Investing in equities? 3 key questions to consider

Global Investment Strategist

This week delivered the last big read before next week’s Federal Reserve (Fed) meeting: Inflation came in right on target, keeping rate cut plans on track. Investors now lean toward three 25-basis-point cuts by year-end, while the S&P 500 hit new highs.

On the labor side, conditions softened further. The Bureau of Labor Service’s (BLS) benchmark revisions lowered the count of jobs added between March 2024 and March 2025 by about 911,000 as new unemployment claims rose to the highest level in almost four years.

In short: The inflation readings suggest that tariff-related price pressures are slowly working through the economy (not as a disruptive spike) and the labor market has clearly softened. With that backdrop, the Fed has the green light to lower rates.

What does that mean for investors? As we laid out last week, we’re working through a simple three-part playbook:

- Embrace carry in fixed income

- Position for risk-asset outperformance

- Diversify internationally

Today, we focus on “positioning for risk-asset outperformance.”

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Why does a potential Fed rate cut favor equities?

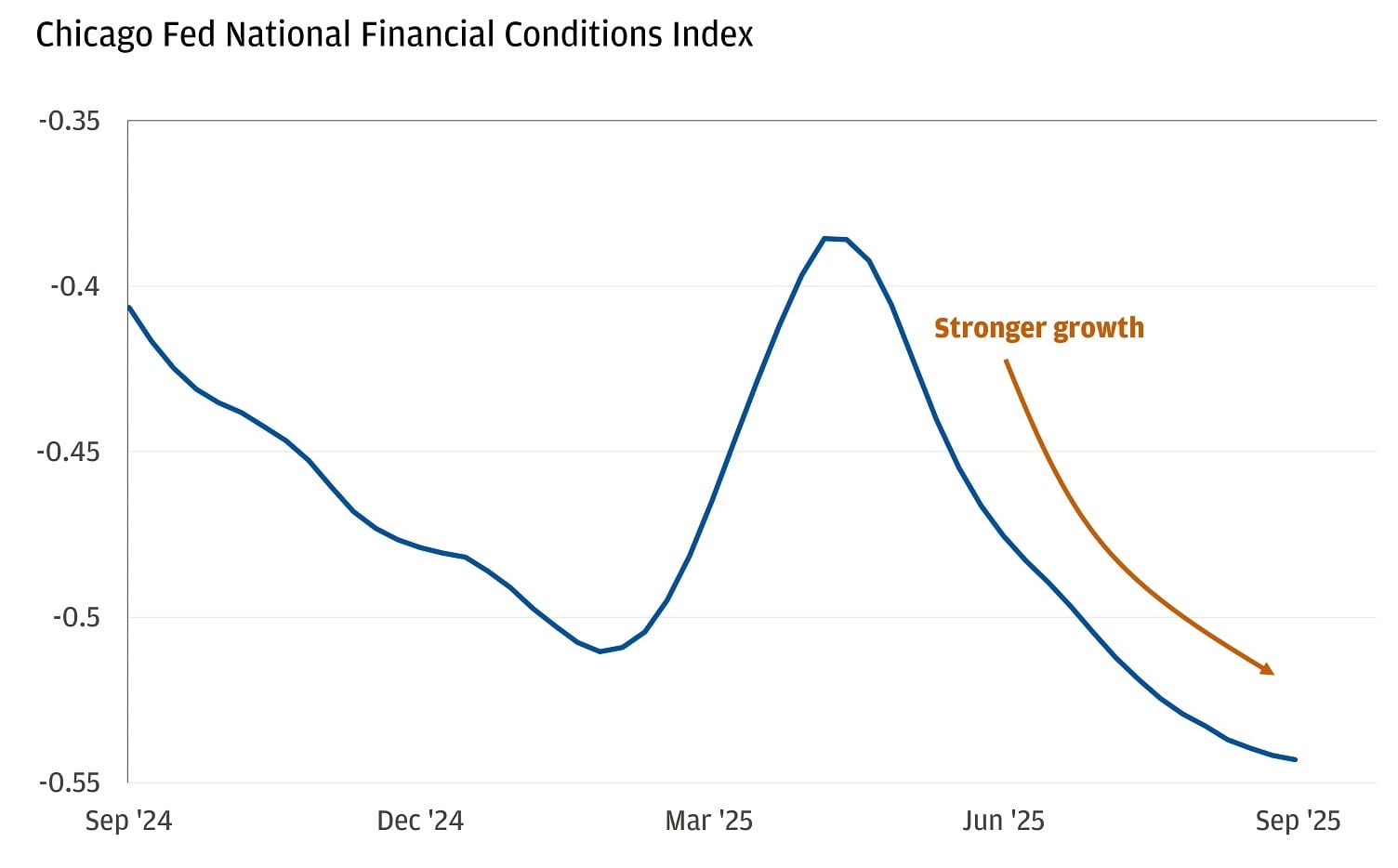

First and foremost, these cuts should provide a modest but meaningful boost to growth. We think the Fed is cutting to ease financial conditions, not because a recession is looming – an ideal scenario for stocks. Beyond the policy rate dropping, this contributes to easier financial conditions – the mix of market rates across the curve, credit spreads, equity levels, the dollar and even market volatility. Economists summarize that mix in financial conditions indexes: When they ease, they tend to support growth in the year ahead. By that framework, today’s combination of lower market rates, a softer dollar, tight credit spreads and firm equity markets points to a boost of roughly 50 basis points in gross domestic product (GDP) over the next year.

Easing financial conditions point to modest growth

Three key questions to consider before putting money to work in equities

Are valuations too high?

Valuations may be high relative to history but they seem justified. At about 22.5 times next twelve months (NTM) earnings, the S&P 500 sits near levels last seen in the late 1990s/early 2000s. Two facts underpin the valuation:

- The index constituency changed. Technology and communication services – home to most of the hyperscalers – now account for a far larger share of market cap and profits than in past cycles. Tech alone is roughly 33% of market cap (versus roughly 15% 20 years ago) and about 25% of profits (versus roughly 12% in 2005). By our estimates, that mix shift – especially the higher tech weight – adds roughly three multiple turns. Said differently, the S&P 500’s forward price-to-earnings (P/E) moved from about 17× in 2005 to around 22.5× now and more than half of that change is explained by mix.

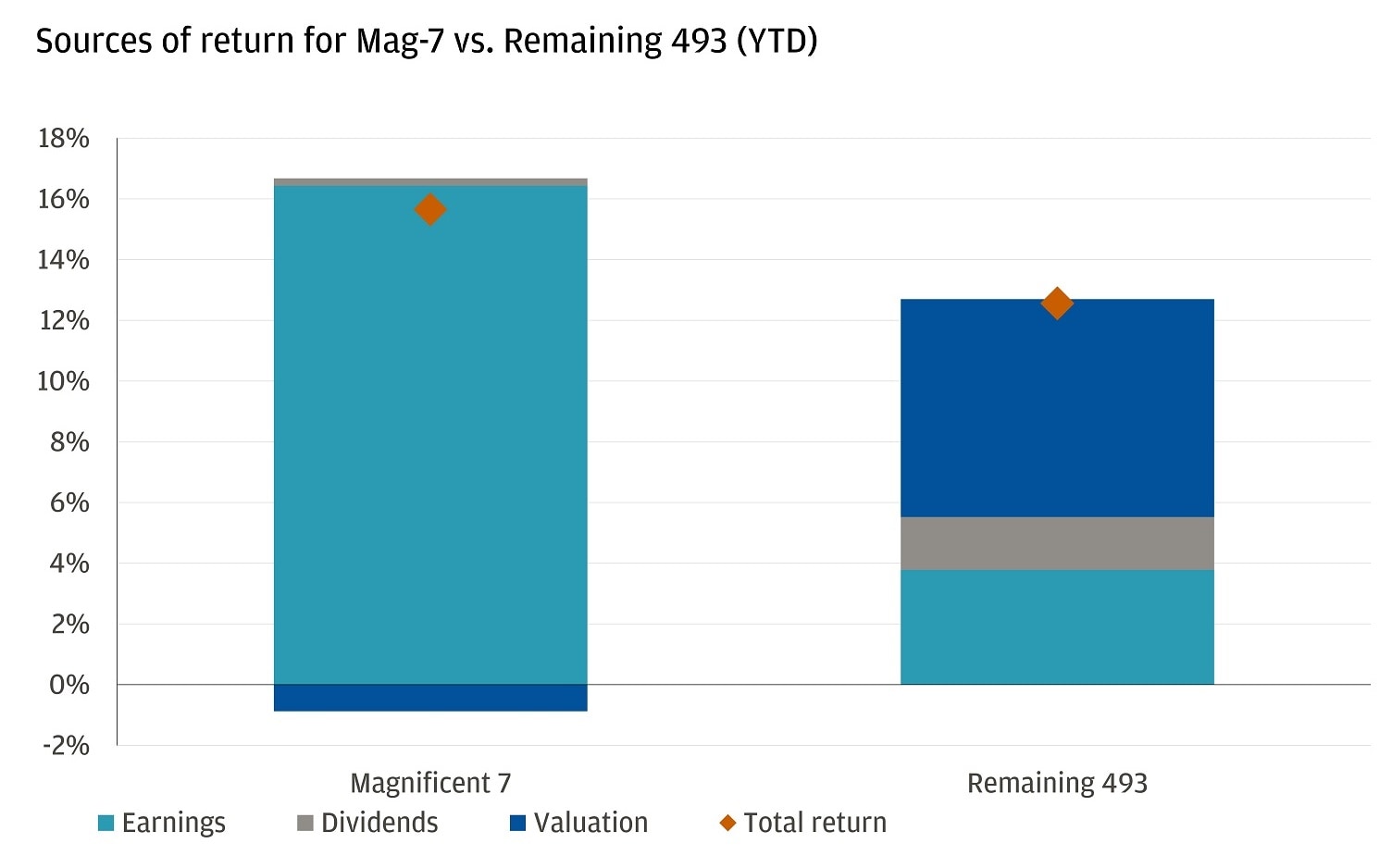

- Earnings and earnings expectations. A higher multiple can be reasonable if the “E” is still moving up – and it is. For this year, the Magnificent 7 (Mag-7) are expected to grow earnings about 21%, down from roughly 40% last year but still ahead of roughly 8% for the other 493 companies. That said, looking ahead to 2026, consensus has the Mag-7 up about 15%, versus closer to 12% for the other 493 – a narrower gap that helps the earnings base broaden over time.

Our take: This isn’t the same index. It’s more tilted to faster-growing, high-margin, cash-generative businesses and less to capital-intensive cyclicals. If real borrowing costs ease with policy, that lowers the discount on future cash flows and helps support today’s valuations. Combine that mix with healthier balance sheets, ongoing buybacks, limited new issuance, an earnings path that still trends up and a higher forward multiple can be sustained rather than hoped for.

Is there too much concentration?

True, the index is historically concentrated but it’s for the right reasons. The top 10 stocks are about 40% of the index and have driven most of this year’s earnings growth; the Mag-7 are compounding profits at roughly two times the pace of the rest. That makes concentration largely an earnings story, not just a multiple story.

Our view: While longer term we expect a broader set of artificial intelligence (AI) winners across size and sector, incumbents are likely to lead the charge over the next 12 to 18 months as deployment ramps.

Earnings underpin Mag-7 returns

There are pockets of froth, though. Not every leader will keep growing at the same clip and in a market this well-owned, there isn’t much room for error. That’s where selectivity matters: recognizing which names still have durable cash-flow runways – and which don’t – while sizing exposure so winners don’t overwhelm the portfolio.

When does capital expenditure (capex) investing become a concern?

There’s an AI build-out underway, and the numbers are big – no new news here.

Meta now guides $66 to $72 billion of 2025 capex and says 2026 will be another year of significant growth. Nvidia’s leadership has framed industry-wide AI infrastructure needs at $3 trillion to $4 trillion by the end of the decade. All in all, recent trackers put hyperscaler capex around $370 billion in 2025 (about +44% versus 2024) and more than $400 billion in 2026 as deployments ramp. For context, that’s almost double that of the U.S. federal research and development budget (roughly $180 billion to $200 billion a year).

So, when does it become a concern? When spend outruns payoff – we’re watching three main variables: Revenue growth, operating margins and productivity.

So far for hyperscalers, revenues are rising, margins are strong and headcount hasn’t surged. Microsoft’s operating margins grew by four percentage points while revenue increased at the fastest pace in five quarters – and headcount growth was roughly flat. Similarly, Meta generated a strong acceleration in revenue growth to 22% year-over-year in Q2 2025, up from 16% in Q1 2025, while operating margins continued to expand with modest headcount growth. Point being, even as they spend, profitability remains high and productivity is improving.

In all, we believe global equity markets will continue to rally, driven by an easing Fed, tax incentives and accelerated depreciation, AI and data-center spending, and investment in energy, grid and onshoring. In the multi-asset portfolios that we manage, we remain fully invested in equities diversified across geographies and sectors, including technology and financials.

All market and economic data as of 09/12/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

For important disclosures, please refer to the Disclosures section for detailed information.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist