The rate-cutting playbook: Fixed income in focus

Global Investment Strategist

Cooling labor market suggests interest-rate cuts could be forthcoming

The Federal Reserve (Fed) appears ready to resume its rate-cutting cycle. Some argue it is being pushed to act too quickly. We see a Fed prioritizing a cooling labor market over tariff-driven price noise. This week’s jobs data highlighted the slowdown:

- The ADP private-payrolls report, based on actual company payrolls, showed a gain of 54,000 jobs in August, below the expected 68,000. New filings for unemployment benefits rose to the highest level since June. Hiring is slowing, and the labor trend is softening.

- The Job Openings and Labor Turnover Survey (JOLTS), the government’s monthly tally of posted vacancies and worker flows, showed openings at a 10-month low. For the first time in four years, unemployed people now outnumber posted jobs. The 2022 gap of about two openings per job seeker has closed.

All of this led into today’s Bureau of Labor Statistics (BLS) August employment report, which pointed the same way. Payrolls rose by 22,000 jobs versus expectations of 75,000, and the prior two months were revised lower. Employment is slowing rather than collapsing – the unemployment rate is slowly drifting up toward 4.3%, in line with our view of a gradual slowdown. That keeps the “bad news is good news” setup intact and supports the case for a 25-basis-point cut.

With that backdrop, we’re dusting off the Fed-cutting playbook. Once cuts resume, the landscape could shift fast. Our framework includes the following:

- Embracing carry in fixed income

- Positioning for risk-asset outperformance

- Diversifying internationally

Today we focus on what it means to “embrace carry in fixed income.”

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Positioning fixed-income investments for potential rate cuts

With the path now clearer, let’s start with the basics – the two questions we hear the most.

1. What actually happens when the Fed cuts interest rates?

In short, cash rates decline, but by the time the Fed acts, the yield curve has usually priced it in. Markets are forward-looking; cash (your money-market yield) is typically the last thing to change.

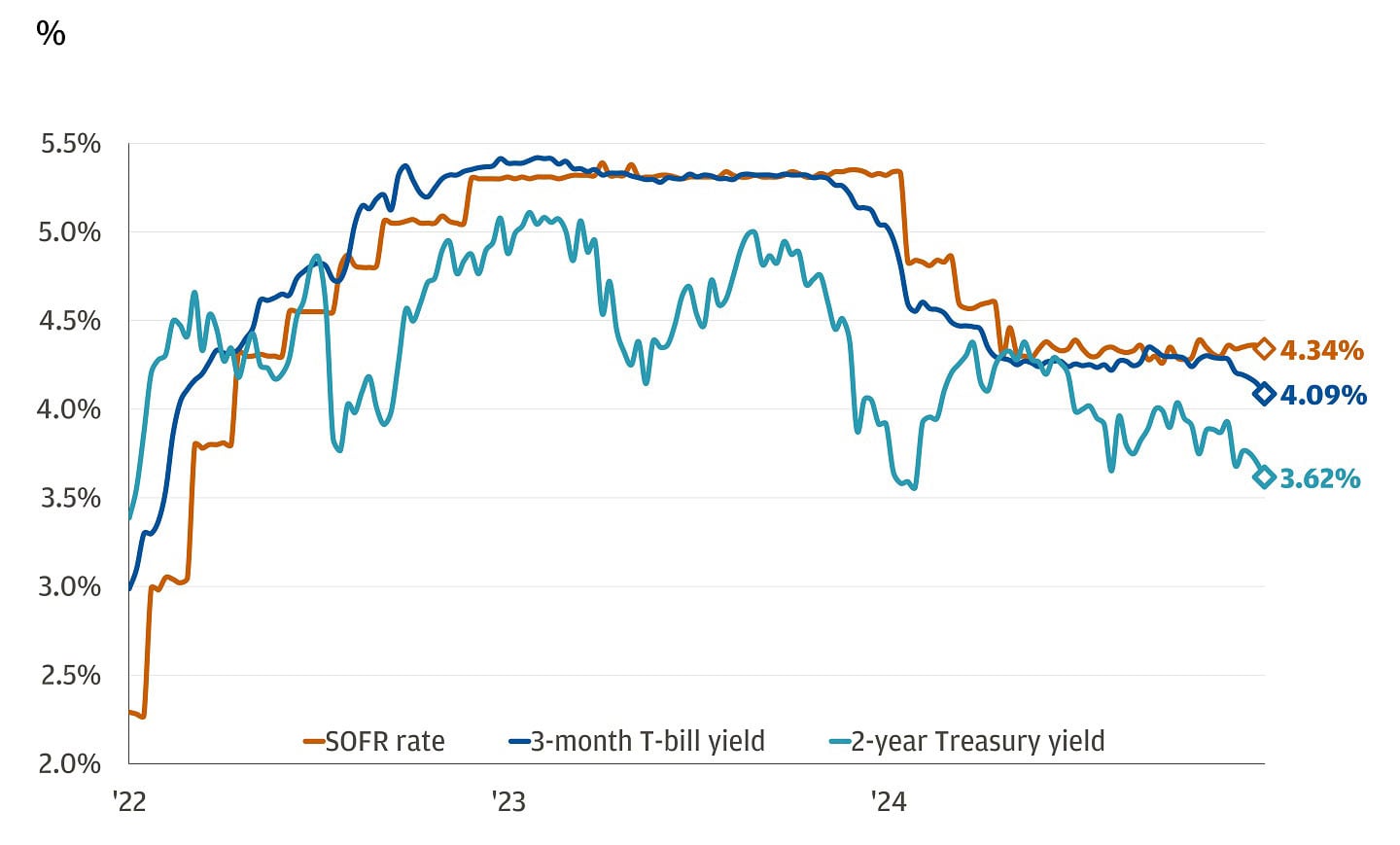

We’re already seeing it. The Secured Overnight Financing Rate (SOFR) – the overnight cost of borrowing cash against Treasuries, which closely tracks the federal funds rate – sits around 4.4%. The 3-month Treasury bill, a simple “cash-like” market proxy, is already down to about 4.1%, reflecting expected cuts.

What does this mean? The curve has already shifted down. Investors are pricing in an almost-certain September cut, with more expected to follow. The 12-month Treasury bill – a good proxy for what cash rates are expected to average over the next year– is near 3.7%, and the 2-year Treasury yield has fallen about 45 basis points since June.

Rates have moved lower. Cash is next.

Our take: The yield curve is much steeper now, so there is an incentive to go further out the curve. Two years ago, cash yields were as high or higher than longer maturities, making it hard to justify moving out. Today, it’s a different story: A 3-month Treasury yields 4.1%, while high-quality corporate bonds with three, five, seven or 10 years offer roughly 10 to 90 basis points more, depending on maturity.

Corporate leaders are signaling the same with their funding choices. Many high-quality issuers prefer very short-term commercial paper (30–90 days) over locking in multi-year bonds. The logic is simple: If borrowing costs are likely to fall, issuers may opt to stay short now and refinance at lower rates later. Uber rolled out a $2 billion commercial paper program and Netflix a $3 billion facility, while Coca-Cola, PepsiCo, Philip Morris International and Honeywell have all tapped the market recently. This is another sign the market expects lower rates. If corporate treasurers are staying short for flexibility, investors can do the opposite – extend selectively where yields remain elevated.

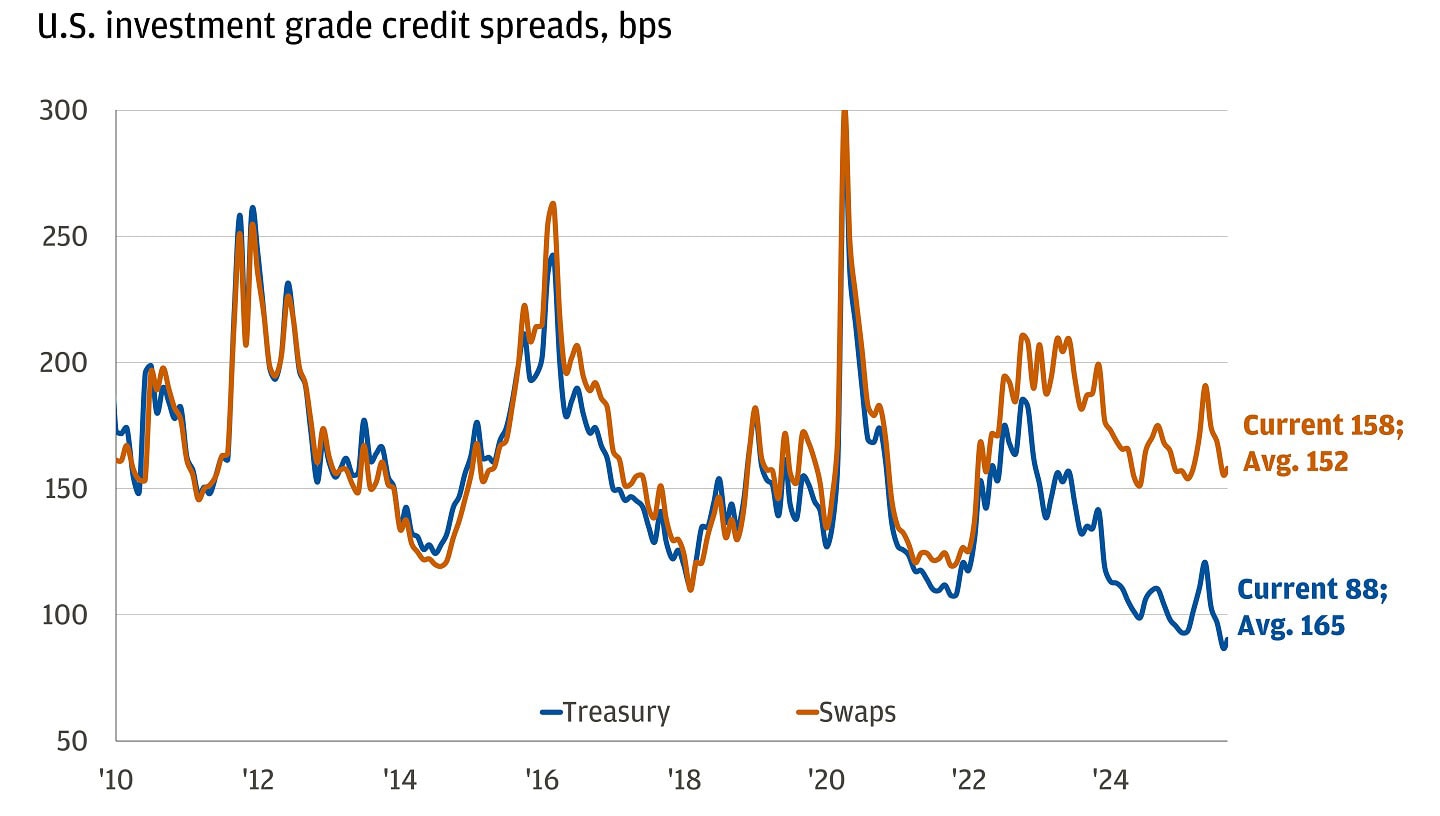

2. Are bonds “too expensive” because spreads are tight?

It depends on the ruler you use.

A spread is the extra yield a corporate bond pays over a “risk-free” curve. When spreads are tight, investors accept less extra yield for taking corporate risk, so bonds look expensive relative to that curve.

There are two reasons we look beyond the headline:

First, the benchmark moved.

Most people measure credit against Treasuries. Recently, Treasuries have traded cheaper than other risk-free yardsticks – think heavy supply, larger deficits and a rebuilt “term premium.” In plain English: Treasury yields are higher than they would otherwise be, so when you compare corporates to Treasuries, the “extra yield” looks smaller. If you use the swaps/derivatives curve built off SOFR – a cleaner proxy for the risk-free path – spreads look much closer to normal.

Credit spreads look less tight relative to alternative risk-free rates

Second, fundamentals and technicals still support firm spreads.

Balance sheets are generally disciplined – solid margins, moderate leverage, slower mergers and acquisitions (M&A) – and market technicals help: Manageable net supply and steady reinvestment demand keep a firm bid for high-quality income. Tight spreads can be justified in this environment.

Our take: Spreads look tight on a Treasury ruler, but closer to average on the SOFR swaps ruler. Overall, part of the “tightness” comes from the benchmark you use, not just the credit market itself.

History shows that, outside recessions, policy rates tend to drift lower after the first cut – about a percentage point in the year after the first cut – and our view is similar. We have focused on the belly of the curve this year to earn income and diversify without long-end volatility, and that has worked. With easing ahead, short-dated Treasuries already yield well below today’s 4% cash, so reinvestment risk is real.

To help offset that decline, here are three areas where we see value.

1. Investment-grade credit (10 years and below). We see value in high-quality corporates inside 10 years: They turn a drifting cash coupon into a steadier one at around mid-5% all-in yields, with single-digit duration instead of long-bond volatility. For context, $1 million at approximately 5% yields is about $50,000 a year before taxes. The market is deep and liquid, making it easy to maintain quality and ladder maturities. Overall, these investments could provide reliable income and contained rate risk.

2. Long-duration municipal bonds (10 years and above). We see value in high-quality, longer-dated munis because adding years meaningfully increases income – and that income is tax-free. Mid-4% tax-exempt yields, for top-bracket taxpayers, are roughly 7%–8% on a taxable-equivalent basis. If policy eases, longer bonds tend to benefit more from falling rates than short ones. It may help to keep it simple and high quality, and pay attention to call features on specific issues.

3. Hybrids (preferreds and corporate hybrids across banks, utilities, midstream). We are constructive on the hybrid space – bank preferreds, utility and midstream hybrids. In plain terms, these sit between regular bonds and common stock, typically offering more income than investment-grade bonds while still coming from large, well-capitalized issuers. The trade-offs: You are behind senior bonds in the payback line; the issuer may keep the security outstanding past the first call (extension); coupons can be paused during periods of stress; and early redemption can occur if tax or regulatory rules change.

As cuts approach, the simplest way to prepare is to turn a rolling cash coupon into a steadier one – locking in the yield you enjoyed while cash rates were elevated. Next week, we will return with our updated thoughts on the equity market.

All market and economic data as of 09/05/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist