Beating the heat: Why US equities soared in June

Global Investment Strategist

An early summer heatwave caused many cities across the U.S. to experience record-setting temperatures in June. But the thermometer wasn’t the only record breaker this month. The S&P 500 rose over 5% in June, hitting its first new record high since February 19.

Below, we dive into the key themes that defined June, including ongoing tariff developments, an update on the Federal Reserve (Fed) and conflict in the Middle East.

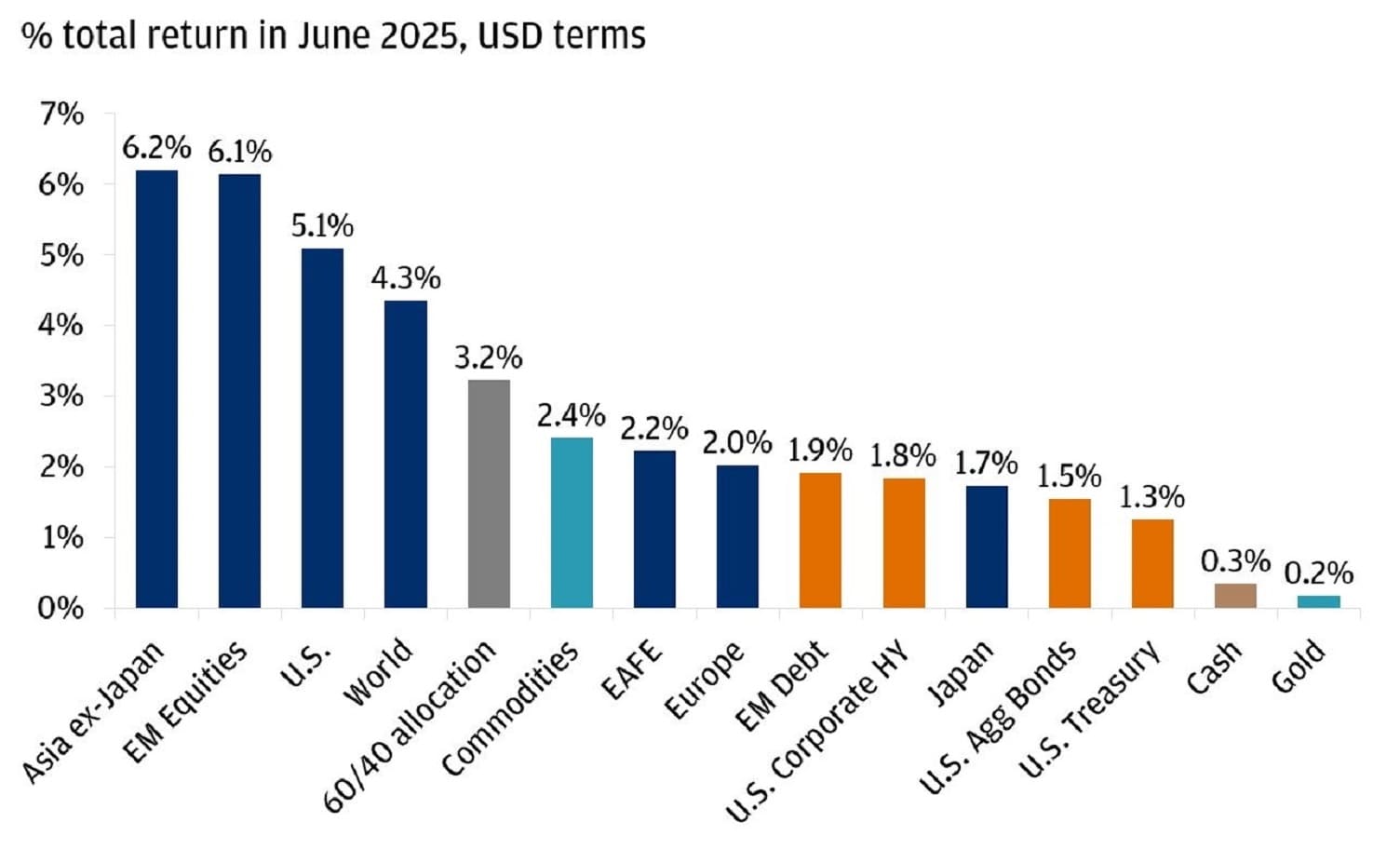

U.S. equities continue to rally in June

Tariff temperature check

June brought more tariff drama. Early in the month, President Donald Trump increased tariffs on steel and aluminum imports from 25% to 50%, affecting all trading partners except the United Kingdom. More broadly, however, trade negotiations seemed to yield some progress. A truce with China was reached that reduced tariffs to 30% for U.S. imports from China and 10% for Chinese imports from the U.S.

With the 90-day reciprocal tariff pause slated to end on July 9, some negotiations are still ongoing. We don’t think it’s likely that tariffs will rise back to the levels threatened in April, but the effective tariff rate remains well above what the U.S. economy has experienced in recent years.

For now, tariffs have yet to feed through to consumer inflation. The May Consumer Price (CPI) Index report was cooler than anticipated, with both the headline and core indices rising 0.1% on the month (compared to expectations of 0.2% and 0.3%, respectively). Core CPI inflation is now down to 2.8% year-over-year, compared to 3.4% at the end of 2024. With tariff collections rising again in June and businesses expected to pass some or all of the cost of tariffs through to consumers, we expect to see a more visible impact from tariffs on prices in the months ahead.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Fed-speak: No rate cut in June, but potentially soon

Despite continued pressure from the White House to lower interest rates, the Federal Open Market Committee decided to keep its policy rate steady for the fourth consecutive meeting, maintaining the federal funds rate within the range of 4.25% to 4.50%. Fed Chair Jerome Powell emphasized the Fed’s wait-and-see approach, flagging ongoing uncertainty in the economic backdrop.

The Federal Reserve also released its Summary of Economic Projections (SEP), which revealed expectations for slower growth, higher unemployment and a modest increase to inflation, compared to their March projections. We believe that even if inflation moves higher, the Fed is prioritizing focus on the health of the labor market. Said another way, their bias seems to be tilted towards rate cuts in the second half of the year.

The unemployment rate and broader labor market conditions appear stable for now, but cracks may be forming. While initial filings for unemployment insurance remain low, filings from existing unemployed persons are on the rise. What that indicates is that those who lost their jobs earlier this year may be facing increasing difficulty in finding new jobs.

Escalation of conflict in the Middle East

In June, geopolitical tensions between the U.S. and Iran reached a critical point following U.S. airstrikes on Iran's nuclear facilities at Fordow, Natanz and Isfahan. These actions initially led to a surge in oil prices due to concerns over supply disruptions, with Brent crude prices jumping by over 13% to highs of $78.50 per barrel.

Gold, typically a hedge during geopolitical crises, initially rose as investors sought safe-haven assets but ultimately ended the month almost flat (+0.2%) as Iran opted for a telegraphed and de-escalatory response. The door for future negotiations seems to be open. The cease-fire helped calm investor nerves and contributed to a decline in oil prices by the end of the month.

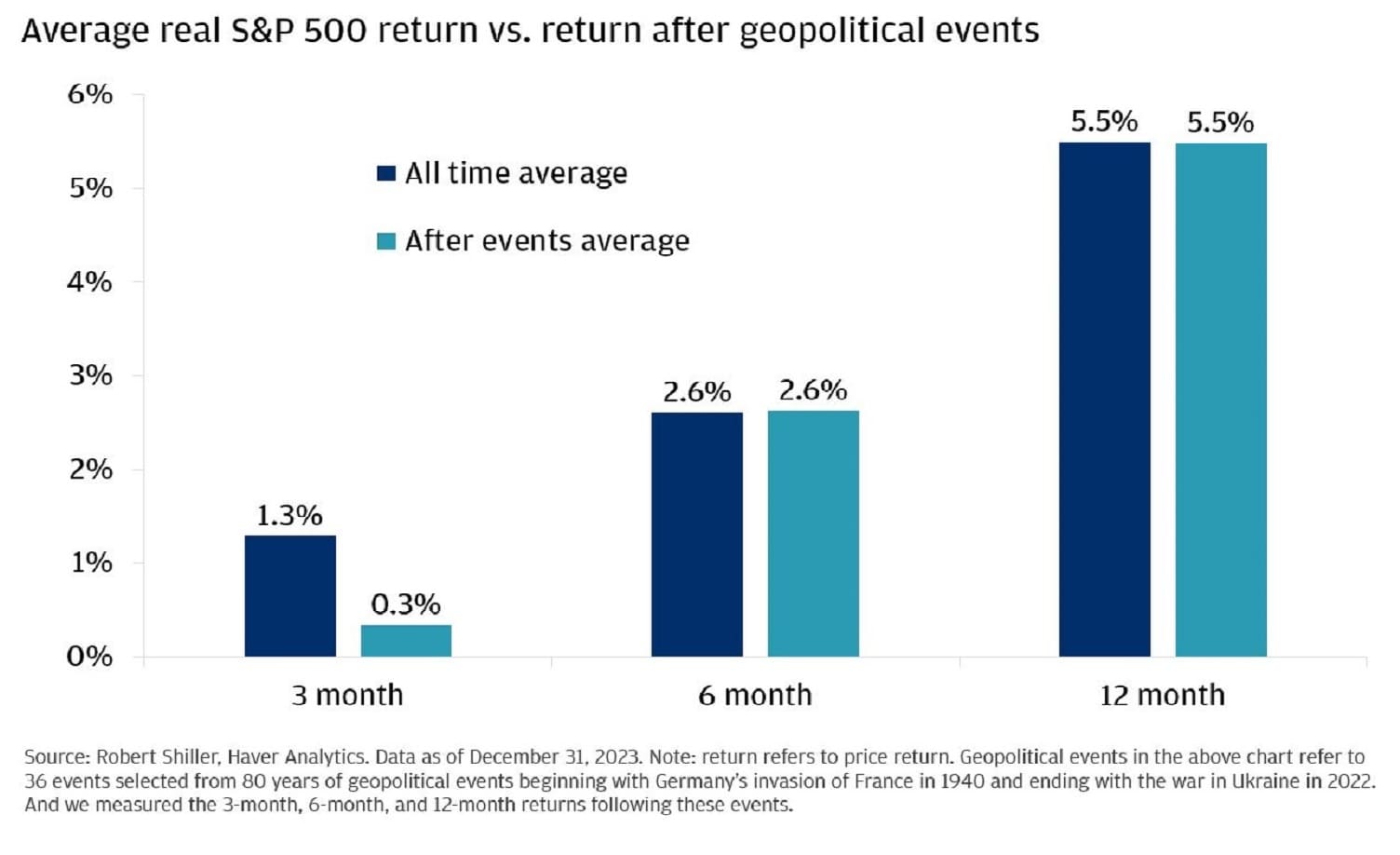

That said, the risk of re-escalation isn’t zero, which could cause near-term volatility. However, it is important to remember that the impacts of geopolitical events on markets tend to be short-lived.

Geopolitics typically have a brief impact on stocks

Investing amid uncertainty

While politics and policy continue to dominate the headlines, market reactions to these kind of events seem to be more muted. Despite the ongoing uncertainty and geopolitical tensions, the S&P 500 reached all-time highs in late June. As we swim into July, one of our key investment themes continues to be increasing portfolio resiliency amid policy uncertainty and geopolitical conflicts.

Ultimately, we think that starts with a portfolio comprised of geographically diversified equities and fixed income that can provide exposure to rising corporate profits during the good times, but also protect against the potential of a growth slowdown. Another potential tool to enhance long-term portfolio resilience may be gold, as it is often considered a safe-haven asset during periods of geopolitical tensions. By focusing on diversification and resilience, portfolios can potentially be better positioned to navigate ongoing uncertainties.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

Global Investment Strategist