Tariff turmoil and dollar's fall stress importance of geographical diversification for investors

Head of Investment Strategy, J.P. Morgan Wealth Management

We’ve all heard the adage that April showers bring May flowers. And while we don’t know what kind of flowers this May will bring just yet, it’s fair to say that investors faced a storm of policy uncertainty and heightened volatility in April.

In light of the inclement weather, so to speak, we’re here to explore three key themes that shaped the month for investors: the “Liberation Day” tariff announcements (and what followed thereafter), the unusual path of recent U.S. dollar-denominated asset depreciation and the continued importance of asset-class and geographical diversification in portfolios.

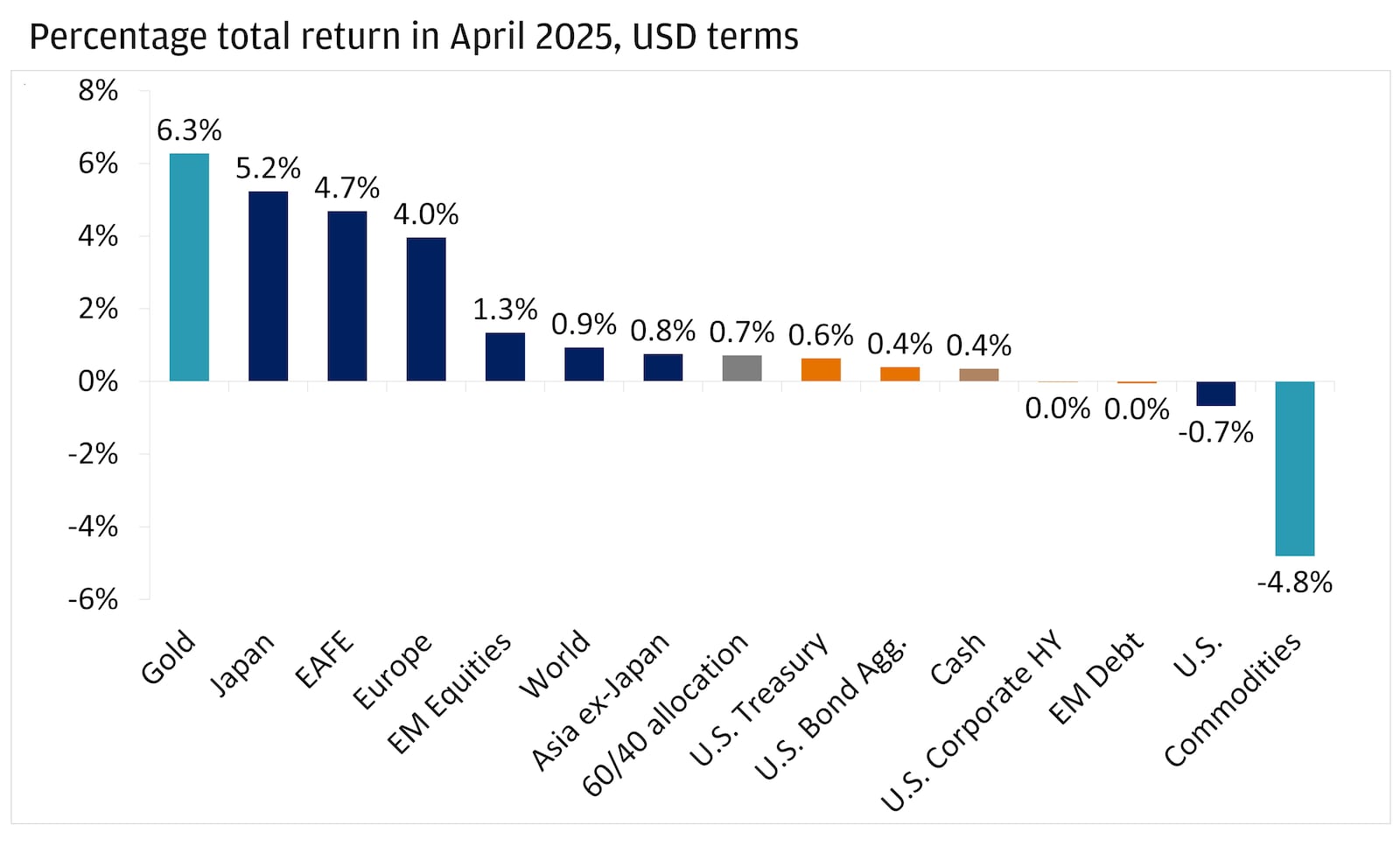

Gold and international equities continue to play a diversifying role

The moment we’ve all been all waiting for?

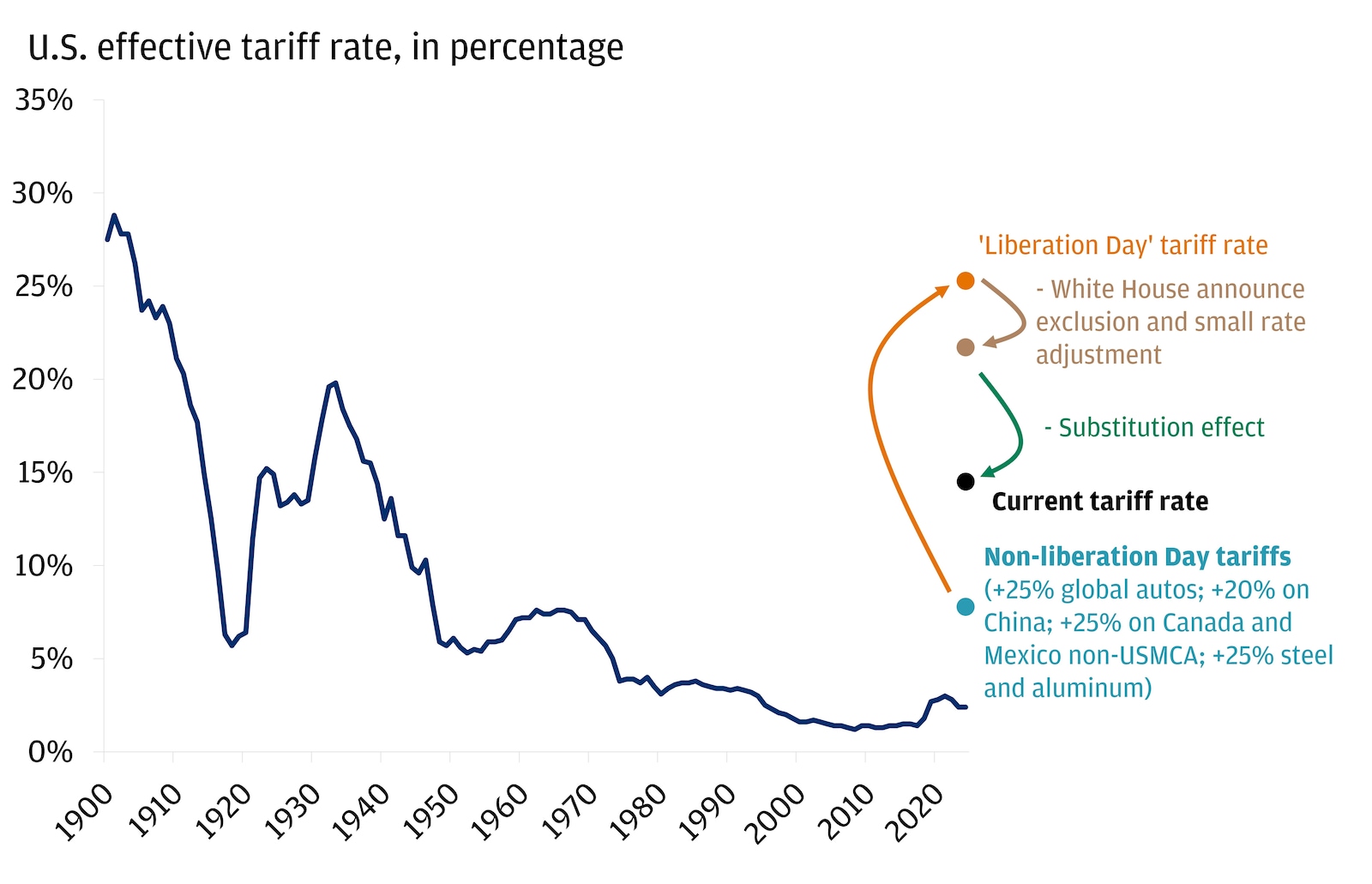

April began with “Liberation Day” on April 2, when President Trump announced new, sweeping tariffs that exceeded most of Wall Street’s estimates. These tariffs included a baseline 10% tariff on all imports, with additional “reciprocal” tariffs on goods from most U.S. trading partners.

The announcement triggered quick risk-off moves in markets, with the S&P 500 falling nearly 5% on the first subsequent trading day. The tumble continued for a week until April 9, when the Trump administration announced a 90-day pause on most reciprocal tariffs, excluding China (which had subsequently retaliated and was slapped with an increased tariff rate of 145% as a result). The freeze on “reciprocal” tariffs catalyzed a single-day gain of nearly 10% for the S&P 500, making it the 10th biggest jump in the history of the index.

Throughout the rest of the month, tariff carve-outs were created for specific sectors, like electronics and semiconductors and headlines about negotiation progress swirled. Heading into May, the situation remains fluid.

At the very least, the Trump administration seems open to compromise, and tariff rates look likely to land at lower levels than the opening bid presented on “Liberation Day” – albeit ones that are still higher than those that have been in place for nearly a century. We’ll be monitoring incoming developments closely along with economic indicators like consumer spending, employment conditions and inflation gauges for signs of slowing growth and rising price pressures. In the longer term, we’re keen to observe how supply chains and long-standing trade alliances may shift.

To dive deeper on our assessment of the risks, check out our recent Top Market Takeaways on the matter.

The current tariff rate still presents challenges the U.S. economy

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Is the dollar seeing its demise?

For a long time, U.S. stocks, bonds and the dollar have enjoyed a privilege among global investors, thanks to strong economic growth and high returns relative to their peers. This year, however, uncertainty around U.S policies (e.g., tariffs, deportations and White House pressure on the Federal Reserve) has been making investors question the durability of U.S. exceptionalism.

The concurrent decline in U.S. stocks, rise in U.S. Treasury yields (i.e., lower bond prices) and depreciation of the U.S. dollar seen in April were unusual. This rare occurrence is raising questions as to whether investors are rethinking their confidence in U.S. markets and the dollar’s status as the world’s dominant reserve currency.

Why does a potentially weaker dollar matter? In the short term, a weaker dollar can make imported goods and commodities more expensive, which might lead to higher inflation and complicate matters for the Fed. On the flip side, it can help U.S. companies that sell products overseas by making their goods cheaper for foreign buyers. And for investors with exposure to international markets, a weakening currency actually adds to dollar-denominated total returns.

Thinking longer term, some are wondering if April’s moves signal the start of the dollar’s demise. We do not believe that is the case. Rather, last month’s depreciation of the currency is more likely a cyclical reset to correct a material overvaluation than it is a fundamental breakdown.

However, there is a risk that the erosion of U.S. institutions and global trust could lead to a more structural reset and weigh on the value of the dollar over the medium term. For now, the U.S. economy remains strong, still a major player in the global financial system and its assets are still valuable core holdings. Regardless, the recent shifts remind us of the importance of not being overly reliant on any single market and, of course, having a well-diversified portfolio.

Investors who are cautious about a declining dollar should consider spreading investments across different regions and currencies. This could mean looking at international markets, like Europe and Japan, to help balance portfolio exposures.

Speaking of diversification…

An investor holding an overweight – or sole exposure – to U.S. stocks likely felt the fallout of April’s volatility more acutely. A relief rally in the second half of the month helped recoup the worst of the losses, with the S&P 500 ultimately finishing down less than 1%. Even so, the journey for U.S.-only stock investors was bumpy.

Investors who navigated the month with diversified positions across regions, however, likely had a smoother ride. For example, European and Japanese equities provided stability amid U.S. equity volatility (+4% and +5.2%, respectively) in April. Including assets like gold or fixed income in portfolios offered additional stability. Gold continued to soar with a 6.3% gain for the month, and U.S. bonds held steady (+0.4%).

While tempting, it’s important not to over-index portfolios to only recent winners. Consider Tiger Woods, one of the greatest golfers of all time, who’s won 82 PGA tour events throughout his career. Exceptional, right? Sure, but when we take into account that he’s played over 1,000 tournaments, 82 victories suddenly seems low. The takeaway here is that Woods winning one tournament didn’t necessarily mean he was guaranteed to win the next – any seasoned athlete can tell you that. Case in point, heavy hitters don’t shine all the time; if anything, the bright spots punctuate frequent, inevitable bouts of trial and error.

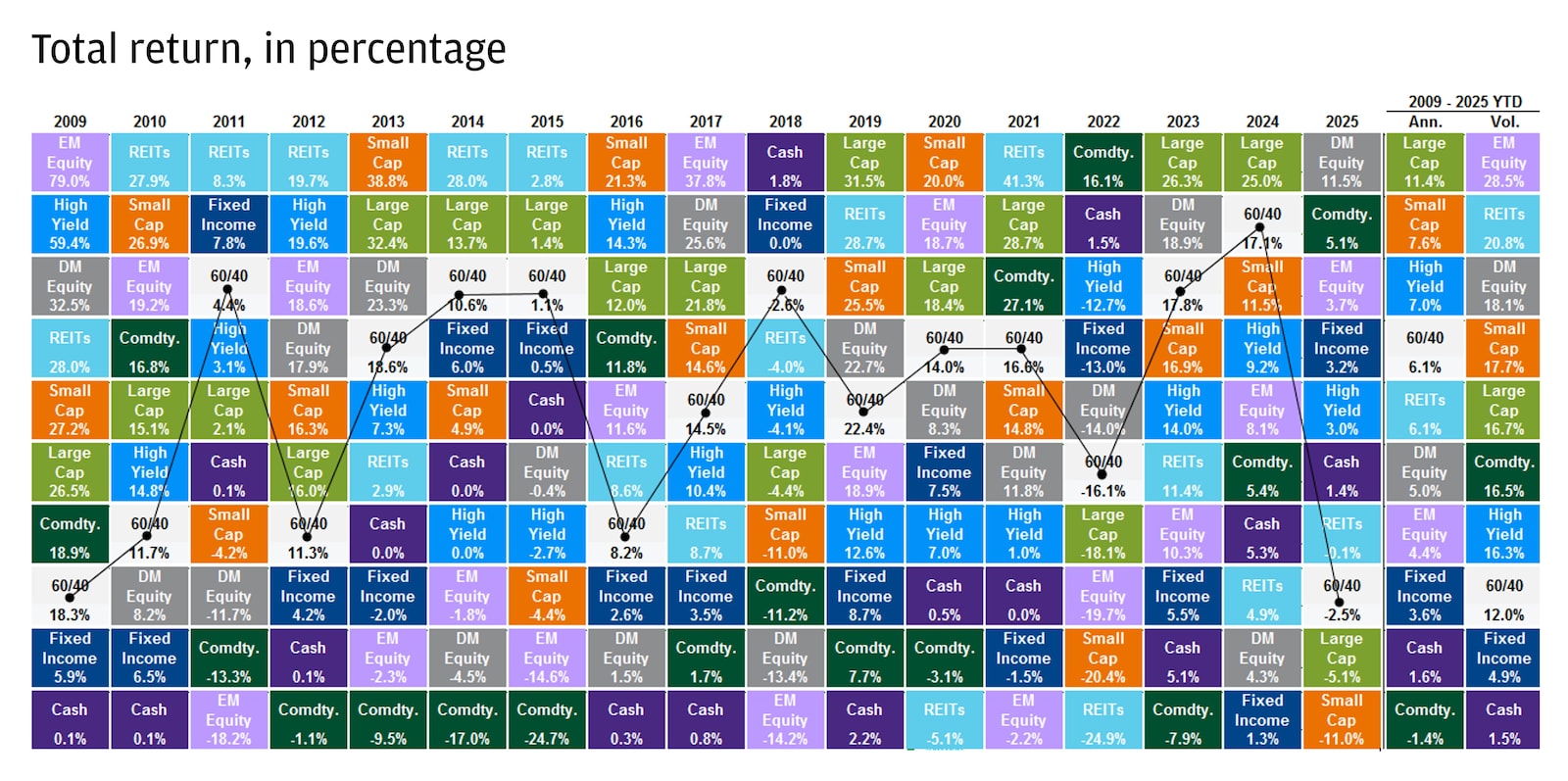

Funnily enough, this concept translates over fairly well to investing, too. Just because one asset has had a strong 2025 thus far doesn’t mean it’ll stay strong through the remainder of the year. Following this, diversification is almost always the key to more consistent returns. By spreading investments across different asset classes and geographies, you can reduce the risk of being overly exposed to any single market or event. In weather terms – and in the spirit of this past April’s showers – a well-diversified portfolio makes for a wider, sturdier umbrella.

Diversification is key to consistent returns

May flowers?

While April presented its share of challenges for investors, those with diversified portfolios were better prepared to navigate them. Looking ahead, we’re keeping an eye on where tariffs land, how the Fed responds to incoming economic data and corporate earnings results.

Remember that maintaining a long-term perspective and diversifying your investments are crucial to staying on track with your financial goals. J.P. Morgan Wealth Management is here to provide guidance and support as you make investment decisions aligned with your investment strategy and risk tolerance.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

Head of Investment Strategy, J.P. Morgan Wealth Management