Expansion mode: 3 signs of resilience in the US economy

We put the odds of the U.S. staying in expansion mode in 2026 at 80% – including a 20% chance that the economy exceeds expectations and leads to a reacceleration of inflation. That’s not a “nothing can go wrong” call; it’s a strong vote of confidence in the resilience of the underlying economic environment.

That matters because 2025 gave investors plenty of reasons to doubt the outlook. Tariffs, immigration and policy noise fueled volatility and forced many economists to trim growth forecasts. Yet the economy kept moving – in Q3 2025, real gross domestic product (GDP) grew at a 4.3% annualized rate, far exceeding the initial expectation of roughly 3.3%. Our view is that this resilience extends into 2026.

The reason we’re comfortable leaning that way is that the key macro constraint is loosening, and it starts with inflation and the Federal Reserve (Fed). We anticipate inflation to remain rangebound (still above target, but not broadening to the stickier components), which should allow the Fed to maintain an easing bias. In fact, we’re anticipating one additional rate cut this year – not a signal of aggressive easing, but a move that keeps rates on a lower trajectory. That matters because it keeps financial conditions supportive.

With that backdrop, here are three reasons why we think growth will stay supported in 2026:

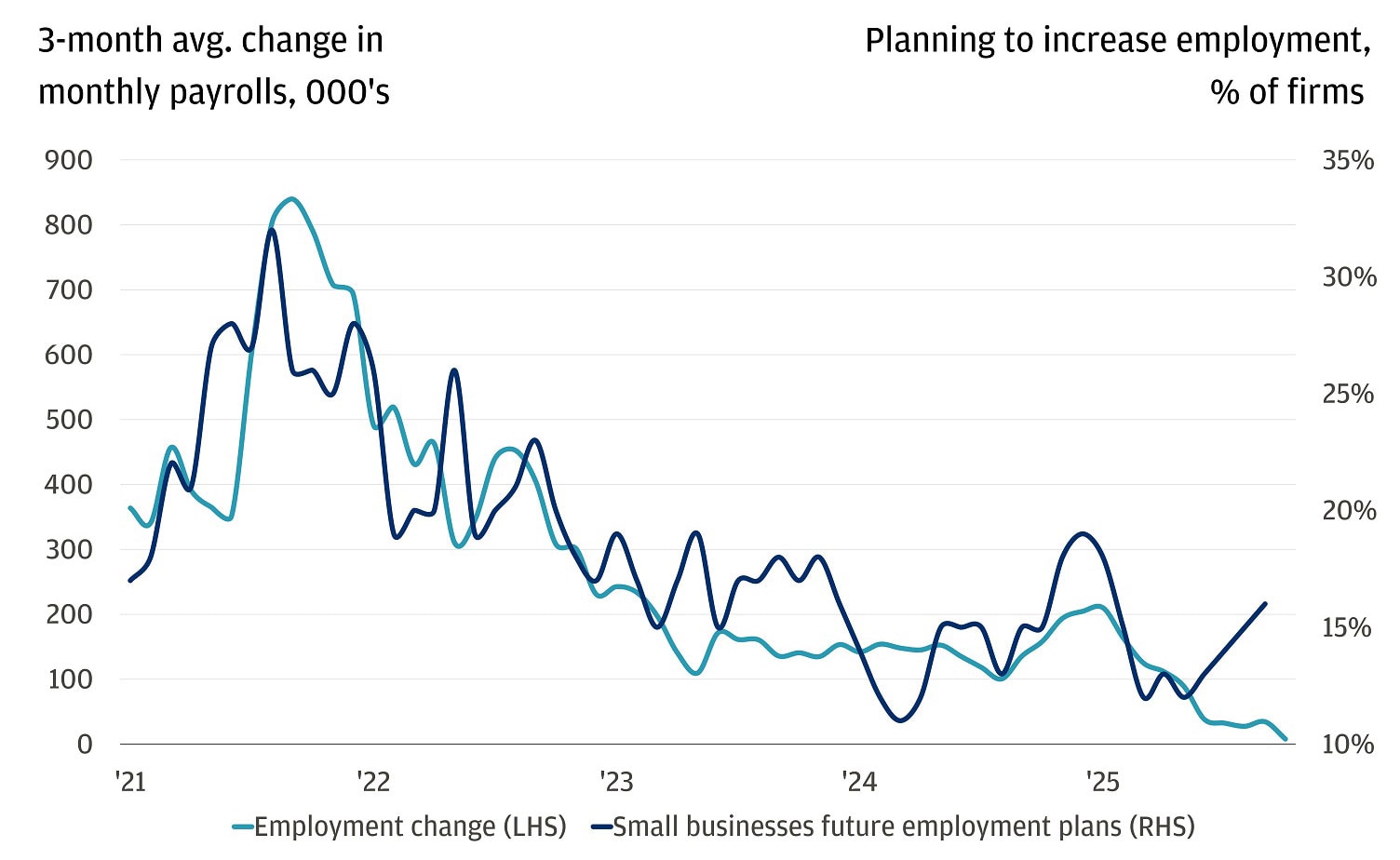

We expect the labor market to improve from here

Even though labor demand remains weak, further deterioration is unlikely because margins are near historic highs, talk of job cuts is limited and early signs of small-business hiring are emerging. Lower rates and steady real incomes should help stabilize conditions. The labor market doesn’t need to get red-hot; it just needs to stop sliding. We believe it will.

Labor market weakness showing signs of troughing

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

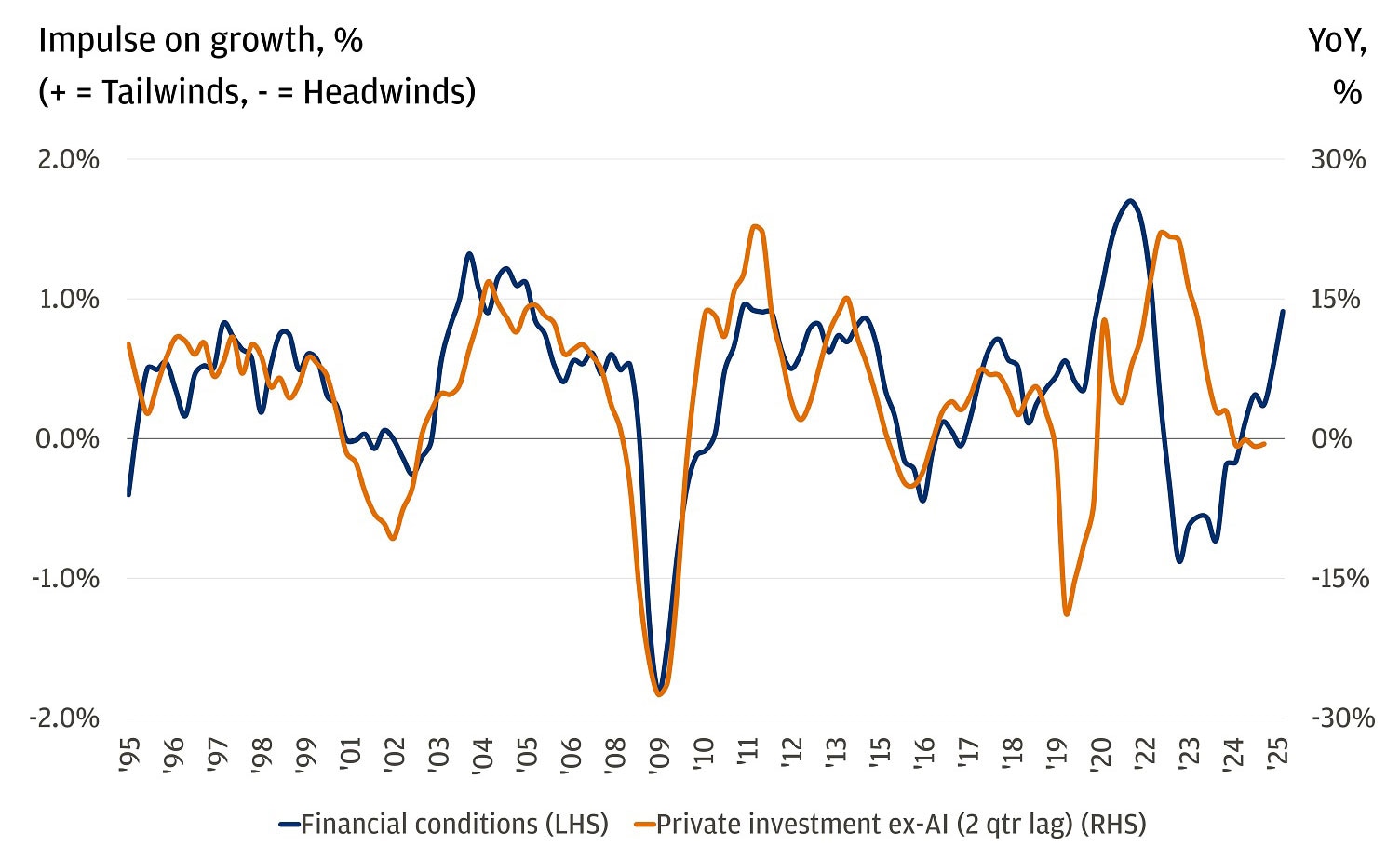

Capital expenditure keeps the cycle moving (artificial intelligence is the headline, but not the whole story)

The investment impulse looks durable, and easier financial conditions help extend the runway. Artificial intelligence (AI) capital expenditure (capex) is a meaningful driver, but capital expenditures beyond AI – from transportation equipment and industrial machinery to nonresidential structures – are expected to expand in tandem with easier financial conditions.

Easier financial conditions should bolster ex-AI capex

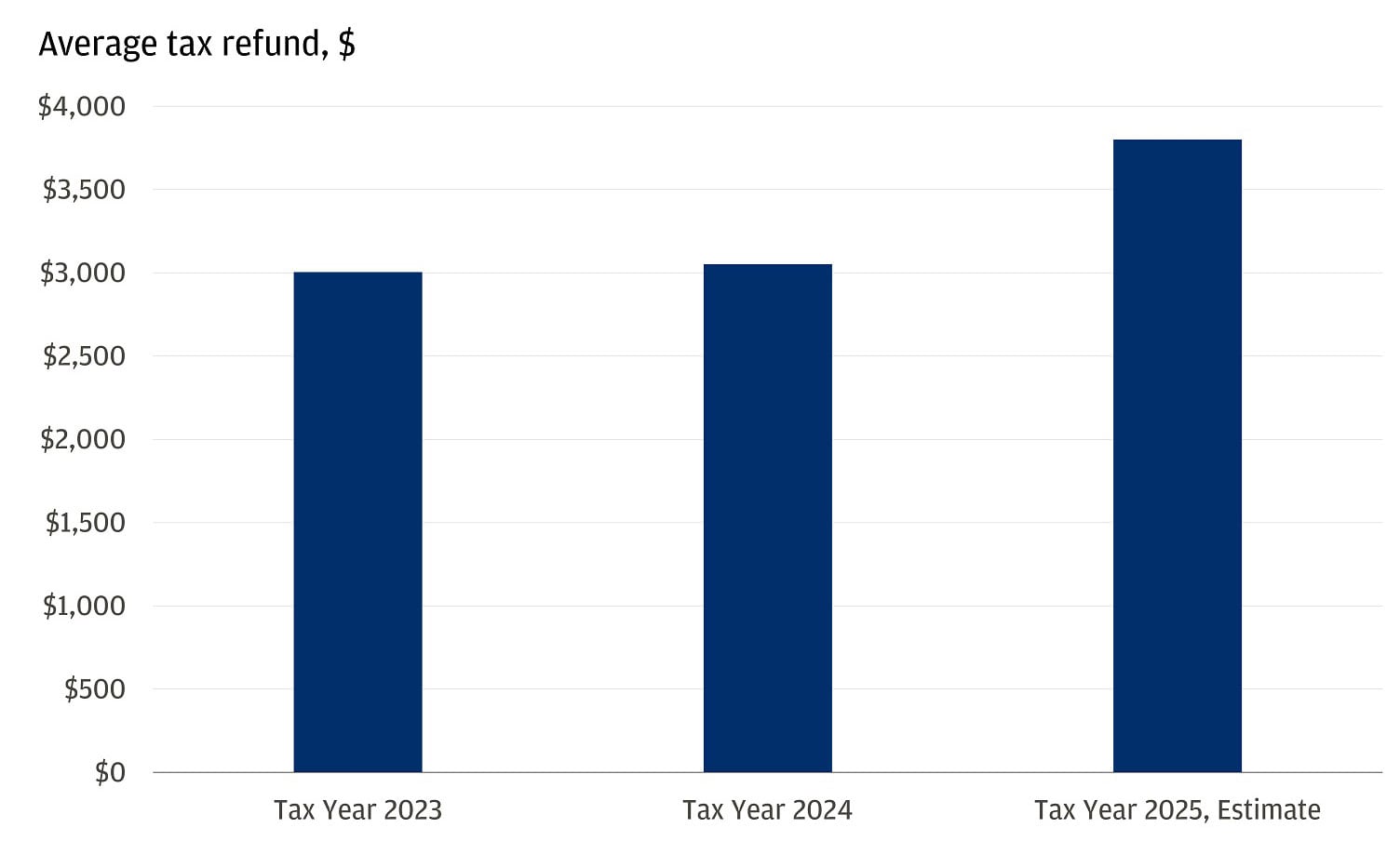

The One Big Beautiful Bill Act (OBBBA) adds a policy tailwind

It is a potent pro-growth surge delivering fiscal support and targeted incentives. Rising tax refunds early in the year should buoy consumer spending and spur business investment. We estimate that consumers will receive an extra $50 billion–$100 billion, about 0.2%–0.4% of annual disposable income.

The OBBBA should result in large tax refunds in 2026

The bottom line

Put it together, and we’re comfortable underwriting 2% growth in 2026, a similar level to the 2% growth expected for 2025.

This setup is very much in line with how we’re framing 2026 in our broader Outlook: Promise and Pressure. We see breakthrough AI innovation, a shifting global landscape and a recalibrated inflation regime create an environment of significant opportunity tempered by enduring structural challenges.

Of course, there are risks. The Venezuela headlines this past weekend were upbeat for the future prospects of the country (check out our latest webinar replay hereOpens overlay), yet they still served as a real-time reminder of how quickly the narrative can shift. There is also the risk that inflation proves sticky or reaccelerates. The Fed could be forced to pause rate cuts – or even revisit rate hikes – catching markets off guard after they had been anticipating a lower inflation and rate environment. Geopolitics and inflation are just one source of uncertainty, but far from the only one. In our 2026 Outlook, we address the big questions we’re hearing most from investors about AI, a fragmented world and inflation.

Building on that discussion, our Chairman of Market and Investment Strategy, Michael Cembalest, in his 2026 Eye on the Market Outlook, covers a range of topics. Notably, he highlights four key risks shaping today’s environment: a metaverse moment for the hyperscalers, U.S. power generation constraints, China expanding its competitive edge in AI and the paradox of U.S. reliance on Taiwan – a crucial semiconductor hub that is de¬eply tied to China.

All that to say, stay constructive but mindful. Our base case keeps us leaning pro-growth, while our risk analysis guides us on where to size carefully, what to diversify with and what we want to own if the path gets bumpier. Here are the areas we have highest conviction on:

- We’re targeting an S&P 500 year-end around 7,300 in our base case – with a bull case closer to 8,100 if the market keeps rewarding durable growth.

- We expect investment grade (IG) bond spreads to hold around 85 basis points (bps). More a steady, reliable carry than a wild home run, but nonetheless a vital ballast in a diversified portfolio. In an era of rangebound inflation and an easing Fed, bonds can finally shine again.

- We’re anticipating that gold will finish above 5,250. Gold is a robust hedge against sticky inflation, geopolitical headwinds and unexpected policy moves. Think even broader when diversifying your diversifiers.

All market and economic data as of 01/09/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.