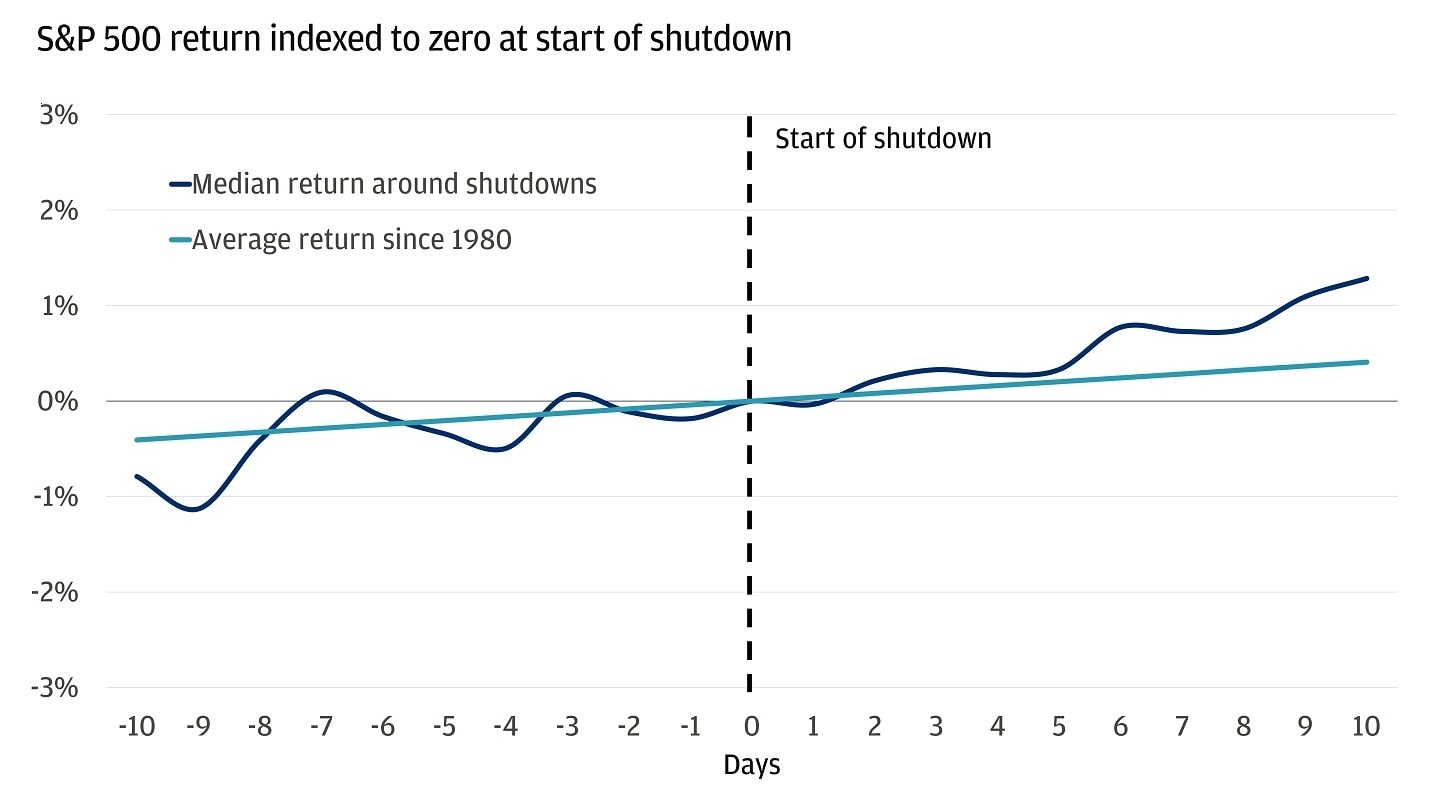

First, investors have historically treated shutdowns as non-events – there hasn’t been a clear market impact overall. On average, the S&P 500 has continued its typical positive trend in the days before or after a shutdown, and U.S. Treasury yields and the U.S. dollar have followed a similar pattern.

Shutdowns have not affected market trends

Past performance is no guarantee of future results.

Why? Shutdowns have no bearing on Treasury debt (unlike debt ceiling standoffs, like in 2013), and the economic impact is typically limited. While each week of a shutdown is estimated to reduce quarterly gross domestic product growth by about 0.1 to 0.2 percentage points – especially since none of the appropriations bills for 2026 have been passed – most of this impact is typically reversed in the following quarter. In other words, federal workers don’t get paid during a shutdown but receive back pay once funding is restored.

Second, economic data releases are affected. Yesterday’s initial and continuing jobless claims weren’t published on time, and the September employment report from the Bureau of Labor Statistics (BLS) will not be published today. In general, we’d expect data releases scheduled for early October to be delayed by slightly longer than the duration of the shutdown, as was the case in prior episodes. To fill the gap, economists rely on other sources. For instance, the Federal Reserve Bank of Chicago’s unemployment index – sometimes referenced by its president, Austan Goolsbee – isn’t affected by the shutdown since it’s not funded through congressional appropriations. The point is, the Federal Reserve (Fed) can still monitor the labor market and make informed decisions even if the BLS report isn’t published, as there are several alternative data sources available.

There are some concerns this time, as the Office of Management and Budget has asked agencies to prepare for possible permanent job cuts – not just temporary furloughs. While the practical implications remain unclear, we’re closely monitoring the situation and will keep you updated as it develops.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Why is the Fed cutting rates?

Policymakers are prioritizing a weak labor market over a gradually rising, tariff-driven pace of inflation.

The three-month average of jobs added to the economy is hovering around 29,000, compared to an average of 168,000 last year. While we do not expect further significant deterioration – the kind that leads to recession – it makes sense for the Fed to gradually ease financial conditions.

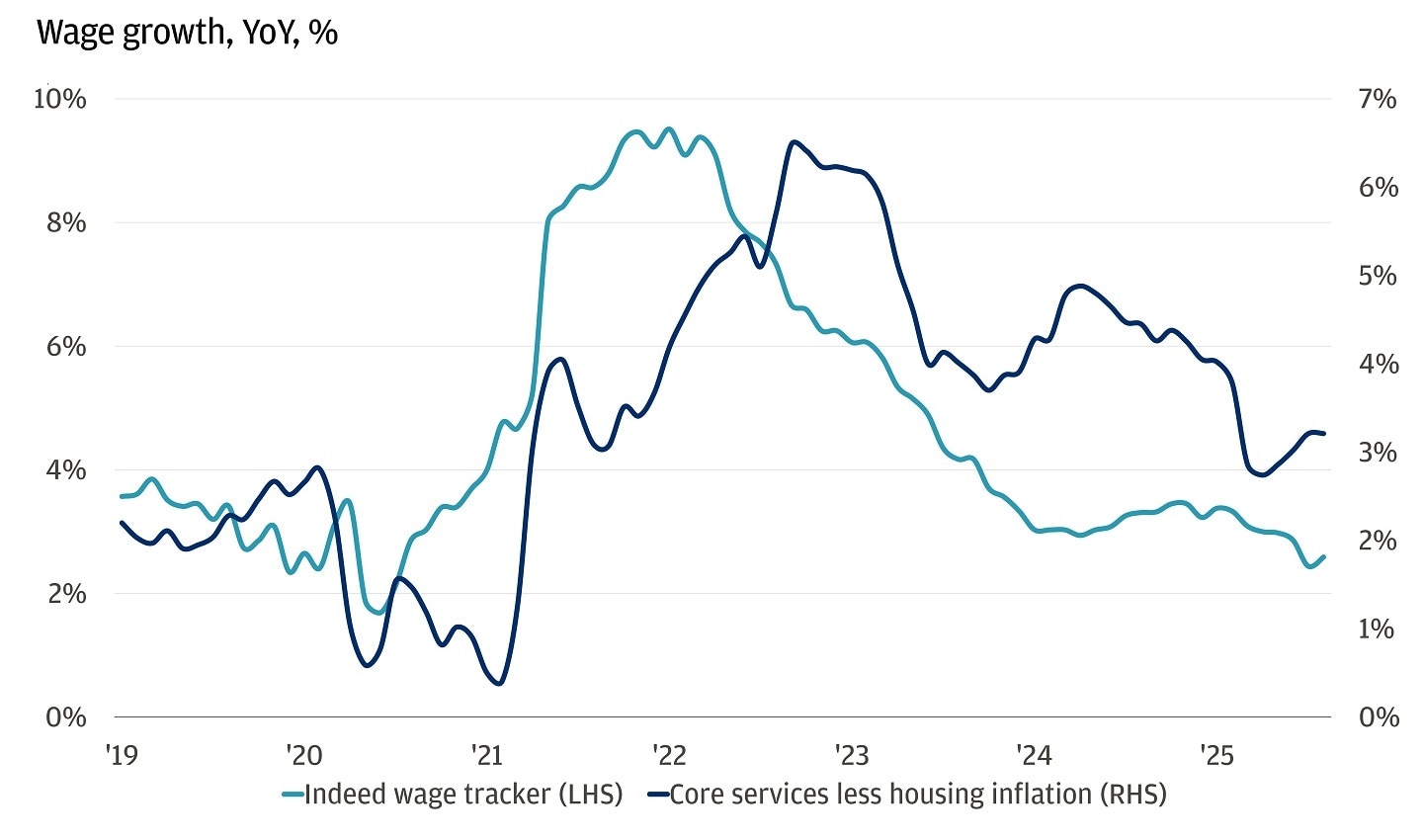

On inflation, we’re watching closely. We expect prices to rise gradually as tariffs continue to trickle through the economy. In fact, we estimate that consumers will eventually pay about two-thirds of tariffs, up from the current level of around 50%. However, we don’t expect this to spill over into the stickier services components of inflation – like energy and housing – or to impact inflation expectations. Energy prices are flat year-over-year, and shelter inflation has been trending down, now sitting around 3.6% year-over-year – a level not seen since 2021. All in all, it’s difficult to see overall services inflation accelerate without stronger wage growth, which we don’t foresee given the loose labor market.

Difficult to see services inflation accelerate absent stronger wage growth

Is the AI rally feeding on itself?

To some extent, yes. AI leadership does create some self-reinforcing loops: The top 10 S&P 500 names make up about 40% of the index, and Nvidia alone is around 8%, so every new dollar into market cap-weighted funds tends to favor the same winners. But it’s not just hype – there’s real cash flow and heavy capital spending behind it.

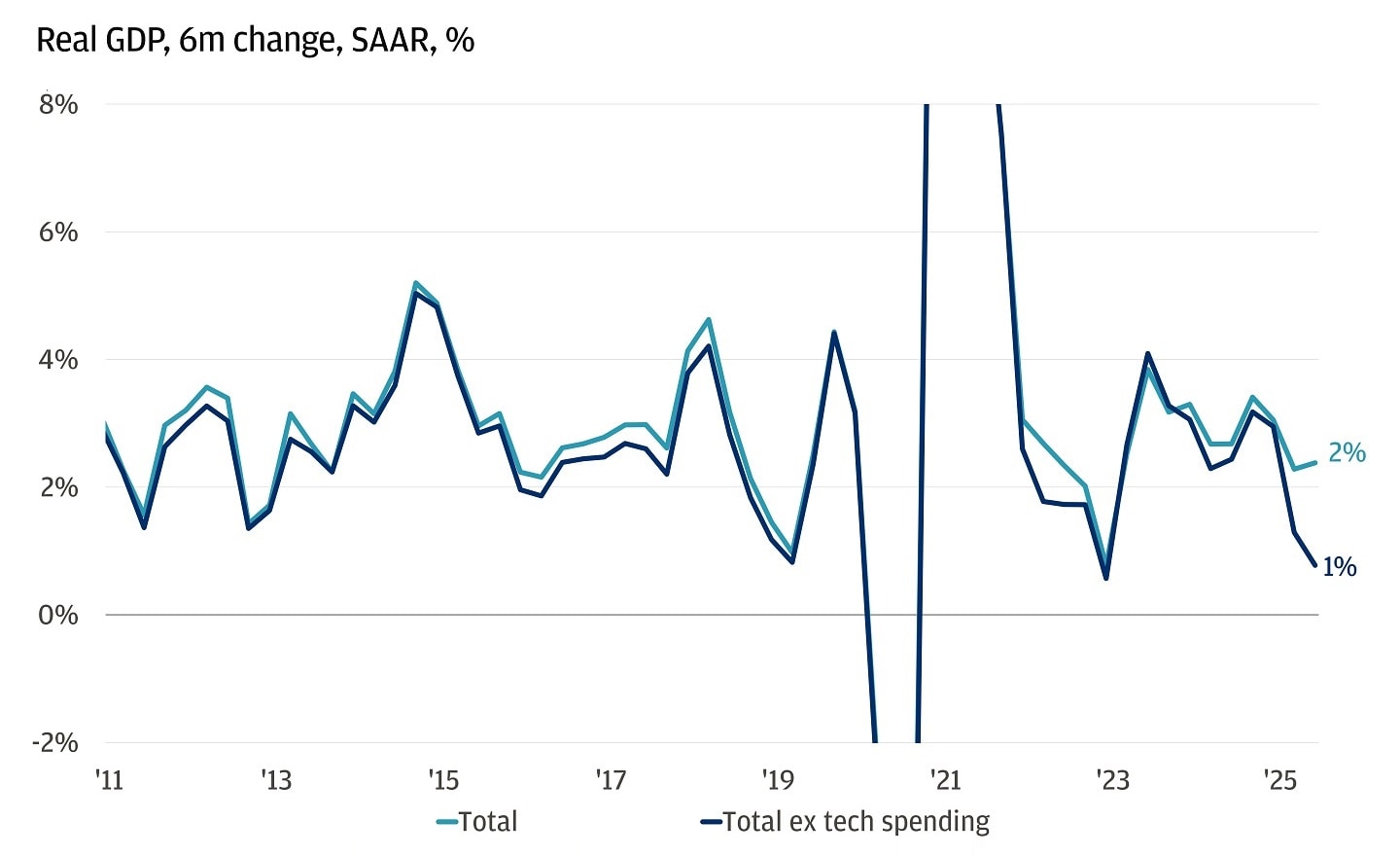

AI is driving U.S. stocks – and, increasingly, the real economy. Tech+ stocks overall now make up roughly 50% of the S&P 500 and account for about 60% of the market’s year-to-date return. Meanwhile, real U.S. growth in the first half of 2025 would be about half as strong if you stripped out capital spending on software and IT equipment.

The U.S. economy is stagnant without tech spending

Earnings and capital expenditure (capex) trends tell the story. So far this year, the earnings growth of the “Magnificent Seven” is about 28% year-over-year, and consensus expects 21% for the full year – three times that of the other 493 S&P names – and about 17% for 2026. Momentum is still going strong. On the capex side, we estimate it will increase by about 80% year-over-year to roughly $450 billion as AI builds accelerate. For those worried about a bubble in capex spending, it’s worth noting that the major hyperscalers building AI data infrastructure have less debt on their balance sheets than they generate in profit, and companies like Microsoft, Meta and Alphabet have a surplus of cash.

We’re watching closely as the story unfolds. The models keep getting better and requiring more compute power, which means more buildout. Strong financials and measured capex show no signs of an AI investment bubble, valuations remain contained and there’s still plenty of runway left for AI adoption – according to a Census Bureau survey, only 9.9% of companies report actively using the technology to produce goods or services.

The bottom line

Despite the noise from the shutdown, shifting Fed policy and questions around AI, markets have stayed focused on what matters: resilient fundamentals and an economy that’s still holding up. We’re keeping a close eye on policy shifts, labor market trends and the evolving AI landscape as key drivers for what comes next.

All market and economic data as of 10/03/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

For important disclosures, please refer to the disclosures section for detailed information.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist