Defying the tariff drag: 3 reasons markets are moving forward

Global Investment Strategist

Market Update

Investors have turned risk-on amid a flurry of positive trade headlines and strong corporate earnings. Fears over trade and policy setbacks are fading as investors focus on strong fundamentals: The labor market remains resilient with initial claims down for the seventh consecutive week, while the U.S. composite Purchasing Managers’ Index (PMIs) hints at an accelerating economy.

The bottom line? Risk spirits are running high. Equity markets are hitting new highs globally, with the S&P 500 marking its 13th all-time high this year, while sovereign bonds have sold off.

While there are some weak spots, the resilience is clear. Bears label it complacency. After all, if someone had predicted a 15% to 20% tariff rate at the year’s start, many would have expected a tough year for risk assets. So, why isn’t that the case? We can think of three reasons.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Spotlight

1. Costs are shared among foreign exporters, U.S. businesses and U.S. consumers.

U.S. consumers, businesses and foreign exporters are all chipping in on tariff costs. We estimate U.S. consumers are paying about a third of the tariffs so far, with foreign exporters and U.S. businesses sharing the other 66% based on our look at goods prices and revenue collections through June. All that to say, consumer burden is low, especially compared to the 2018 and 2019 tariffs when U.S. consumers bore 80 to 90% of the costs. The key difference this time? U.S. companies can absorb some costs to keep their market share. After all, their profit margins are about 60% higher today than they were in 2018 and 2019, according to National Income and Product Accounts (NIPA) data for goods industries.

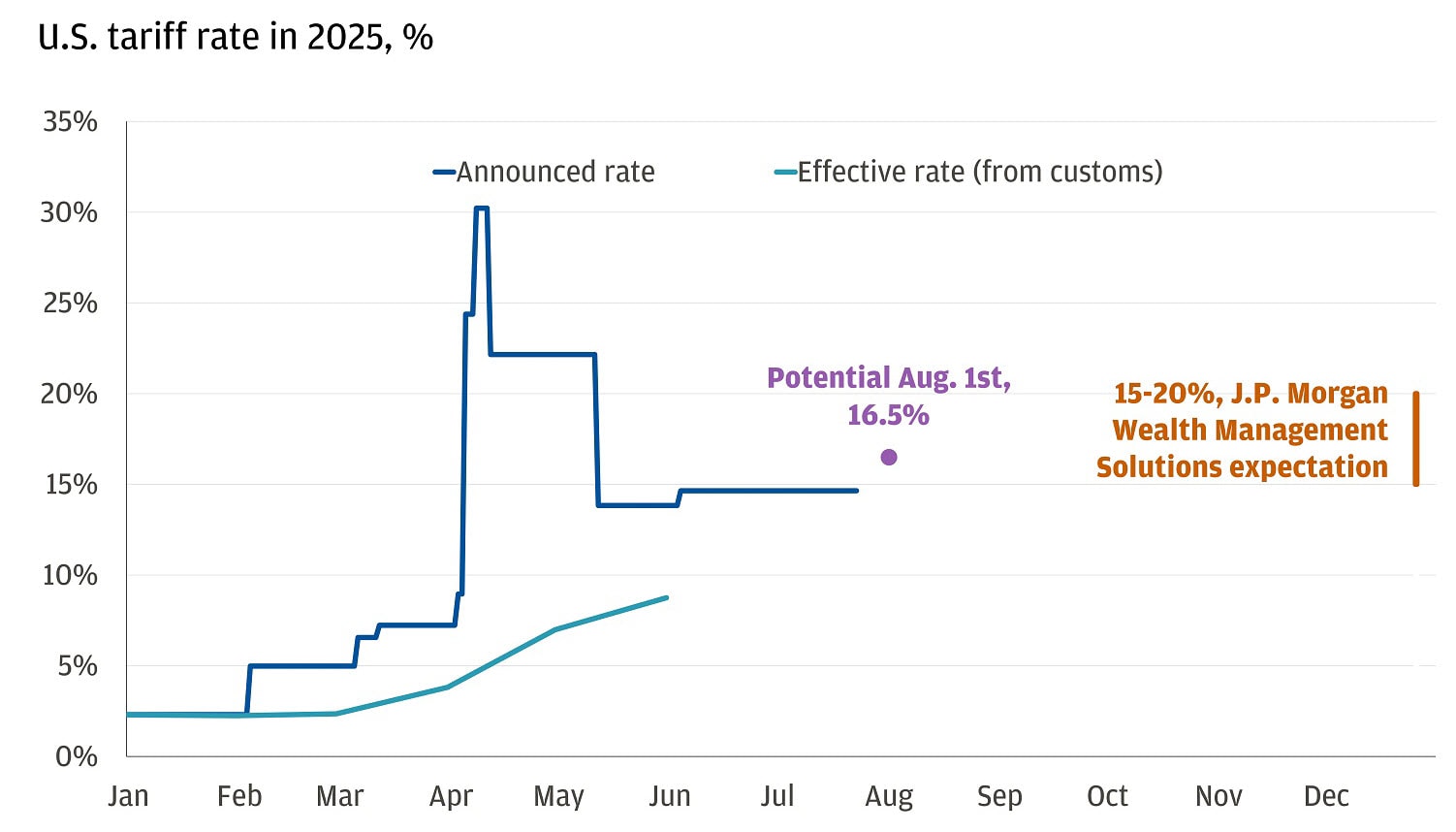

On top of that, the effective tariff rate is around 8% as of June, far below the announced rate of roughly 17%.

Tariff collections lag announcements

Our take: While businesses may try to raise prices to pass on costs to consumers over the long term, wider margins have allowed them to absorb some of the burden, easing the impact. Given the latest deals and announcements from the White House, we believe the effective tariff rate could settle in the 15% to 20% range. We think that will continue to be manageable for markets.

2. Companies are adapting fast.

Initially caught by surprise after liberation day, S&P 500 companies issued the most downward revisions to earnings guidance since 1Q 2014. The C-suites were bracing for impact. Yet Q1 2025 earnings defied expectations, with 78% of companies exceeding estimates – surpassing both the five and 10-year averages.

As Q2 2025 earnings roll in, it’s clear that companies have had four months to prepare. Earnings beats are running at about 6% to 7%, with 79% of companies surpassing estimates. Seeing is believing, and we find comfort in a couple of examples from this week – a tale of two cities, if you will:

- General Motors faced a direct impact from tariffs, reporting a $1.1 billion hit that affected their full-year guidance by $4 to $5 billion. Despite this, their adjusted earnings per share (EPS) exceeded estimates due to higher revenue and improved international profits.

- Johnson & Johnson, on the other hand, initially forecasted a $400 million tariff hit for 2025 but cut that to $200 million in their Q2 2025 earnings report. Also, they reported Q2 sales and adjusted EPS that topped expectations and raised full-year sales guidance. They absorbed the $200 million hit thanks to wide margins, announced a $55 billion U.S. investment to reduce import dependency and implemented cost control initiatives to counter inflation and tariffs – that’s what preparation looks like.

On the flip side, a weaker U.S. dollar has been an unforeseen tailwind, boosting earnings. Companies like PepsiCo, Coca-Cola and Netflix are among those beating estimates, thanks in part to currency tailwinds that have lifted revenue and offset cost pressures.

Our take: Coming into the Q2 reporting season, expectations for earnings per share were modest, with 5% year-over-year growth penciled in – the slowest in two years due to March and April revisions. But a low bar is easier to beat. Over the past year, S&P 500 companies have exceeded earnings estimates by 6.3% on average. This trend has boosted the earnings growth rate by 4.6 percentage points. If applied to the starting point for Q2 estimates, actual growth could approach double-digit rates.

Earnings have surpassed expectations in recent years

Companies are navigating headwinds and adapting well to the fluid environment. With emerging policy clarity and diminishing downside risks, we anticipate continued strong corporate performance. Corporate America handled the Washington noise effectively in Q2 and they could perform even better now that the C-Suites have more insight into government policy.

3. Tariffs are not the only thing happening in markets.

Investors have been laser-focused on tariffs, but tariffs aren’t the whole market story. While politics have dominated the conversation over the past two months, Google’s monthly token usage more than doubled. In other words, Google’s artificial intelligence (AI) models are being used far more aggressively – what some call a hockey stick moment.

The punchline: AI usage is compounding and the productivity impact is already being felt.

- ServiceNow saved $100 million in hiring costs by automating workflows with GenAI. The CEO mentioned in their Q2 earnings call that they’re “doing more with fewer people without sacrificing growth.”

- AI is writing about 30% of all internal code at Microsoft, saving the company $500 million in operating expenses post-AI adoption in customer support and software engineering.

- IBM reported a 200 basis points of gross margin expansion in Q2 2025, citing productivity gains from AI.

- Our own JPMorganChase Chief Information Officer Lori Beer recently noted that an internal AI coding assistant has boosted developer efficiency by up to 20%, enabling engineers to focus more on strategic, high-value projects. Management estimates that AI could deliver $1 billion to $1.5 billion in economic impact annually.

Another underappreciated tailwind has been One Big Beautiful Bill Act (OBBBA), where provisions on research and development (R&D) expensing and favorable tax law changes are bolstering capex. Notably, hyperscalers are expected to invest around $360 billion this year alone.

Our take: It all starts with adoption. This reminds us of the late 1990s surge in productivity growth, which surprised many – driven in part by the widespread adoption of the internet and personal computers (PCs). We believe a revolution is underway and we’re only in year three. In the long run, AI will drive higher productivity, leading to higher gross domestic product (GDP) growth. Tariffs raise the hurdle; AI raises the bar. Overall, higher productivity can lead to incremental revenue and increased government revenues.

Amidst all the policy changes, remember that the administration’s intent isn’t to cause a recession. Beneath the surface, tariffs haven’t been as bad as expected – a 15% to 20% tariff rate on paper has translated to about an 8% rate in practice. Consumers are holding up, earnings have surprised to the upside and positive catalysts are on the horizon. Markets don’t need an "all clear" to move forward; they need solid fundamentals and a bit more clarity. Corporate America is stepping up. Risks are real, but so is resilience.

All market and economic data as of 07/25/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

Global Investment Strategist