When oil jumps, household wealth guides the economy

History is no stranger to oil shocks. The oil embargo of 1973. The crisis of 1979. More recently, the price surge after the war in Ukraine in 2022. Each episode rattled the global economy, yet over time markets and policymakers have become better at navigating supply disruptions. Oil production can adjust. Strategic reserves can be tapped. While painful, they can be temporary.

But a hit to demand is a different story. Unlike supply-driven disruptions, demand destruction is far harder to reverse. Once consumers pull back, spending habits shift, and growth slows. That means the next oil shock has the potential to paralyze economies not through gasoline or diesel shortages, but rather through a potential selloff in the stock market. Cue the wealth effect.

Before exploring what this looks like, it’s worth remembering that none of this inevitable. The conflict in Iran is not expected to be drawn out. And this hypothetical doesn’t account for changes in monetary policy, government intervention, fiscal support or production increases from American shale and deep-water rigs around the world— all of which are likely to materialize should oil prices remain high and the economy truly show signs of duress.

A matter of time

The Federal Reserve’s inflation model approximates that a $10 increase in oil prices pushes inflation up by 0.35%. Using that as a roadmap, a conflict ranging three to six months that pushes oil to $100 per barrel would further inflate the economy by 1.4%. And from there, the number rises. The longer the conflict, the higher the price and the more direct readthrough into inflation.

The good news is that it can take time to affect consumer behavior and trickle into the data, which means if the disruption is brief, the impact can be limited. Perhaps the most apt example is the 1990-91 Gulf War when Iraq invaded oil-rich Kuwait. Crude prices doubled, stocks dropped over 20% and recession odds spiked. Within three months, prices normalized. Speed was the advantage.

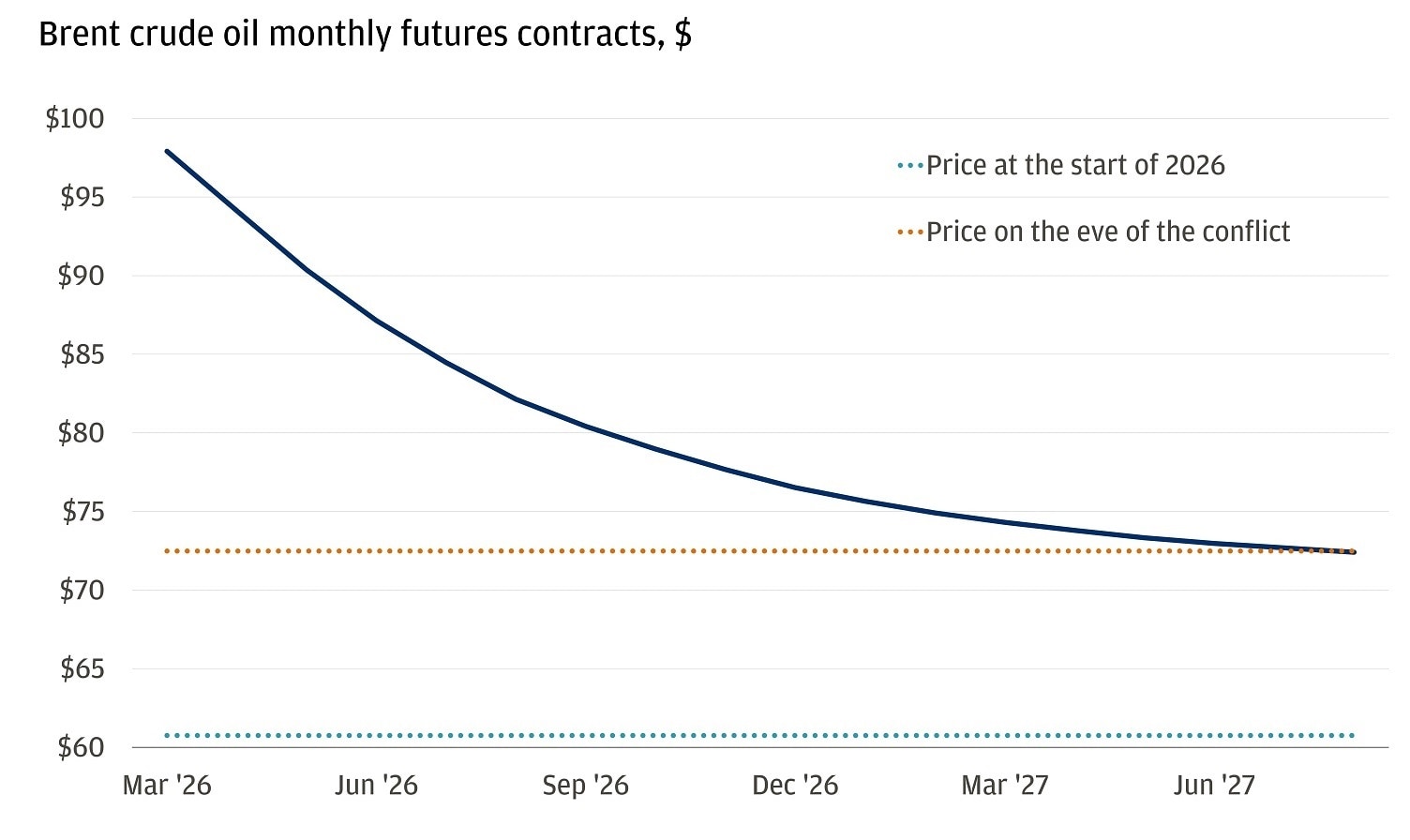

Today, the same scenario could be far more destabilizing, even if it only lasts three months. And markets are expecting Brent crude prices to remain above pre-conflict levels until mid-2027, as even a quick end to the conflict would involve a slow return to full production and heightened risks for the near future.

Markets expect elevated oil prices for some time

The knock-on effects of the oil spike aren’t just inflationary via prices at the pump and dangerous passage in transit routes like the Red Sea or Strait of Hormuz. It also rattles the stock market. That’s the transmission mechanism that makes this not just a supply side issue, but a demand-destructive one. And that could be even more dangerous for the global economy.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

A magnifying glass

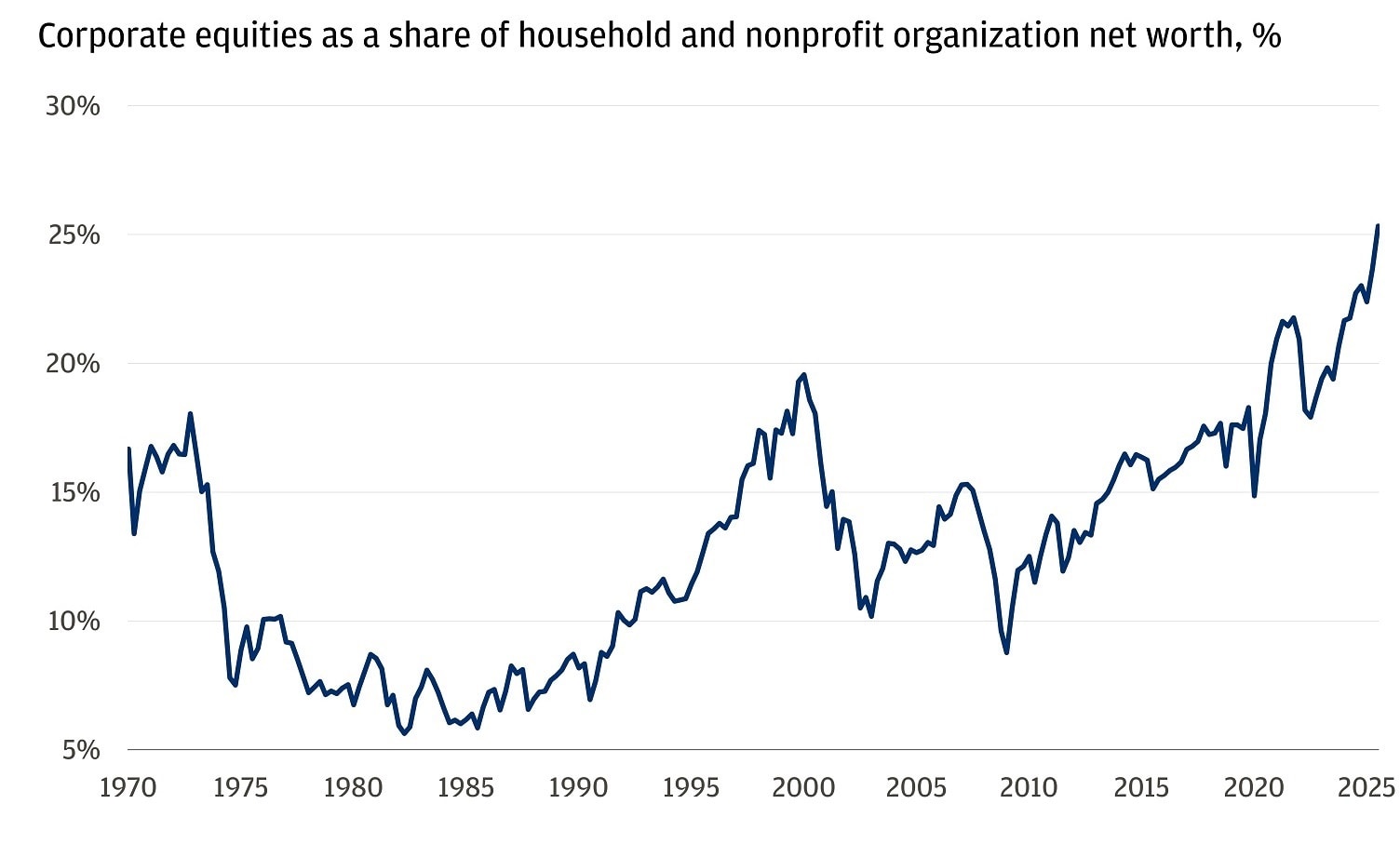

American households have been spending at a rate outpacing income growth for the last 18 months. With balance sheets at all-time highs, 25% of net worth comes from corporate equities.

Emboldened by the stock market rally, consumers have been taking their cue from the price of their assets over the marginal increases in their paychecks. When times are good in the market, it feeds into the economy. It feels like there’s more money in savings, investments and retirement accounts and therefore encourages more spending. It’s the wealth effect at play.

Household wealth in equities is at record levels

But that also leaves the economy asymmetrically vulnerable. A reversal in asset prices can cause a sharper pullback in consumption, magnifying the oil shock’s inflationary impact onto the economy. In other words, the stock market drops, savers feel the crunch – even if it’s only on paper – and suddenly, they’re careful about making their next purchase. Combine that with prices at the pump ticking higher, and it becomes harder for consumers to spend again.

A domino effect

A sustained oil price as high as $90 per barrel would likely catalyze a 10%–15% decline in the S&P 500. As the price rises toward and beyond, say, $120 per barrel, the selling in the S&P 500 will intensify. The implications extend beyond the United States. International and emerging markets typically carry a higher sensitivity to global growth shocks, and the spillover abroad could be even larger. The shift in outperformance is already palpable since the start of the conflict.

From a growth perspective, every 10% decline in the U.S. stock market then has the potential to reduce consumer spending by 1%. Now, combine it all. The compounded effect of sustainably higher oil prices and an S&P 500 bear market has a destructive demand effect, materially amplifying the hit to growth.

But in the face of shipping and oil production snafus, it’s the stock market that may have a more immediate impact on consumer behavior, before prices at the pump. And if the stock market reacts sharply enough, the next oil shock will not just be a supply problem. It could become a demand one. The situation remains volatile and there is no guarantee of the outcome, but overall consumer health and energy independence put the U.S. on relatively more resilient footing compared to its international peers.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank