What moved US markets in November?

Global Investment Strategist

What moved US markets in November?

November brought cooler temperatures to the Northeast, and a noticeable chill to equity markets. Still, U.S. equities managed to squeak out a seventh straight month of positive returns (S&P 500 +0.2%), even as the artificial intelligence (AI) story continued to evolve with a mix of optimism and skepticism. Meanwhile, investors grappled with shifting Federal Reserve policy path expectations. Even though these events sparked bouts of volatility, assets like bonds and gold helped provided stability to portfolios.

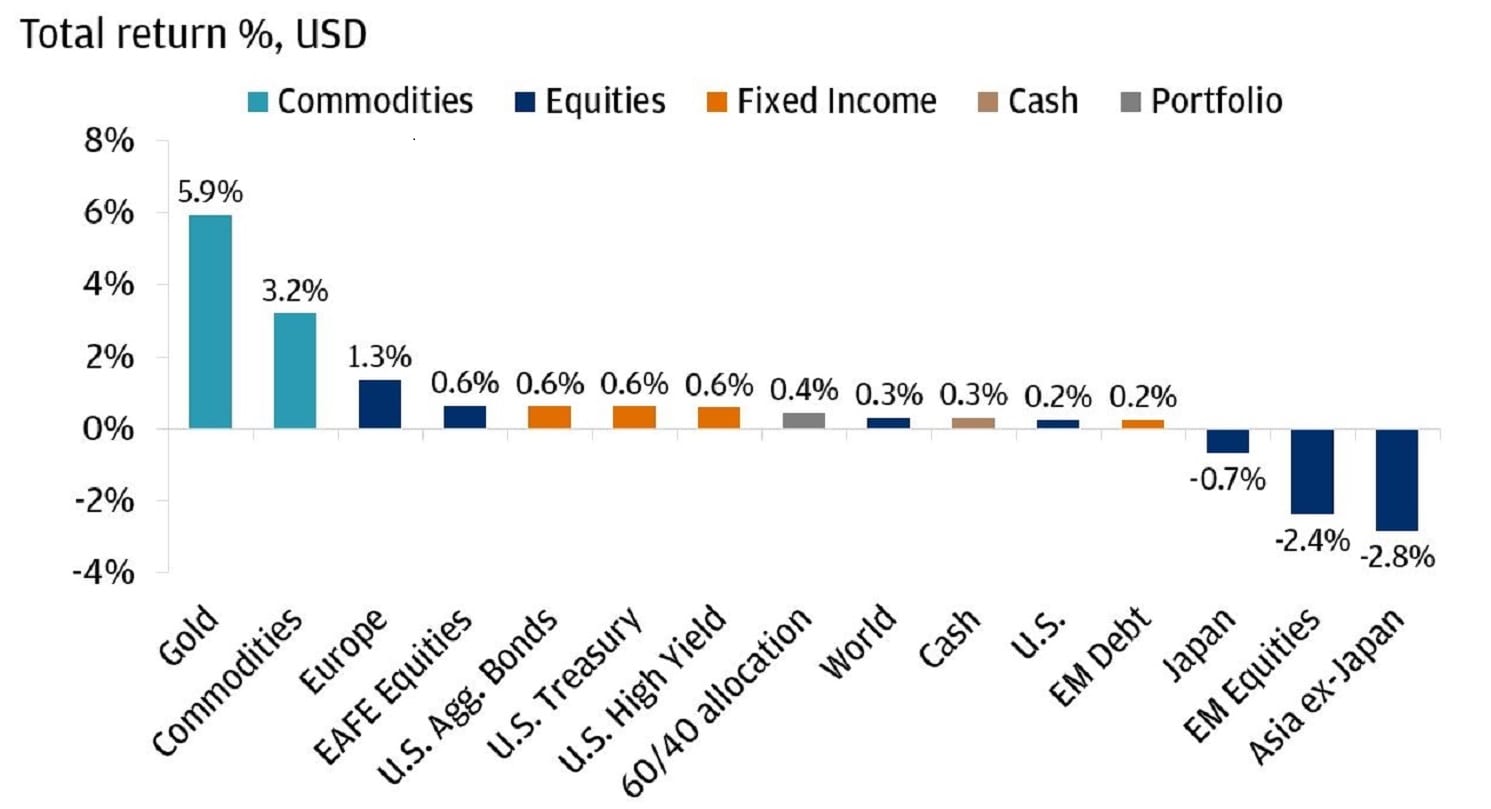

Despite volatility, U.S. equities delivered a positive return in November

Below, we recap how these themes shaped market performance over the past month and what they could mean for portfolios as we head into the final days of 2025.

AI euphoria meets skepticism

November marked a turning point for the S&P 500’s technology sector, which posted its first negative monthly performance since March (-4.4%). Hyperscalers, in particular, faced continued scrutiny as concerns about rising AI capital expenditures and fears of a potential bubble stayed in the spotlight. These worries weighed heavily on hyperscalers, the broader tech sector and the overall AI ecosystem, prompting investors to question whether the AI-led rally could be sustained.

One of the most closely watched events was Nvidia’s Q3 earnings report, which served as a litmus test for elevated valuations across the AI trade. The chipmaker once again beat expectations and underscored the sector’s momentum, with both earnings and sales up over 60% year-over-year. In addition, Nvidia’s guidance for Q4 ($65 billion in revenue) helps reinforce the notion that AI-driven growth is more than just hype.

Despite delivering impressive earnings and robust guidance, Nvidia’s shares declined more than 8% in November. This reaction highlights how investors remain highly attuned to any signals that could challenge the AI growth narrative and the justification for elevated valuations across the sector. Notably, Nvidia’s forward price-to-earnings (P/E) ratio, now around 27 times, sits below its five-year average and remains well below dot-com-era extremes. This suggests that, while scrutiny persists, the market continues to differentiate genuine growth from speculative excess within the AI ecosystem.

While the broader tech sector was among the worst performers for the month, communication services (+6%), led by Google (+11%), stood out as one of the best-performing sectors of the quarter, helping to keep the S&P 500 positive for the month. Google’s launch of Gemini 3 reportedly surpassed OpenAI’s GPT-5 model in intelligence. This breakthrough underscored that legacy tech giants remain competitive and at the forefront of AI innovation.

Overall, November demonstrated that AI continues to be a powerful market driver, but the narrative is becoming increasingly complex. Investors are balancing optimism about future AI spending with concerns about emerging risks and shifts in sector leadership. The divergence in performance among AI-related companies highlights growing selectivity among investors and reinforces the importance of avoiding overconcentration in any single name.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

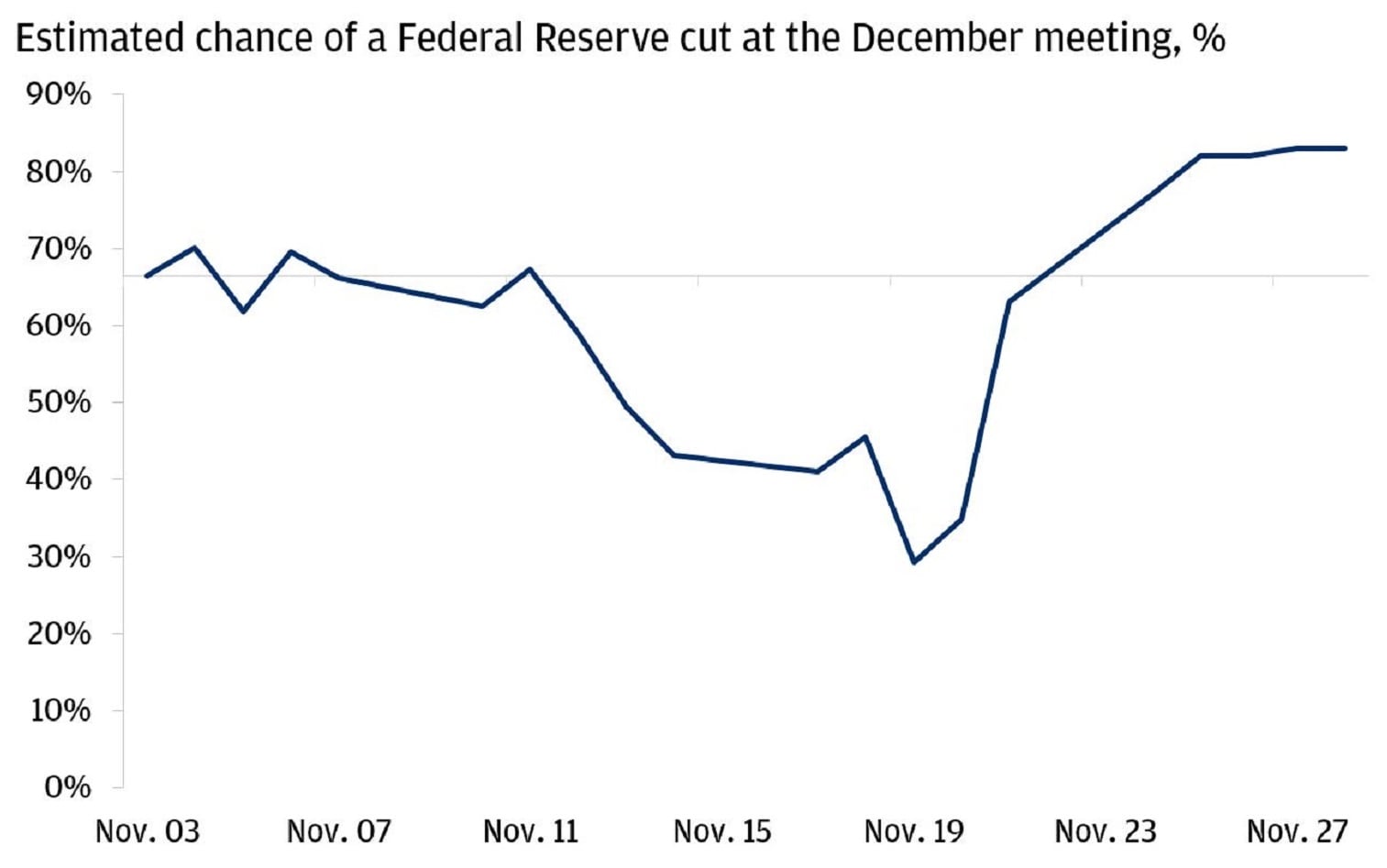

Shifting expectations for a December cut

Markets also faced headwinds in November as expectations for a Federal Reserve rate cut shifted throughout the month. The record-long U.S. government shutdown caused for the delay of several key economic indicators, including inflation and jobs reports that the Fed typically relies on to help guide its policy decisions.

The September jobs report finally arrived late in November, showing a mixed bag as there was a positive surprise in jobs growth (119k jobs added versus estimates of 51k) and an unexpected uptick in the unemployment rate to 4.4% (from 4.3%). Notably, the labor force participation rate rose 0.1% to 62.4%, which helped drive the unemployment figure higher. Importantly, the report showed consistency with the alternative sources of labor market data the Fed relied on during the government shutdown to help guide its policy decisions.

While these dynamics initially helped buoy investor hopes for a rate cut in December, confidence shifted as more information trickled in. Odds dropped below 30% after the announcement that the official October jobs report would be canceled, with some data to be released alongside the November report. However, expectations were later bolstered by dovish Fed commentary, and market-implied odds for a December cut were hovering just over 80% at the end of November. Against this backdrop, we maintain our view that the labor market is bending, not breaking. This should allow the Fed to gradually proceed with rate cuts over the coming months, a development that could be positive for risk assets.

Volatile expectations for a Fed cut in December

Equity volatility: The result of shifting narratives and uncertainty

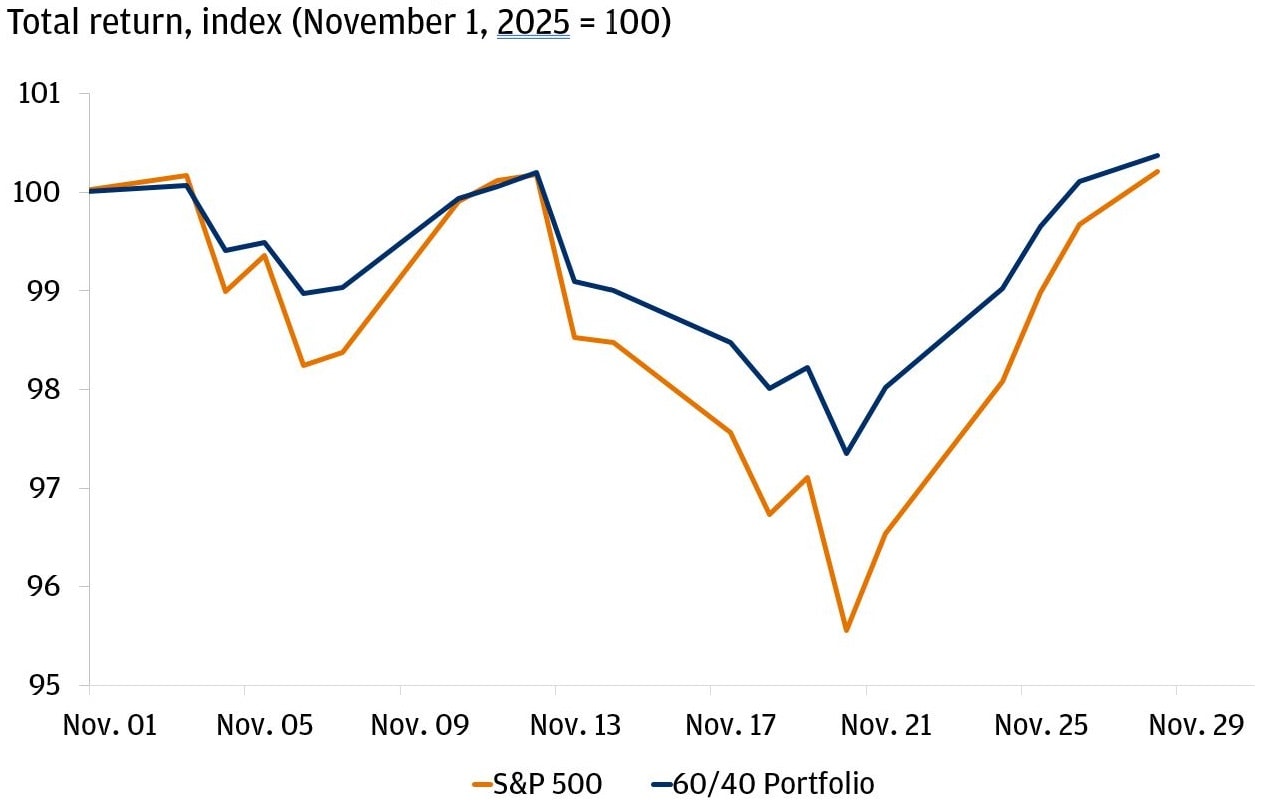

Skepticism around the AI trade and Fed policy uncertainty sparked volatility in November. The CBOE Volatility (VIX) Index, a measure of market volatility, spiked to its highest level since April, reflecting heightened investor anxiety. In previous months, we’ve highlighted the importance of building resilient portfolios that can potentially be better positioned to withstand shocks. November provided a demonstration of that principle in action.

The largest companies in the S&P 500 now account for over 40% of the index and are largely tied to the AI investment trend. As a result, when these companies come under pressure, the rest of the index is likely to follow – a dynamic investors experienced in November. The classic 60/40 portfolio, with 60% allocated to the S&P 500 and 40% to the U.S. Bloomberg Aggregate Bond Index, not only outperformed the S&P 500 outright for the month, but also helped smooth the ride as U.S. equities experienced volatility.

Diversification helped mitigate volatility in November

Gold (+5.9%) again rallied in November as Russia continued its military advances against Ukraine and both sides exchanged drone strikes. A revised U.S.–Ukraine peace framework is circulating, but progress stalled as Russia reiterated that any deal would require Ukraine to surrender territory, a demand Kyiv firmly rejects. These ongoing risks highlight why diversification – including exposure to assets like gold – can help build more resilient portfolios.

All in all, evolving AI narratives, shifting expectations for Federal Reserve policy and equity volatility tested portfolios in November, highlighting the importance of maintaining resilient portfolios. As we inch closer to 2026, our outlook is shaped by both promise and pressure: the promise of innovation, resilience and new opportunities, and the pressure of a fragmenting world order under more volatile inflation.

All market and economic data as of 12/02/2025 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist