5 things working in markets today

Market update

This week saw a dramatic swing in market sentiment as investors shifted from the brink of geopolitical chaos to near elation over potential Federal Reserve (Fed) cuts.

By Saturday, the Israel-Iran conflict had escalated with U.S. bombers targeting key nuclear sites, raising fears of a global crisis. Yet, a ceasefire was announced and nuclear talks are set to begin, easing tensions. Amid this uncertainty, European NATO members pledged to boost defense spending to 5% of gross domestic product, a level not seen since the Cold War.

As geopolitical risks quickly faded, investor focus pivoted to the Fed’s dovish stance. The market now sees the central bank prioritizing the labor market over inflation, hinting at potential rate cuts sooner than expected. Investors embraced this proactive approach, viewing it as accommodating for the economy. Short-term bonds rose, while safe haven assets like gold and the U.S. Dollar declined, and global equities rallied – with the S&P 500 just five basis points shy of all-time highs – on positive momentum.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Spotlight

Investors are in a weird place right now – grappling with uncertainty while markets hover near all-time highs. The economy is fundamentally strong, with corporates enjoying robust revenue and Earnings Before Interest, taxes, Depreciation and Amortization (EBITDA) growth, low default rates, resilient consumers, a balanced labor market and inflation close to the Fed’s target.

Yet, the landscape is also shifting. Bears caution that the real disruption from tariffs and geopolitical tensions is yet to come. Meanwhile, markets remain fixated on the strong fundamentals. How should we cope with this dual reality? We believe the focus should be on the many aspects that are working right now in markets:

1. A diversified portfolio.

To boot, a global 60/40 portfolio is up +7.3% so far this year, showcasing its resilience.

There’s more proof of disinflation occurring despite tariff risks, central banks still maintain an easing bias and geopolitical risks fade.

Within U.S. equities, industrials (+10%), financials (+7%), utilities (+7%) and tech (+7%) have led the charge higher, with the last three being among our preferred sectors. We believe there’s more room to grow.

Bonds have delivered a solid performance halfway through the year, with the U.S. Bloomberg Aggregate up +3.6% and the Global Bloomberg Agg. up +2.6%. When markets were rattled by tariff fears, bonds performed even better.

Even if our base case doesn’t materialize, a diversified portfolio has proven its worth during growth scares. For instance, when the S&P 500 was down 15% year-to-date, a global 60/40 allocation was only down 6%. After all, bonds now offer something we didn’t see pre-pandemic: The potential for both income and hedging for growth scares.

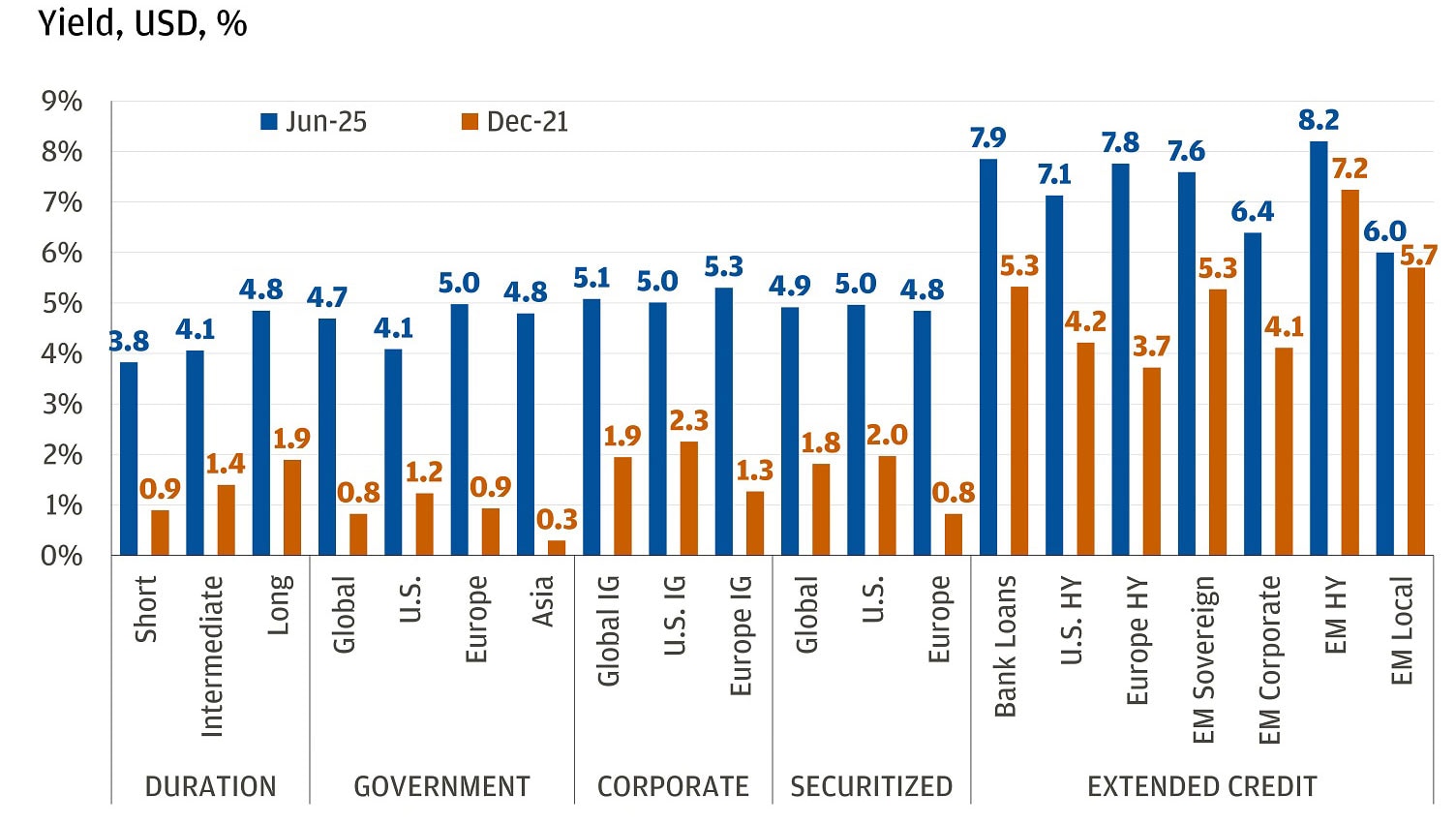

Rising yields have created more attractive entry levels for fixed income investors

2. Regional diversification.

Investors worldwide have shifted their focus away from U.S.-centric investing.

While the U.S. market has been buoyed by artificial intelligence (AI) and financials, the broader S&P 500 isn’t expected to see as much earnings growth. In contrast, Europe and China tech are showing breadth and resilience, highlighting their potential for continued growth.

Year-to-date, these regions have also outperformed the U.S., with a USD investor up +23% in China and +24% in Europe, compared to just +4.4% in U.S. equities. Although these markets were perceived as more sensitive to tariff and geopolitical risks, recent catalysts have demonstrated their resilience and potential for continued growth.

3. Bank stocks.

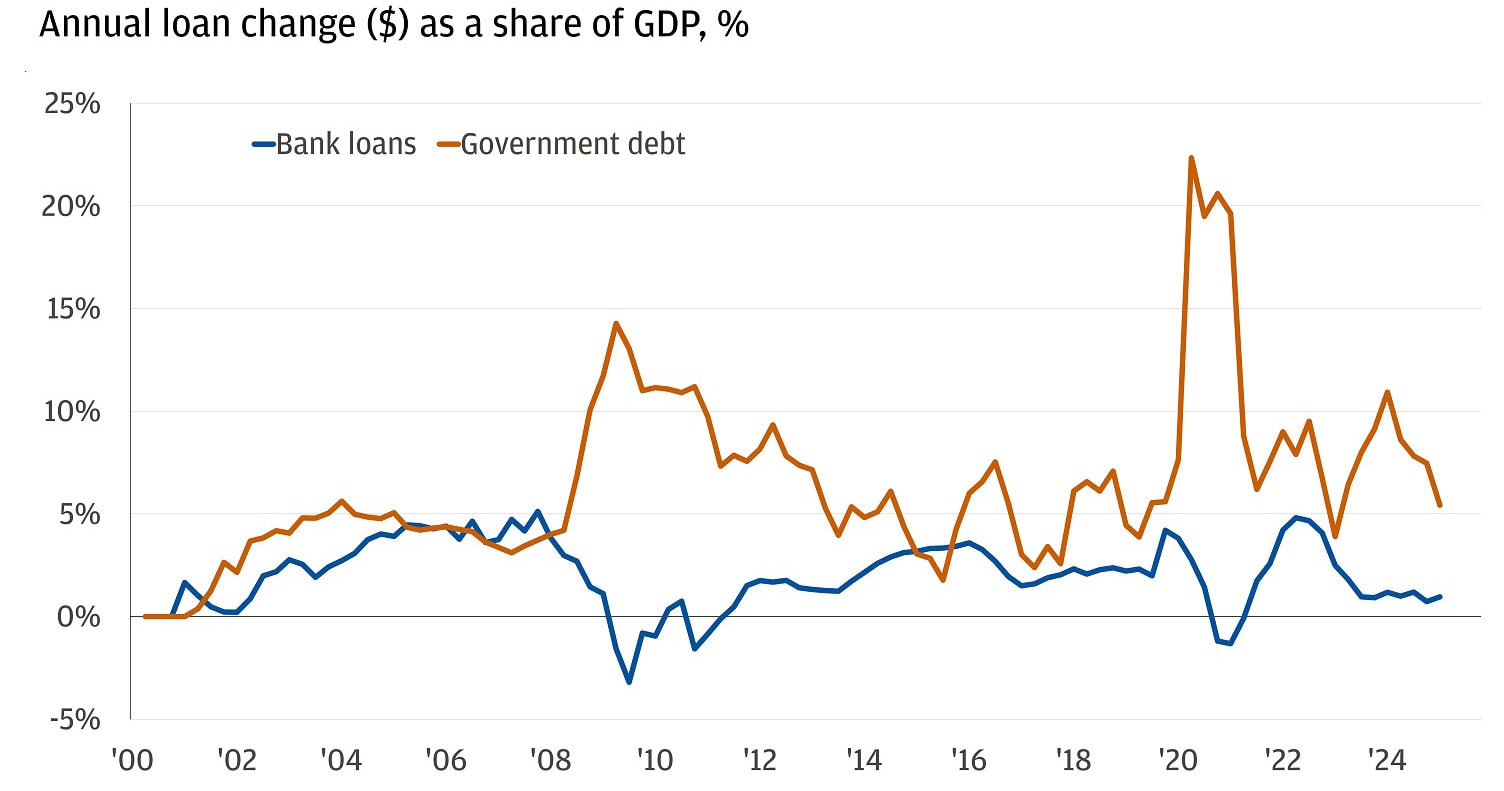

Deregulation is here. This week, the Federal Reserve proposed easing leverage requirements for banks, lowering the supplementary leverage ratio (SLR) from 5% to between 3.5% and 4.5%. This change could allow banks to use their excess capital more effectively.

The ongoing conversation around bank deregulation presents a promising opportunity for the U.S. banking sector. With softer regulations, banks can enhance profitability through increased market activity and reduced regulatory costs.

The financials sector, up about +7% this year, stands to gain further from these changes. To boot, deregulation could enable banks to deploy around $200 billion in excess capital, which we expect will boost the economy through increased buybacks and loan growth. Interestingly, government debt growth has outpaced bank lending since the financial crisis, and we believe this shift will likely accelerate loan and economic growth.

Government debt growth has exceeded bank lending since the Global Financial Crisis

4. Recent IPOs.

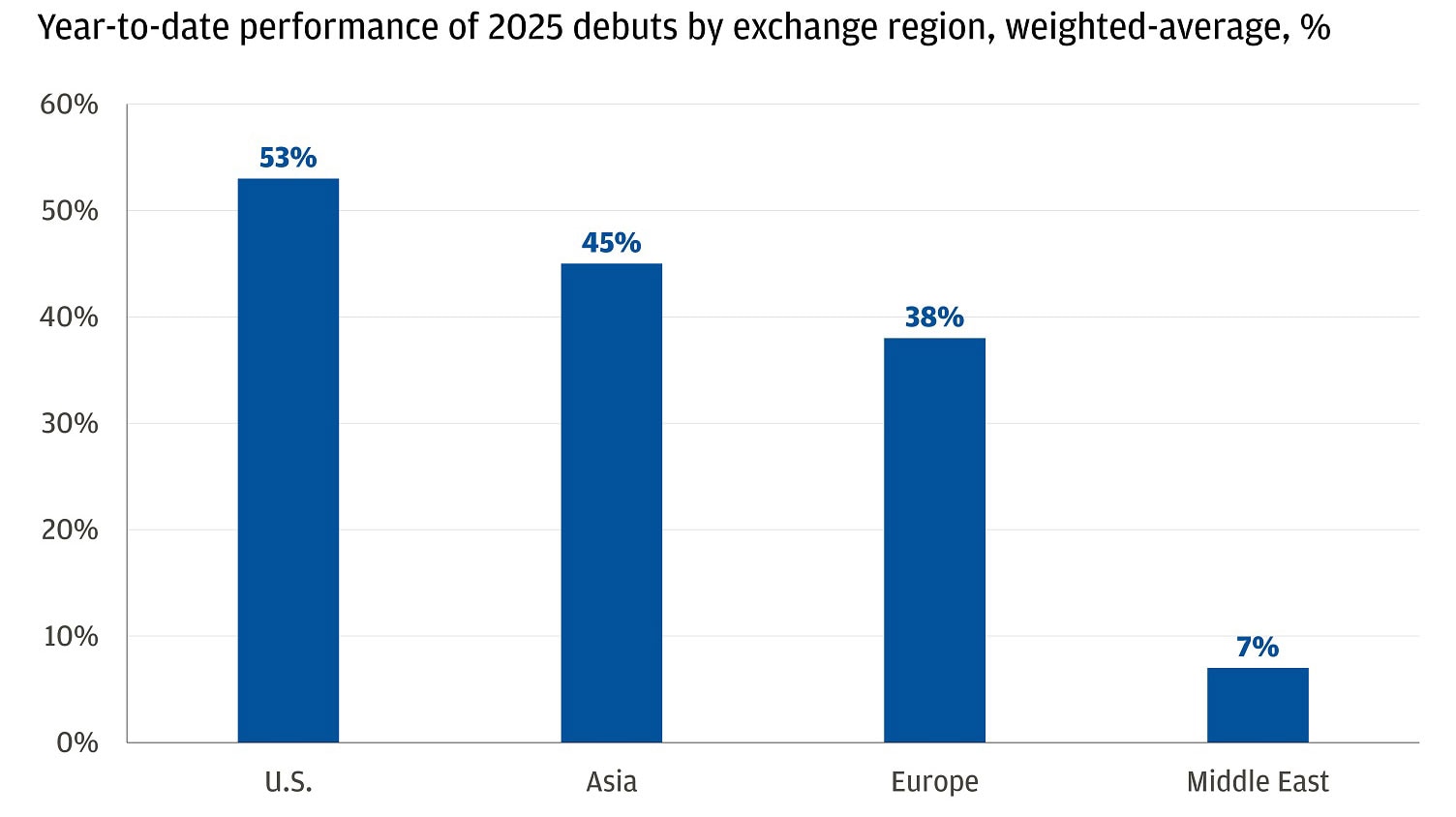

Up until recently, initial public offering (IPO) activity was blocked at the top of the funnel, but now the dam is starting to burst. Recent high-profile IPOs like Circle (+598%) and CoreWeave (+295%) have been very successful, signaling a resurgence. In fact, May marked the strongest month for global IPO and M&A activity since May 2022, despite a post-Liberation Day slowdown.

Private equity-backed IPOs captured a record 55% of capital raised on major U.S. exchanges. At nearly the halfway mark of the year, IPOs on U.S. exchanges have raised $29.1 billion, up 45% from the same period last year. Notably, AI has seen about $150 billion in deal activity, up from $20 billion last year.

All that being said, two of the year’s five largest IPOs on U.S. exchanges are trading up by a weighted average of about 53%, leaving investors eager for more. As rates decline and deregulation unfolds, we expect this momentum to continue.

U.S.-listed companies deliver outsized returns after IPO

5. Long-term themes like defense.

On Tuesday, many major defense stocks experienced a classic ‘buy the rumor, sell the fact’ move after a ceasefire between Iran and Israel went into effect, with Northrop Grumman, RTX and Lockheed Martin all declining over -3%. However, the S&P 500 aerospace and defense sector remains robust, up over 22% year-to-date. Palantir, a defense application software company, leads the S&P 500 with a +93% year-to-date gain.

While the perceived risk of further escalation in the Middle East may be low, we continue to view the defense sector as a strong long-term trend. This week alone, European NATO members pledged to boost defense spending to 5% of GDP, a level not seen since the Cold War.

This shift in defense spending will extend beyond traditional defense, benefiting areas like power, infrastructure, supply chains and cybersecurity.

All in all, we’re in a catalyst-heavy period for markets, with tariffs, taxes, geopolitics and more in play. Our focus is on helping investors feel more comfortable in an uncomfortable market.

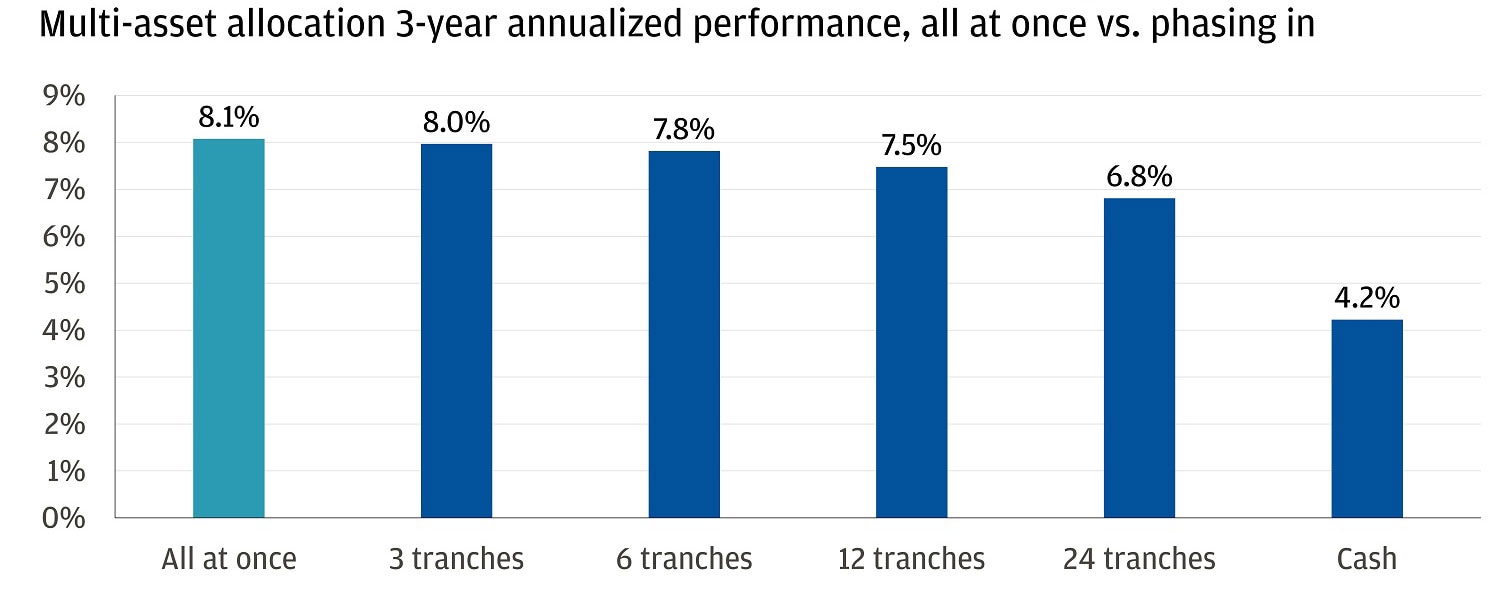

If you’re still hesitant to invest right now, a phasing-in strategy could help you feel more comfortable. A consistent phasing-in approach has typically outperformed staying in cash and reduced return variability.

Phasing-in historically meant giving away some returns, but is still better than staying in cash

All market and economic data as of 06/27/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.