3 themes that defined portfolios in 2025 and could continue to shape them in 2026

Global Investment Strategist

The end of the year is often a time for reflection. As this is our last edition of Quick Shot in 2025, here are three themes we believe defined portfolios this year and could continue to influence the year ahead.

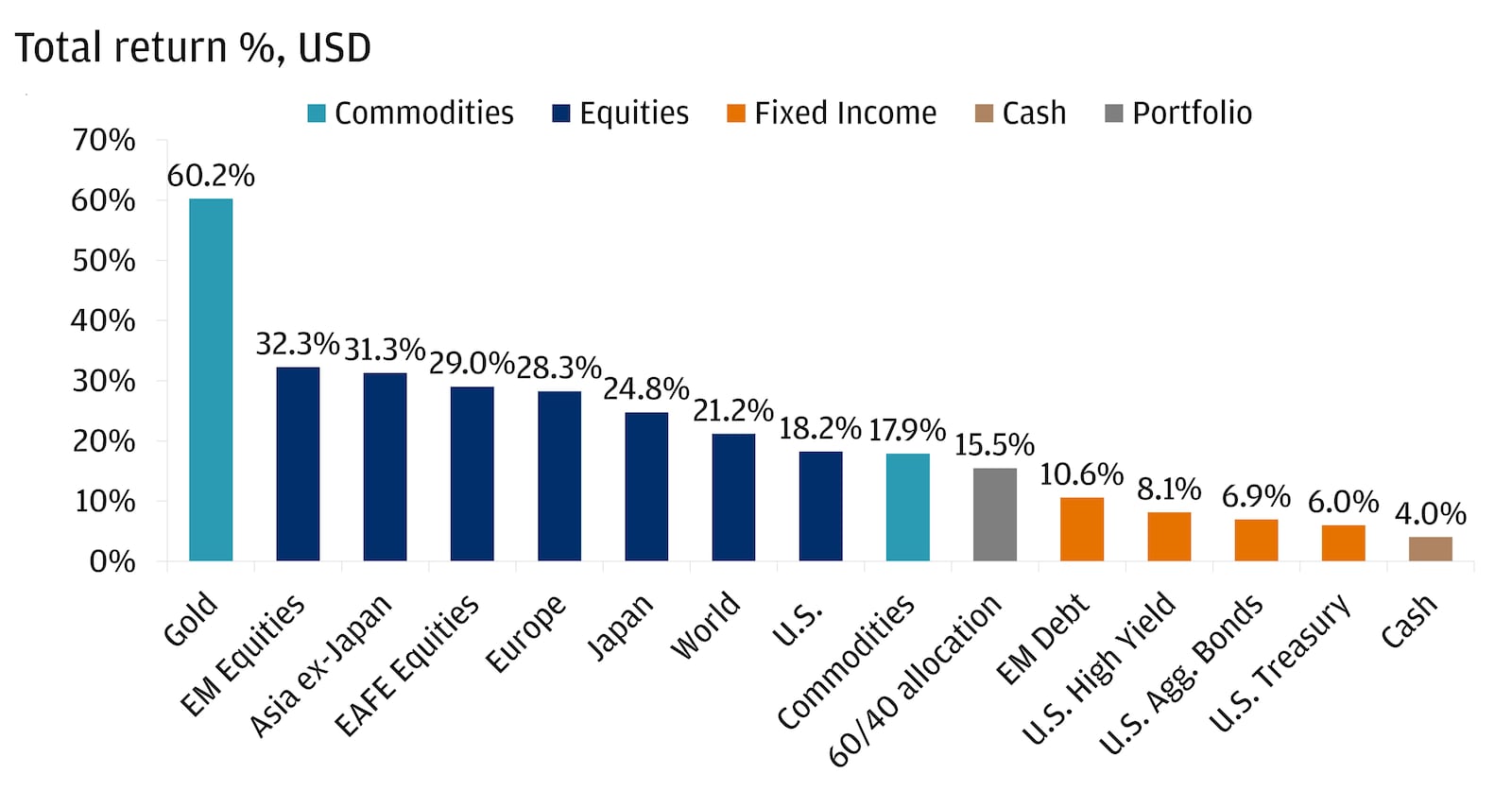

Cash was one of the worst-performing asset classes this year

While elevated yields made cash appear attractive to some investors over the past few years, it was one of the worst-performing asset classes in 2025. Cash has returned just 4% year-to-date compared to roughly 21% for global equities and around 7% for U.S. bonds.

Markets are pricing a nearly 90% probability the Federal Reserve (Fed) will deliver a 25-basis-point cut at the Federal Open Market Committee (FOMC) meeting today, and we expect the Fed to deliver an additional cut thereafter before the middle of next year. As a result, cash yields could continue to decline. In addition, our 2026 Outlook: Promise and Pressure explores why we believe we are entering a new era of inflation, which could be more volatile and elevated than investors have grown accustomed to in recent years.

Cash has been one of the worst performers in 2025

Ensuring you have enough cash on hand to cover expenses and potential emergencies can be an important part of an investment strategy. However, with the potential for lower cash yields and higher inflation moving forward, over-allocating to cash could potentially impact your ability to meet your goals, as higher inflation could eat away at purchasing power. Investors should consider reviewing financial strategies to ensure they are up to date.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

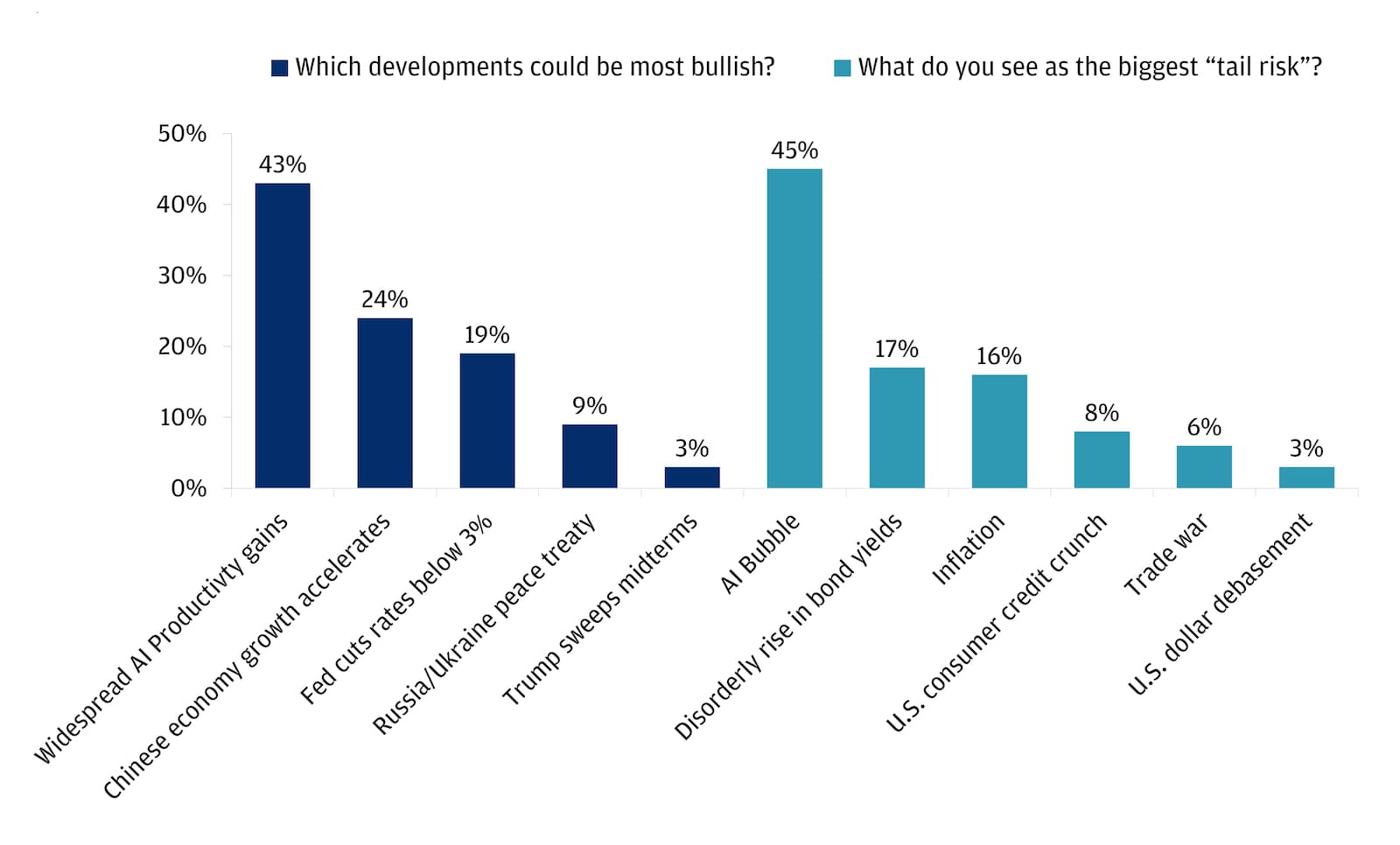

Artificial intelligence brings both promise and pressure to markets

As we head into the new year, the conundrum surrounding the artificial intelligence (AI) transformation is poised to continue, with some investors believing it will bring promise and others seeing pressure. This dynamic is creating a double-edged sword; a recent survey of fund managers showed that AI is driving both bullish and bearish narratives in markets for 2026. On the bull side, investors are optimistic about the potential productivity gains AI could bring. On the bear side, there are bubble concerns that the rapid pace of investment and soaring valuations in AI-related sectors may be unsustainable. This could potentially lead to market corrections if expectations are not met or if the technology fails to deliver on its promise.

AI is at the center of bull and bear cases for markets in 2026

As outlined in our 2026 Outlook, we believe one of the biggest risks for investors is not participating in the AI trade, as this could mean missing out on what may be one of the most important drivers of market returns and transformational opportunities in the coming years.

Still, investors should be mindful of concentration risk. With 30 AI-related names (including NVIDIA, Google parent Alphabet and Facebook parent Meta) representing over a 40% weighting in the S&P 500, investors who participate in the index already have exposure to many parts of the AI trade – without even leaning in intentionally via tech or growth-oriented strategies. Consider balancing positions with our other high-conviction ideas, including the health care sector, which we discussed in a recent edition of Top Markets Takeaways as a sector we’ve turned positive on.

Diversification helped smoothed the ride in 2025

At times, 2025 tested even the most disciplined investors’ resolve, as markets grappled with elevated tariff rates, recession chatter, a weakening labor market, policy uncertainty, geopolitical tensions and more. In our 2025 Mid-Year Outlook, we emphasized the importance of ensuring portfolios are resilient to ongoing risks, in part by incorporating bonds and international equities.

While some investors have questioned bonds’ ability to provide a buffer to portfolios following 2022, when stocks and bonds both declined simultaneously, in 2025, investors have again seen the traditional negative correlation between stocks and bonds play out. Throughout all the trials and tribulations this year, bonds acted as a partial shock absorber to portfolios as equities experienced volatility. So far this year, a 60% MSCI World / 40% Global Aggregate Bond portfolio has delivered nearly the same return as the S&P 500, but with half the volatility. This underscores the potential value of having a balanced asset allocation and the benefits of staying invested.

Even with a sharp recovery in U.S. equities since April’s lows (over 35%), developed international markets have outperformed meaningfully this year. We don’t think the international investment thesis has already played out and believe investors should consider adding non-U.S. equities to portfolios, largely due to important moves made in Europe over the past year regarding expansionary fiscal policy. Germany introduced its largest fiscal policy package since the period following the country’s reunification in 1991. The spending is expected to contribute about 1% to euro area gross domestic product (GDP) next year, potentially supporting corporate profits and valuations. The country is committed to investing hundreds of billions of euros in defense in the decade ahead, with additional funding set aside for infrastructure investments. Additional spending on defense and infrastructure could unlock faster productivity growth, which Europe has lacked for decades.

Going forward, we have a constructive view on both U.S. and international equities, but investors who are underweight international markets relative to MSCI World weightings could consider moving to a “neutral” weighting between markets versus global indexes (approximately 70% U.S. and 30% non-U.S.).

The bottom line

All in all, we believe the coming year presents a market environment that will be shaped by promise and pressure. Your J.P. Morgan advisor is here to help you evaluate how to right-size cash holdings, lean into potentially transformational megatrends and enhance the resilience of portfolios against potential risks to the outlook. See you in 2026!

All market and economic data as of 12/08/2025 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist