In the rear view: How did our 2025 themes pan out?

Markets cheered the end of the longest government shutdown in history. U.S. equities rose on news of a deal before losing their gains later in the week, weighed down by losses in megacap tech due to jitters around artificial intelligence (AI) spending.

Investors are now waiting with bated breath for a wave of economic releases in the coming weeks, which will help inform the Federal Reserve’s (Fed) decision at the December meeting. Right now, it’s basically a coin toss whether we’ll see a rate cut.

We’re excited to release our 2026 Outlook on Monday. Before we do, let’s take a look back at our last Outlook and how our views played out.

Six months ago, our 2025 Mid-Year Outlook encouraged getting comfortably uncomfortable – staying invested, but adding resilience. At the time, uncertainty was high: tariff swings, a noisy policy path and a tug-of-war between easier financial conditions and sticky inflation.

Our call was that the economy would muddle through the soft patch, avoid a recession and support market gains.

Markets have since climbed the wall of worry into an everything rally: Gold (+26%), emerging markets (+23%), S&P 500 (+16%), Euro Stoxx 50 (+16%) and global aggregate bonds (+7%) all surged – outperforming cash (+2%). We laid out five pillars to guide the rest of the year – here’s a scorecard of what we said, what happened and what we learned:

We said the economy would power through uncertainty. Shock absorbers worked, and tailwinds steadied the ship.

With good reason, investors were nervous. There were clear causes to fear – tariffs, immigration and legal uncertainty – and real reasons to cheer including deregulation and pro-business policies.

Our view then: We expected tariffs and policy uncertainty to weigh on parts of the economy but believed strong corporate profit margins, healthy labor markets and the AI-driven capital expenditure (capex) cycle would act as shock absorbers. Our call was that growth would bend, not break and that secular tailwinds – especially AI – would help the economy stabilize as we headed into 2026.

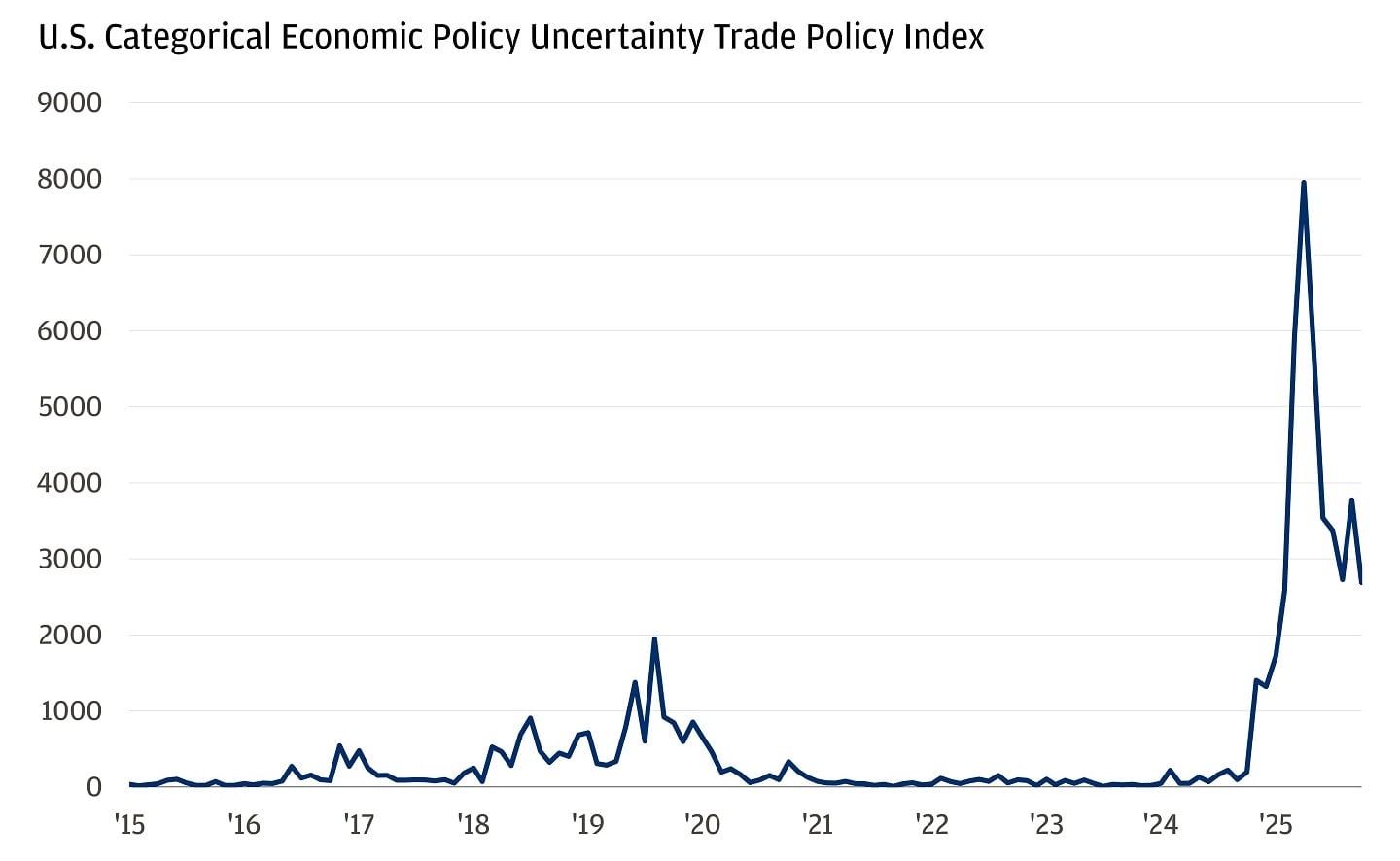

Tariffs weighed on parts of the economy, with hiring slowing sharply and trade policy uncertainty spiking. But by late summer, markets moved on, embracing the AI investment cycle and looking ahead to support from easier monetary policy and One Big Beautiful Bill Act (OBBBA) benefits. Much of the investment concentrated in AI, especially among hyperscalers, helped drive half of 2025 gross domestic product (GDP) growth from capex and investment.

Trade uncertainty spiked this year

The punchline: Tariffs were a headwind, but growth persisted – driven by AI and easier policy. As we expected, these forces should help the economy stabilize into 2026. While tariffs remain a source of uncertainty, markets are pricing in limited disruption, and the economy continues to show resilience.

We warned that stickier inflation would challenge portfolios. Above-average inflation now threatens to erode returns.

We highlighted a regime shift: Low inflation and rates have given way to two-way risks and persistent policy uncertainty.

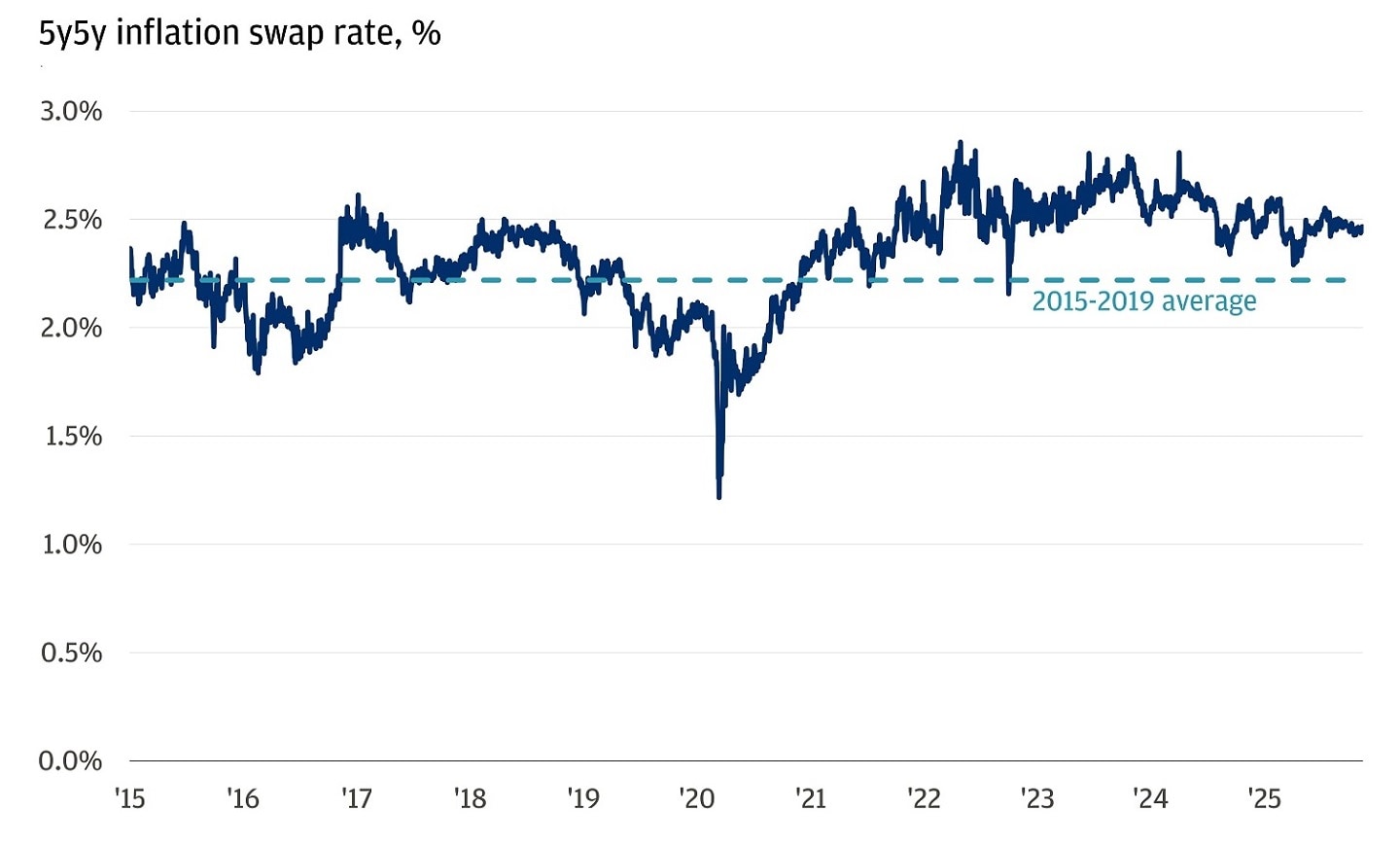

Our view then: Inflation following the height of the COVID-19 pandemic pushed prices higher – not necessarily a direct risk to markets, but a real challenge for portfolios. Despite the uncertainty, we believed the Fed would be able to cut rates. With that backdrop, portfolio diversifiers that don’t move in tandem with other assets and can outperform cash on their own were (and continue to be) the goal – such as gold.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Inflation from the 2021–2022 period has left expectations elevated and made it even more important to insulate portfolios from stickier, more volatile inflation and the positive correlation between stocks and bonds. Tariffs provide upside risks going forward, though a surge in inflation is not our base case. The Fed has resumed cutting rates despite the above-target inflation, and gold has rallied nearly 30% since our Mid-Year Outlook.

Swaps are signaling higher inflation in the years ahead

The punchline: Inflation rose, leading to a positive correlation between stocks and bonds – not a threat to markets, but a real challenge for portfolios. While we didn’t expect this to broaden out, and we still don’t, inflation remains a persistent risk to personal wealth. Holding large cash positions in this environment can quietly – and permanently – erode real wealth, which is why we continue to emphasize diversification as we look ahead to 2026.

We saw a dollar downtrend, not downfall. The downtrend played out, and the dollar is still a global anchor.

The dollar’s supremacy was called into question, especially after “Liberation Day” triggered a broad sell-off in U.S. assets – leaving investors to wonder if this was a temporary dip or something more structural.

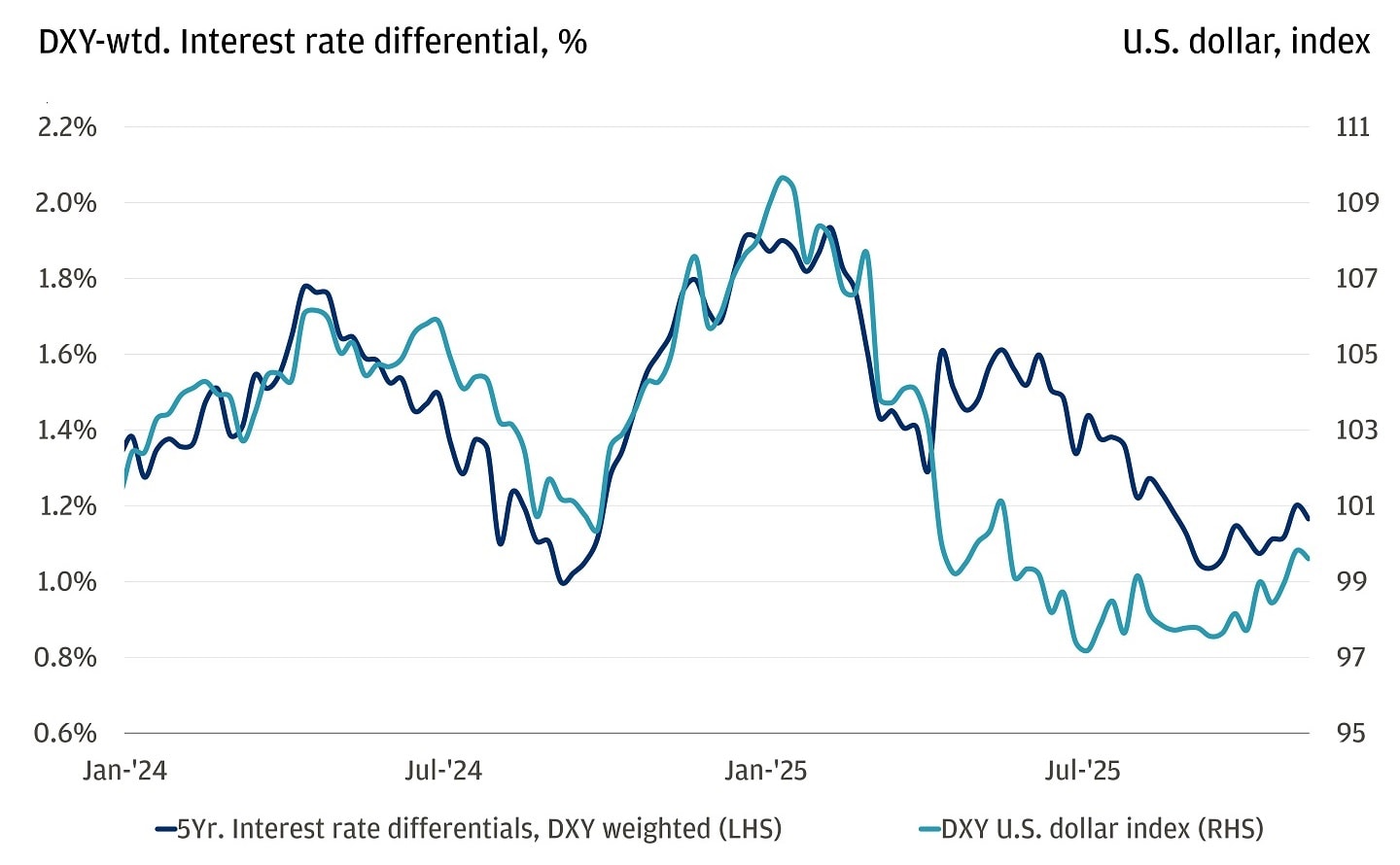

Our view then: We saw this as a downtrend, not a downfall. Our models had flagged the dollar as overvalued for years, and we expected a cyclical depreciation driven by slower growth, outflows from U.S. assets and lower rates. The dollar’s role as the system’s anchor remained intact.

The dollar is now down about 8%, reflecting softer growth expectations for the U.S., narrowing rate differentials, and stronger economic activity abroad. The outflow from U.S. dollar assets has played out, and we expect interest rates to drive currency moves over the next year. Diversification remains our call to action, with notable gains in Europe and emerging markets like Taiwan and South Korea.

Interest rate differentials are again driving the USD

The punchline: We said “downtrend, not downfall” – the dollar would lose some shine but remain the system’s anchor. Since then, that call has played out. Looking ahead, we expect it to remain range bound around current levels.

We didn’t overlook AI during the tariff tantrum. The AI theme has only accelerated.

Six months ago, AI had faded from the spotlight as tariffs dominated the conversation and AI-linked stocks led the March slide.

Our view then: Don’t overlook AI just because it’s not grabbing headlines. The build-out is ongoing, costs keep falling and capabilities keep rising. We saw lasting opportunity in the broader ecosystem – semiconductors, cloud and data-center infrastructure, software and “old economy” enablers like power and networking.

Strength and momentum around the AI theme were far from over. Since June 1, we’ve seen 11 major AI infrastructure deals, with nine disclosed totaling nearly $500 billion in potential spend – led by OpenAI, Nvidia and Amazon Web Services (AWS). The technology sector has nearly doubled the returns of the S&P 500 over the same period, underscoring just how powerful this theme remains.

AI has pushed tech stocks ahead of the pack

The punchline: Even with all the noise and a normalizing economy, the broader AI space surged. As tariff fears faded, markets shifted back to what matters most: fundamentals, capex and profit growth across the AI value chain.

We said the deal machine was down, not out. Dealmaking is now going strong.

Heading into President Donald Trump’s second term, expectations for capital markets activity were high, but once he took office, pro-business hopes were disappointed by a pause in dealmaking.

Our view then: We argued the deal machine was down, not out. Higher rates and policy uncertainty slowed mergers and acquisitions (M&A), initial public offerings (IPOs) and buyouts, but a healthier equity backdrop, open credit markets and a huge stockpile of dry powder set the stage for a rebound once the rate path and political landscape became clearer.

That’s exactly what played out. So far this year, global deal value has reached $3.8 trillion, with the first three quarters up 35% from the same period in 2024. We’re also on track for the largest number of $30 billion-plus deals ever.

The punchline: Visibility and political clarity brought dealmaking back to life. With fundamentals back in focus, we’re on track for the second-best year ever for global deals.

The bottom line

Stepping back, our mid-year playbook held up: The economy bent but didn’t break, AI remained an earnings engine, dealmaking thawed, tariffs showed up more in prices than in growth and dollar weakness has mostly played out. The core message is unchanged: Stay invested, stay diversified and use volatility to upgrade portfolios – not to sit on the sidelines.

Stay tuned for our 2026 Outlook: Promise and pressure next week, where we’ll highlight the key drivers for the year ahead.

All market and economic data as of 11/14/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.