2025 Outlook update: How to parse policy uncertainty

U.S. Head of Investment Strategy

Our 2025 Outlook explored the key dynamics we believed would define the year ahead for investors. There has been no shortage of developments and data points to support or challenge the views we held in December 2024.

Here, in our first-quarter outlook update, we focus on three of those dynamics to consider what has changed, what has stayed the same, and, most importantly, what it means for you and your portfolio. As this is written, equity markets have moved lower on concerns about recently announced U.S. tariffs that would effectively upend eight decades of trade policy. Whatever happens on the tariff front (and we are braced for a rollercoaster ride), policy uncertainty looks to be here to stay.

We make one final observation before we dig in. At a time of policy uncertainty and elevated geopolitical risk – an environment we expect to prevail for some time –strengthening portfolio resilience can help you meet your wealth goals under a range of economic outcomes.

1. Easing global policy

In our 2025 Outlook, we argued that easing global policy (defined by lower policy rates in the United States and Europe and continued fiscal support in China) would support financial markets. Despite sticky inflation in the U.S., we believe the global easing cycle remains on course.

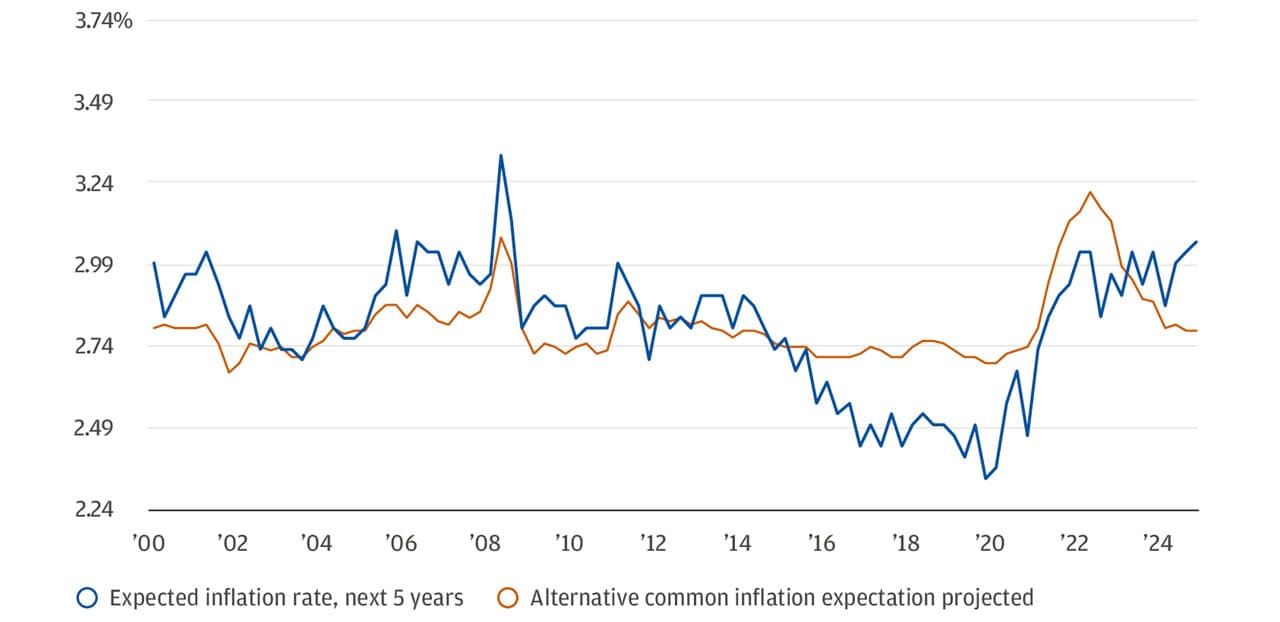

In the U.S., inflation is running close to 3%, but with only very limited signs of excess in the labor market. The quits rate and the hiring rate are at 2016 levels, while wage growth continues to moderate. If there is a risk, it is that tariff uncertainty pushes up inflation expectations. U.S. household surveys already show some signs of rising inflation expectations, but the signal from bond market and professional forecasters is much more muted.

U.S. consumer surveys show rising inflation expectation

In Europe, the growth and inflation backdrop has posed no constraint on policy easing. In early March the European Central Bank (ECB) lowered its policy rate by 25 basis points (bps) to 2.5%. We expect to see further gradual easing as European wage growth seems to have slowed from a nearly 5.5% pace Q3 2024 to 3.5% in Q1 2025.

China continues to deflate its property sector bubble and seeks to limit the economic damage by easing credit conditions for financial institutions. Policymakers’ efforts have been piecemeal so far, but sufficient to stabilize growth.

Overall, the easing bias from the three major economic blocs ought to continue to support economic growth, corporate earnings and bond markets.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

2. Accelerating capital investment

In December, we anticipated that corporate investment would accelerate, driven by companies seeking an edge in the artificial intelligence (AI) race. So far, the AI thesis is on track, but the AI trade is entering a new phase.

The four “hyperscalers” (Microsoft, Alphabet, Amazon and Meta) have increased their capital expenditure estimates by 30%, or $70 billion, from last summer. Indeed, Nvidia, which makes the leading-edge chips that power AI models, recently reported a 70% year-over-year revenue growth rate. However, the market has become more skeptical of hyperscaler spending.

That’s largely because DeepSeek, the now-famous Chinese AI startup, showed that it could create a potentially competitive AI model at a lower cost and with less energy intensity than existing models. Nevertheless, American hyperscalers and companies such as OpenAI and Grok are still incentivized to develop an AI model that can train itself.

While the DeepSeek revelation shook some of the peripheral branches of the AI trade, it makes us more confident in our thesis that AI is likely to be a game-changing technology for the global economy. Indeed, many AI models now track Ph.D.-level output, while costs have decreased by nearly 100% from two years ago. Historically, cost declines in emerging technologies have driven increased adoption and broad productivity benefits. Think railroads and skyscrapers as steel costs declined, air travel as aircraft technology and fuel efficiency improved and software as semiconductor costs dropped.

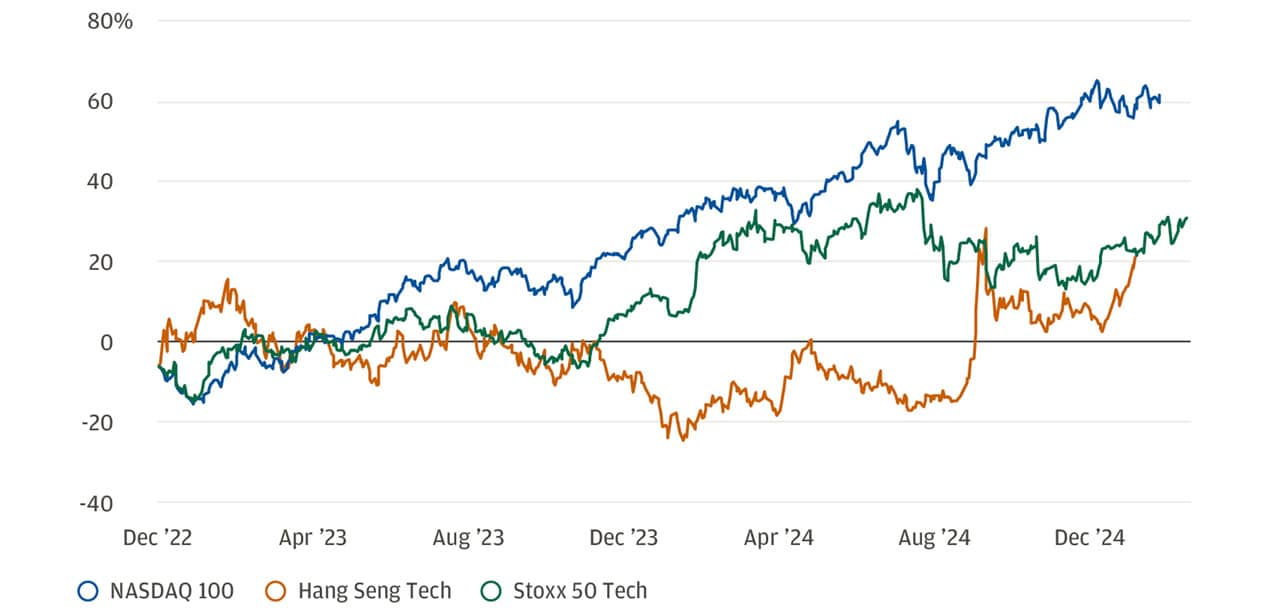

DeepSeek will likely allow more regions, sectors and stocks to participate in any AI-driven rally. Although “Magnificent 7” tech stocks have tumbled during recent market sell-offs, we note that the European and Chinese tech sectors have materially outperformed the U.S. so far this year, and are beginning to catch up on their underperformance since the launch of ChatGPT in November 2022. In our view, the returns from the AI trade will start to shift from the infrastructure providers to the ultimate beneficiaries. We focus on the software and application layers for new investment.

European and Chinese tech companies are beginning to catch to their U.S. rivals

3. Understanding election impacts

Markets initially viewed the election of Donald Trump as pro-growth and capital market-friendly, as investors cheered the promise of tax cuts and deregulations. Bond yields and the financial sector (especially private equity firms) soared between Election Day and Inauguration Day. But the market now takes a very different view of Trump 2.0. Investors’ chief concern: the potential for tariffs (and a possible trade war) to boost inflation and constrain economic growth.

The Trump administration looks to raise tax revenues through tariffs and cut government spending through the Department of Government Efficiency (DOGE). But market action suggests success is far from guaranteed. 10-year U.S. government bond yields peaked around Election Day and have since declined by approximately 50 bps. The yield curve has flattened materially, and “administration aligned” sectors such as private equity have underperformed. Consumer confidence has also failed to maintain the initial “Trump bump.” The S&P 500 is down over 6% from previous peaks.

Investor sentiment could improve with an increased focus on the reconciliation package that Congressional Republicans are shepherding through the House and Senate. Details are still sparse. But the House budget resolution signals that most provisions of the 2017 Tax Cuts and Jobs Act will be extended, offset by significant spending cuts to Medicaid, among other programs. If the reconciliation process is smooth, and investors conclude that tax cuts can stimulate growth without exploding the budget deficit, markets could get a second wind.

In Europe, we see the beginnings of a new regime. European leaders came together to draft a peace plan and build a “coalition of the willing” for Ukraine in the wake of Trump’s contentious Oval Office meeting with Ukrainian President Volodymyr Zelenskyy.

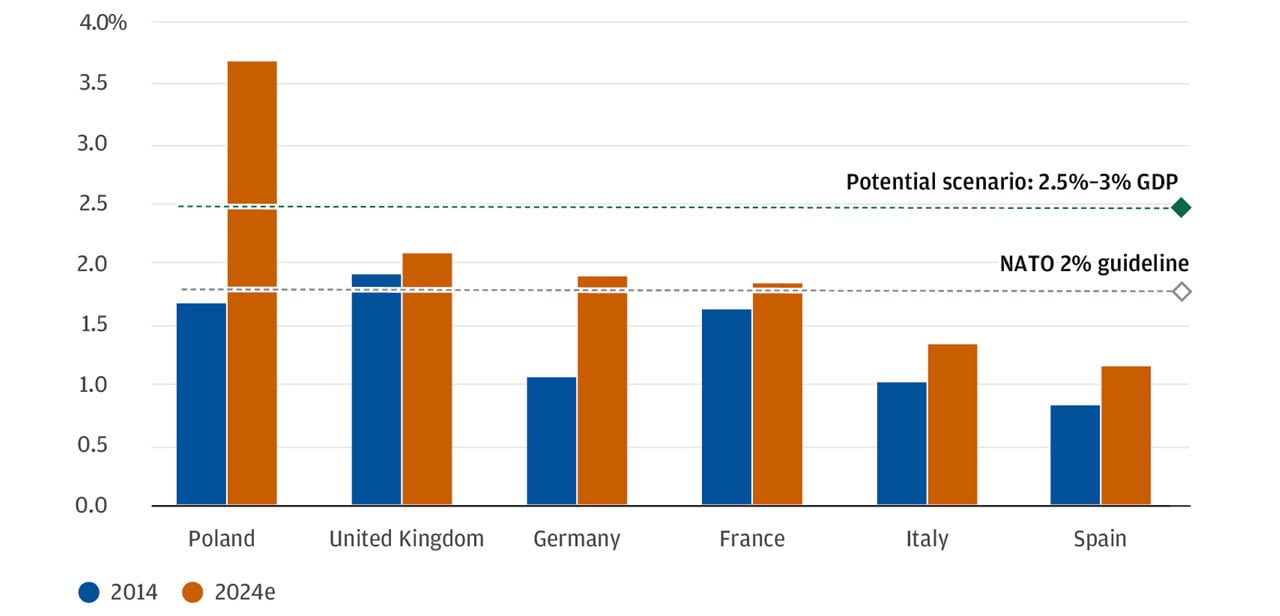

As the transatlantic alliance has frayed, European countries are moving to further boost their defense spending and ensure their own security. In early March, Germany’s likely new Chancellor, Christian Democratic Union (CDU) party leader Friedrich Merz, unveiled a plan to exempt defense spending from Germany’s so-called debt brake. He also announced €500 billion of infrastructure investment. “We will do whatever it takes (for Europe’s defense),” Merz declared. In response, German government bonds saw their yields increase by the most since the Berlin Wall fell, suggesting a major surprise relative to investor expectations for fiscal stimulus.

Security spending by NATO’s European countries could rise to 3% or more of GDP per year, up from an estimated 2% in 2024. Many European countries allowed their military stockpiles to atrophy in the post-Cold War era, and restocking could provide a tailwind to industrial and defense sectors for several years.

More broadly, sluggish euro area growth could pick up in the wake of fiscal stimulus.

A new regime in Europe will feature significantly higher defense spending

The bottom line

Even as markets have wobbled on concerns about the potential damage of a trade war, we believe investors can continue to build on the market strength of 2023 and 2024. The economic cycle looks set to continue, supporting corporate profits and equity markets. At the same time, sticky inflation and policy uncertainty underscore the need to build resilient portfolios by adding assets such as hedge funds, gold and structured notes. Diversifying sources of income remains a priority.

Whatever your family’s goals, our J.P. Morgan advisors are here to guide you.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

U.S. Head of Investment Strategy