Proximity matters: 5 things to know about the US sphere of influence

A fragmented world is reshuffling priorities – and security is back on top. In the first two weeks of the year, the U.S. carried out a dramatic operation in Venezuela, spotlighted Greenland as a strategic imperative and seemed to consider potential action in Iran. Put together, these actions signal a fundamental shift: Proximity matters.

History has a name for this mindset. The Monroe Doctrine once drew the line in the Western Hemisphere, positioning the U.S. as its dominant power. Though today’s context is different, the logic holds: Secure the perimeter, reduce spillovers and limit external influence. From the last year of protectionist measures to the latest more interventionist foreign policy pursuits, the U.S. seems to be taking steps to assert its power, especially among its neighbors.

This shift is indicative of increasingly pronounced global fragmentation – one of the three pillars in our 2026 Outlook: Promise and Pressure. The age of cost efficiency and globalization is pivoting toward a new paradigm of security, resilience and capital-intensive innovation – each force fueling the next through ongoing investment, resource scarcity and rising structural costs.

Here are five things to know about what this means for U.S. neighbors and for markets.

The U.S. wants a secure backyard – and the Monroe Doctrine is a blueprint

It seems even 200-year-old playbooks can still call the shots. The Monroe Doctrine stretches back to 1823, when then-U.S. President James Monroe took a policy stance that, in essence, drew a line between the “Old World” and the “New World” of the Western Hemisphere. The intention was to issue a warning to European powers against interference in the Americas and, in turn, promote U.S. political and economic interests.

Today’s version isn’t a history lesson. It’s a modern security posture. For years, U.S. foreign policy has largely deprioritized Latin America, focusing instead on the Middle East and then Asia. That’s why the so-called “Donroe Doctrine” – a reference to the revival of the Monroe Doctrine under President Donald Trump – has gained traction as a framework of U.S. foreign policy. However, rather than a defensive posture, the new doctrine moves further to an offensive assertion of U.S. power – for military security, economic benefit and expelling influence from certain countries.

Venezuela is evidence that the U.S. will put muscle behind its words

Secretary of State Marco Rubio has characterized the U.S. strike on Venezuela and Nicolás Maduro’s capture not as an invasion, but a “law enforcement operation.” But terminology aside, the U.S. has demonstrated that it’s willing to use force for security aims.

The rationale isn’t new: The U.S. has long worried about Venezuela’s ties to corruption, drug trafficking and Iran-linked actors like Hezbollah. China’s deep lending and energy ties, as well as Venezuela’s role in helping Russia avoid sanctions, only add to the sense that the country is now seen as a strategic, not just economic, problem.

This goes beyond Venezuela – focus is already on Greenland and Latin America broadly

The messaging is broader than Venezuela. Across Latin America, Trump referenced Venezuela as a precedent to ramp up pressure elsewhere, threatening action against cartels in Mexico and Colombia over drug trafficking and issuing Cuba an ultimatum to “make a deal or face the consequences,” with Venezuelan oil flows to the island on the line.

Meanwhile, Greenland has been the subject of rhetoric from a number of U.S. officials, and Trump even called anything short of U.S. control “unacceptable.” The island’s strategic position underpins U.S. Arctic security through missile-warning and space-surveillance systems. Politically, President Trump has framed Greenland as a “large real estate deal” and a once-in-a-generation territorial opportunity.

Natural resources are a major incentive

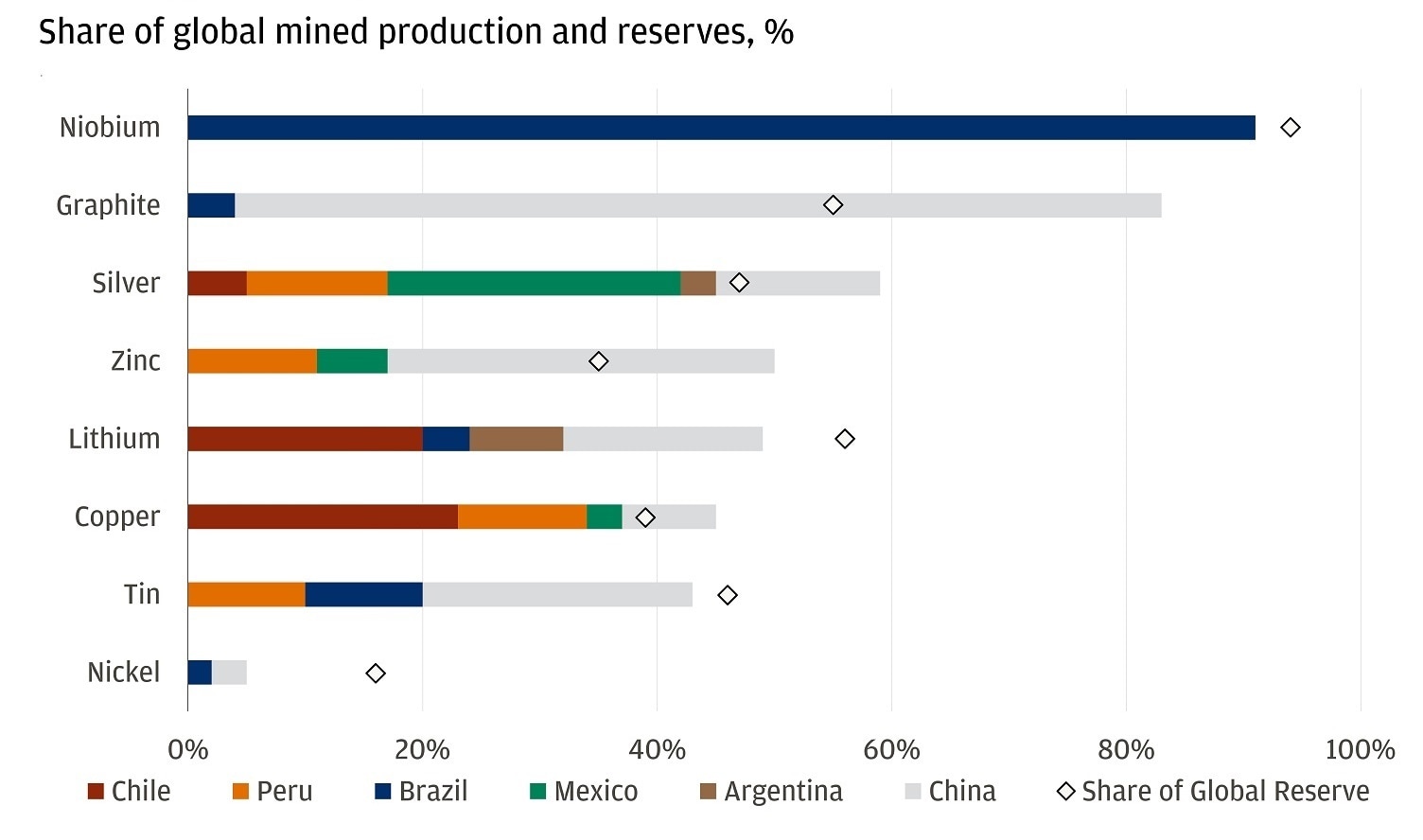

Latin America is increasingly seen as a supply-side powerhouse – at the heart of electrification, with the “lithium triangle” (Chile, Argentina, Bolivia) holding 60% of known global lithium and Chile producing over 20% of the world’s copper.

Latin American countries have a strong share in global mining for key minerals

Energy is the other big driver. Venezuela’s massive oil reserves – the largest proven reserves in the world – mean that if the U.S. can steer its supply, it would have influence over a quarter of global reserves, shifting the global energy chessboard, even if near-term gains take time and investment. The bottom line: Countries with the resources the world needs are rising fast on the U.S. priority list.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Geopolitical events usually impact commodities first

When global tensions rise, commodities are usually the first to react because their prices are closely tied to supply and demand. Any threat to oil, metals or other resources can send prices jumping quickly, reflecting the risk of quick supply disruptions – well before stock or credit markets respond.

Right now, the Middle East is adding another layer of uncertainty. Unrest in Iran and U.S. warnings of possible intervention have pushed oil prices higher. At the same time, markets are watching for a potential, but limited, supply boost from Venezuela – though it remains a small player in the global oil market.

The bigger risk we’re watching is the Strait of Hormuz. This narrow waterway is critical, with about 20% of the world’s oil passing through it. Given Iran largely controls this vital chokepoint, escalation of the current situation could raise the risk of a more acute supply disruption. That said, our commodities strategists see the risk of a Strait of Hormuz closure as very low. While Iran is a genuine source of uncertainty, history shows that oil shocks from regional conflicts are usually short-lived. We could see a temporary spike in prices, but a lasting impact would require a sustained disruption to Hormuz flows – which is not our base case.

The market impact of geopolitics tends to be short-lived

Meanwhile, metals have surged on a mix of safe-haven demand and lower rate expectations. Gold is at record highs, and silver is up 27% just in the first two weeks of this year. This is another example of why we’re adamant on building durable and resilient portfolios.

The bottom line

In a world where the rules are being rewritten, staying nimble and well-diversified isn’t just smart – it’s essential for navigating whatever comes next.

All market and economic data as of 01/16/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.