3 reasons we now favor the health care sector

US markets posted modest gains

Markets have navigated a mixed but resilient week, with major indices posting modest gains. The S&P 500 was slightly higher on the week, leading the index almost back to all-time highs. Macro data painted a nuanced picture: ADP private payrolls unexpectedly declined, reinforcing the dovish narrative ahead of next week’s Federal Open Market Committee (FOMC) meeting, where a rate cut is now widely anticipated. Early holiday shopping data is solid, but retailers report stress among lower-income consumers.

Artificial Intelligence (AI) remains a focal point as headlines this week highlight both innovation and fragmentation:

- OpenAI is set to launch a new reasoning model, aiming to reclaim technical leadership from Google’s Gemini 3.0 model, which was released last month and has been widely recognized for its advanced capabilities.

- Meta announced plans to cut as much as 30% of the budget for its metaverse group. This move signals to investors that Meta is refocusing resources on areas with better growth prospects.

- Microsoft shares fell after reports surfaced of lower AI sales quotas and targets for certain product lines, reflecting customer resistance to rapid adoption. However, Microsoft clarified that while quotas for some specific AI offerings have been reduced, overall company-wide AI sales quotas have not been cut.

Overall, markets are balancing optimism around monetary easing and earnings with caution over policy shifts and continuing unease over AI bubble concerns. Against this backdrop, one sector stands out for its recent turnaround: health care.

Health care as a preferred sector for investors

Recently, we upgraded health care to one of our preferred sectors – a notable change given its marked underperformance over the past three years. This is a trend shaped by several headwinds:

- COVID-19 digestion weighing on earnings growth: Life sciences and vaccine manufacturers expanded capacity during the pandemic, only to face excess supply and earnings pressure as demand normalized. On the other hand, managed care organizations initially benefited from lower costs driven by reduced doctor visits during and immediately after the pandemic, but are now seeing rising expenses as patients return with more complex needs.

- Policy overhang compressing valuations: Policy uncertainty, especially around drug pricing initiatives like the “most-favored nation” drug pricing proposal, has weighed on investor sentiment and sector valuations. For further information on the numerous overhangs, take a look at what Asset & Wealth Management Chair of Investment Strategy, Michael Cembalest, had to say in his piece Sick as a Dog (PDF).

So, what changed to get us more positive? Here are the three main reasons.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

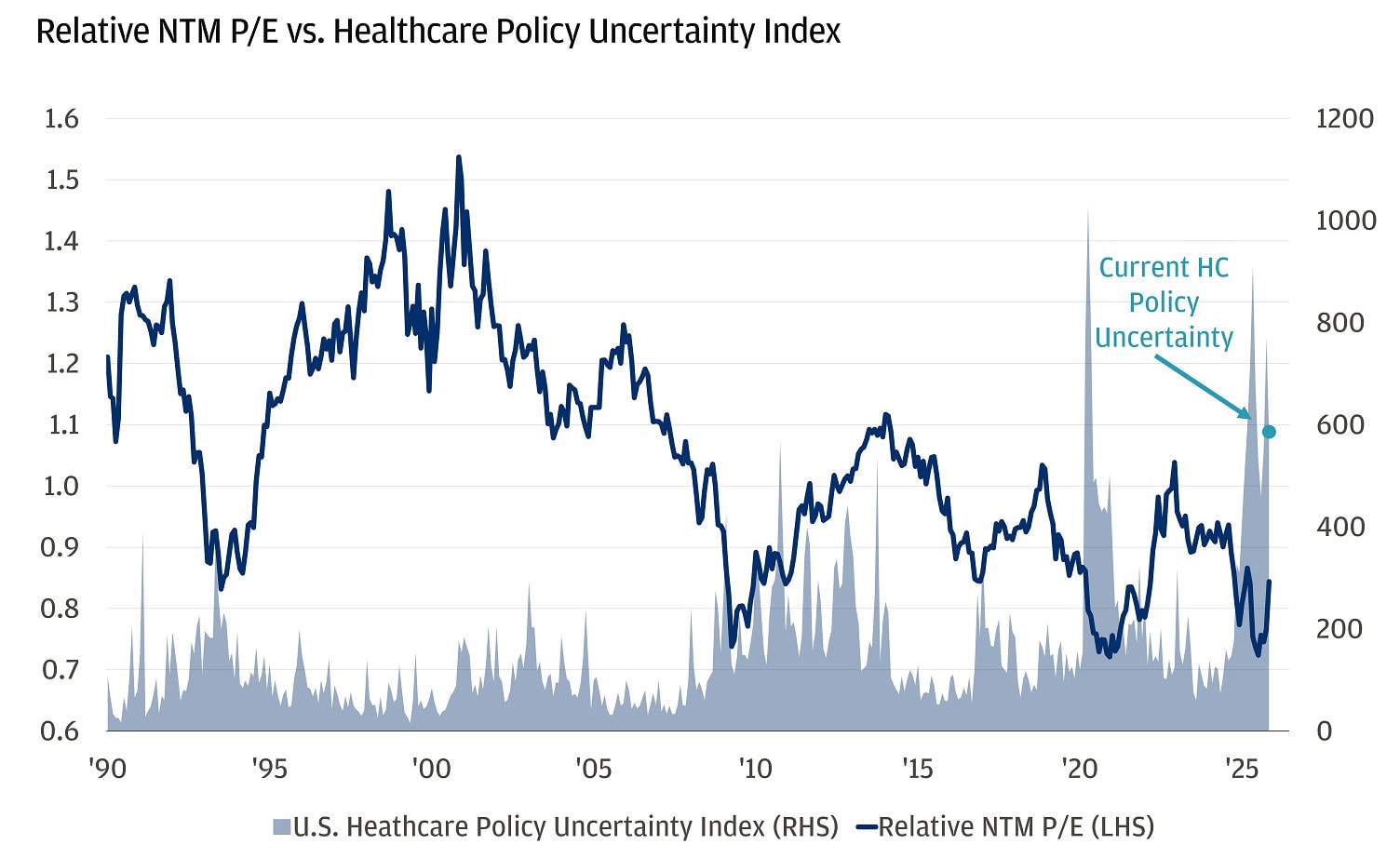

Policy overhang easing

Since last November’s election, policy uncertainty has emerged as a significant headwind for health care valuations. The Trump administration introduced a series of proposals aimed at curbing profitability for various industries, which weighed on investor sentiment and contributed to valuation compression across the sector.

One of the most impactful proposals was the “most-favored nation” drug pricing initiative, which aimed to align U.S. drug prices with those in other developed countries that are oftentimes two to three times less than in the U.S. for a variety of reasons. If implemented, it would have materially affected revenue and margins for pharmaceutical companies and had downstream effects for various other industries as well, such as life sciences companies.

However, in late September, Pfizer became the first major pharmaceutical company to reach an agreement with the administration on drug pricing, removing a significant policy overhang. The deal granted Medicaid access to most-favored-nation-style pricing and expanded discounted direct-to-patient purchasing, helping to resolve this concern and set a precedent for others. Several additional agreements have followed, helping health care become the best-performing sector quarter-to-date (+7% versus S&P 500 +1%). With policy headwinds easing, there is now room for sector valuations to recover from compressed levels.

Policy uncertainty has weighed on valuations

Earnings clarity and stabilization

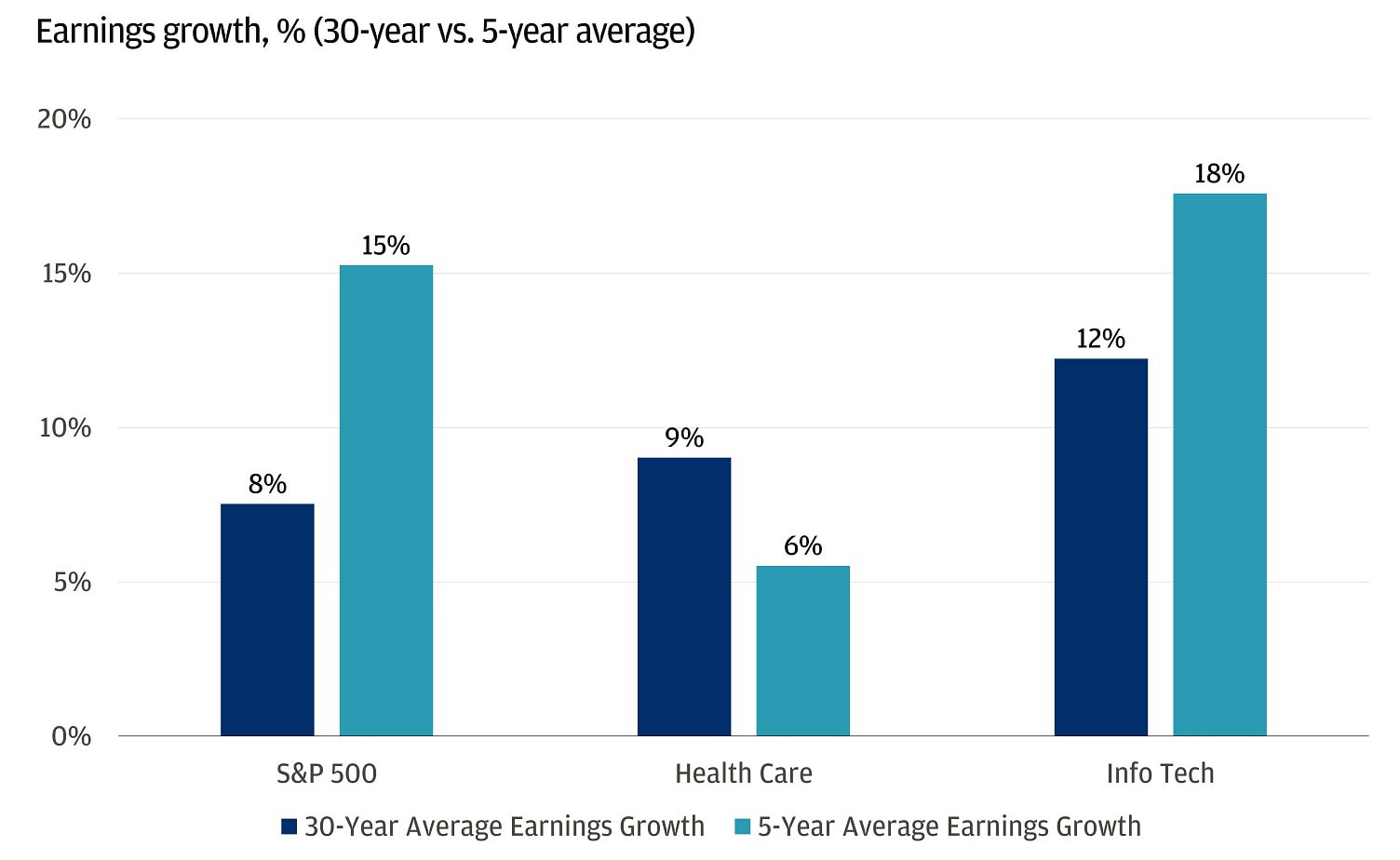

Third-quarter results have provided incremental clarity around where some of the more pressured industries were heading in terms of earnings growth. Life sciences and managed care are showing signs of bottoming as their end markets stabilize and reprice their insurance books, respectively, which allowed them to maintain 2026 guidance. The sector’s relative earnings revisions breadth – which measures the balance between upward and downward analyst estimate changes – has stabilized, and health care companies have beaten Q3 estimates by 13%, well above the broad market’s 7% and the highest beat rate in at least two years. This supports a more constructive setup for earnings growth in 2026.

Historically, health care has outpaced the broader market in earnings growth over the past 30 years. However, in the last five years, the sector has shifted to underperforming the market in terms of earnings growth. The recent stabilization in earnings and guidance from industry leaders suggests the worst may be behind us.

Health Care earnings growth has stagnated following Covid

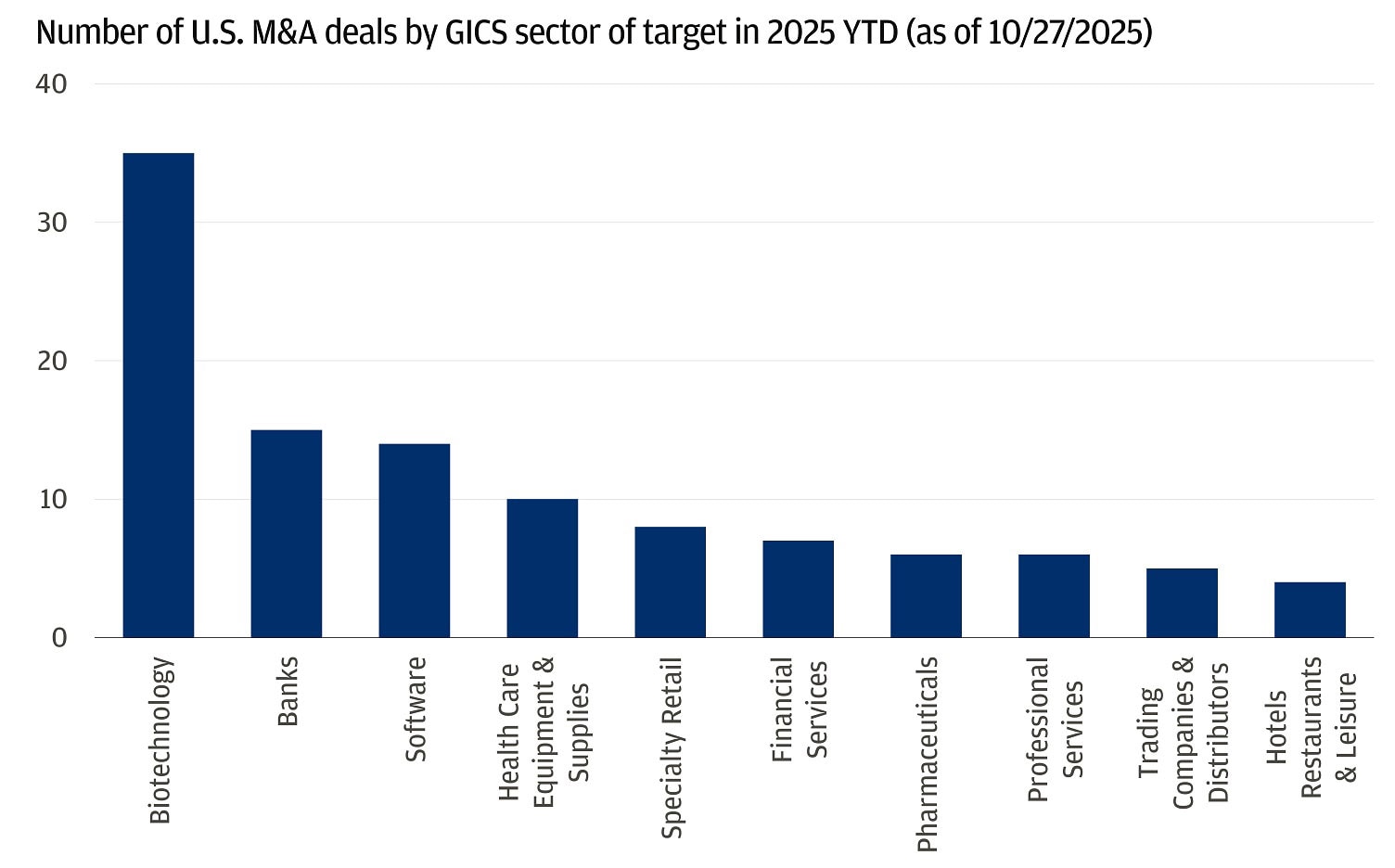

Accelerating M&A activity

Mergers and acquisitions (M&A) have historically been a primary way for health care companies to sustain and grow their revenue pipelines, especially as existing drugs approach patent expiration. When blockbuster drugs lose patent protection, companies face significant revenue declines. To address this, firms typically pursue one of two strategies: develop new drugs internally and secure new patents, or acquire companies that already have promising drugs in development or on the market. Given the high costs, long timelines and risks associated with internal drug development, M&A has become a popular and effective method for quickly replenishing product pipelines and maintaining growth.

After a slow start to the year due to policy uncertainty, M&A activity has picked up meaningfully since Labor Day. Biotech, in particular, has averaged one deal per week, making it the busiest sector for deal activity. If this pace continues, overall health care M&A is on track for its strongest year since 2021.

Biotech has been the busiest sector for deal activity YTD

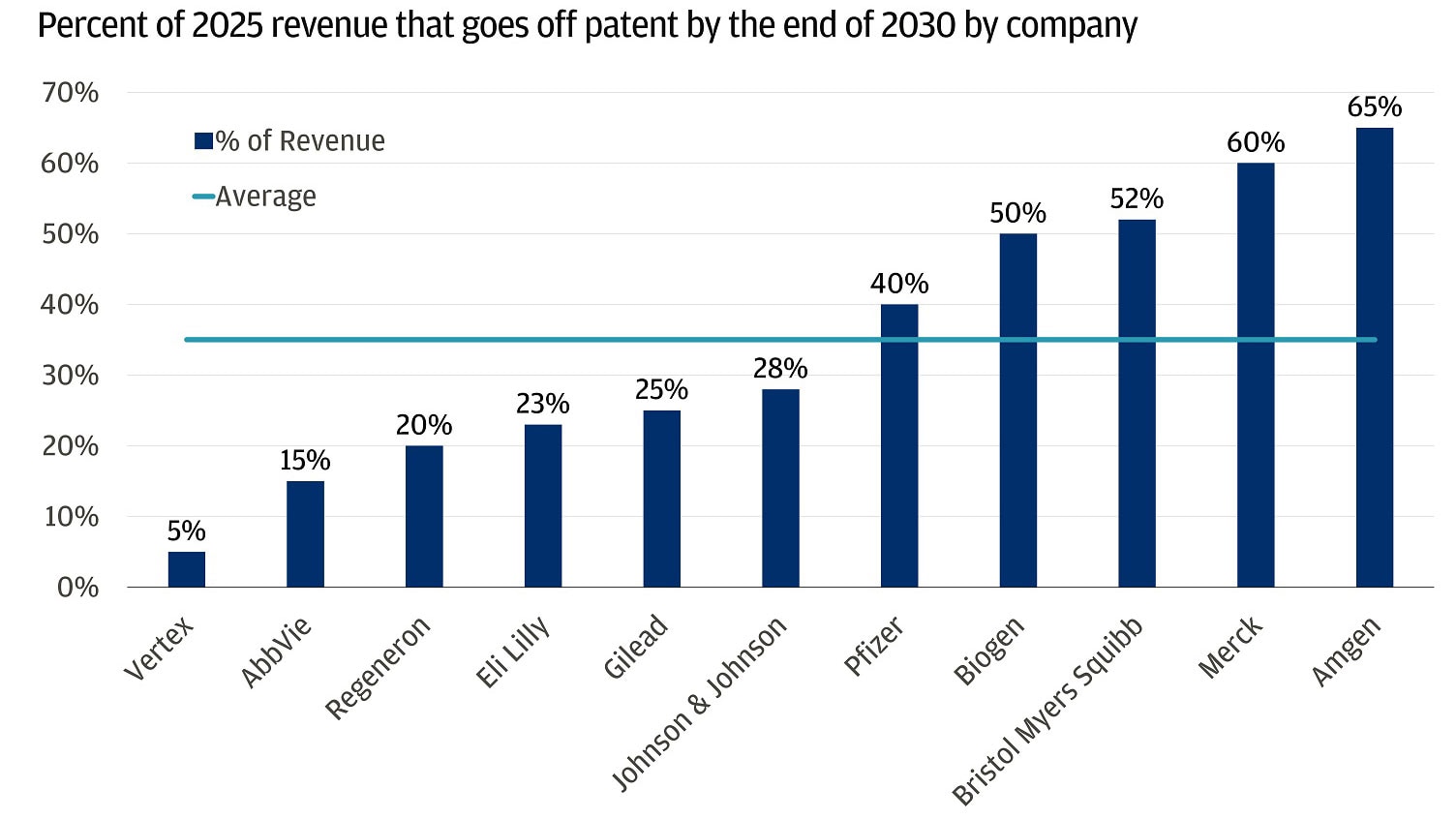

This has ramifications for small-cap biotech, as they are often the primary acquisition targets. However, it also impacts large-cap pharma and biotech companies, which are looking to fill their pipelines as they approach significant patent cliffs through the end of the decade. It is estimated that over $150 billion in revenues will go off patent for large-cap pharma/biotech companies by 2030, representing about 30% of revenue per company on average.

On average, 35% of large cap pharma revenues go off patent by 2030

The bottom line

In summary, after years of headwinds, the health care sector is showing signs of stabilization and renewed momentum. We think that the improving earnings clarity, easing policy pressures and accelerating M&A activity are positioning the sector for a more constructive outlook in 2026 and beyond.

All market and economic data as of 12/05/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

U.S. Equity Strategist, J.P. Morgan Global Wealth Management

Global Investment Strategist