Investing in 2026: J.P. Morgan Wealth Management’s top themes to watch

- The era of low inflation and seamless globalization appears to be over, replaced by three transformative forces as we look to 2026: artificial intelligence (AI), global fragmentation and inflation.

- While spending on AI is expanding rapidly – alongside accelerating investment and adoption – questions are being raised about the valuations of the companies driving the technology and strain on local infrastructure.

- The world economy is reorganizing around national security, resource access and supply chain resilience, diverging from the globalization playbook of the past half-century.

- Inflation is no longer just a temporary feature of the post-pandemic economy. As it becomes structural and more volatile, inflation will likely reframe how investors think about income, risk and diversification.

After a year defined by market volatility, trade policy uncertainty and geopolitical tensions – even as the S&P 500 reached numerous all-time highs – the landscape is becoming clearer: The low-inflation, low-volatility era appears to be behind us. The new reality is built around three forces that are reshaping markets: artificial intelligence (AI), global fragmentation and inflation. All have their own trajectories, but in combination they challenge traditional assumptions about growth, pricing power, capital flows and portfolio construction.

J.P. Morgan Wealth Management has just released its 2026 Outlook, providing an in-depth look at these investment themes. Elyse Ausenbaugh, the Head of Investment Strategy for J.P. Morgan Wealth Management, sees this moment as an opportunity to turn “structural change into strategic advantage. By embracing innovation, adapting to a fragmented world and planning for inflation, you can position your portfolio for both opportunity and resilience.”

Here is a breakdown of these three focus areas, which are shaping markets and the global economy as we look to 2026.

Artificial intelligence: Still early, still expanding

AI is already driving real investment, productivity growth and corporate earnings, but the transformation expected from the technology is still in its early innings. The data centers that power AI require dedicated infrastructure and enormous amounts of energy, measured in gigawatts (GW). One GW of capacity costs approximately $50 billion. Planned data center projects totaling 20 GW, then, could ultimately lead to $1 trillion in capital investment. And yet such staggering numbers would still leave current AI spending below 1% of gross domestic product (GDP), compared with the 2%–5% of earlier innovation cycles such as railways, telecom and computing.

What this all means for investors is that value is being created beyond big tech. “Incumbent leaders of the AI trade look likely to keep winning, but the opportunity set has broadened out,” Ausenbaugh shared. “Investors should look across the ecosystem for the companies providing the power, physical and digital infrastructure, and applications of the technology to keep pace with its evolution. Do so with a mind towards diversification – think globally and across sectors.”

Here are some watch items when it comes to AI looking forward:

Spending on AI infrastructure is accelerating. Capital expenditures by the largest U.S. tech companies have grown from $150 billion in 2023 to over $450 billion in 2025. These firms now account for nearly one-quarter of all U.S. capital investment. In 2025, AI-related investment contributed more to U.S. GDP growth than consumer spending did.

The AI wave isn’t limited to one country or region. The U.S., China, Europe and Saudi Arabia are deploying sovereign-level investment programs in data centers, chip design and infrastructure. When it comes to AI research, some reports suggest China is leading the pack. In fact, Chinese authors accounted for 40% of global citations in AI research publications in 2024, ahead of the U.S. and Europe.

Adoption is also expanding. Nearly 45% of U.S. businesses now pay for access to large language models, and about 10% are using AI tools to supply goods and services. Consumer adoption is accelerating, as well, with ChatGPT reported to have seen growth in usage from 400 million active weekly users in February 2025 to more than 800 million active weekly users in October 2025.

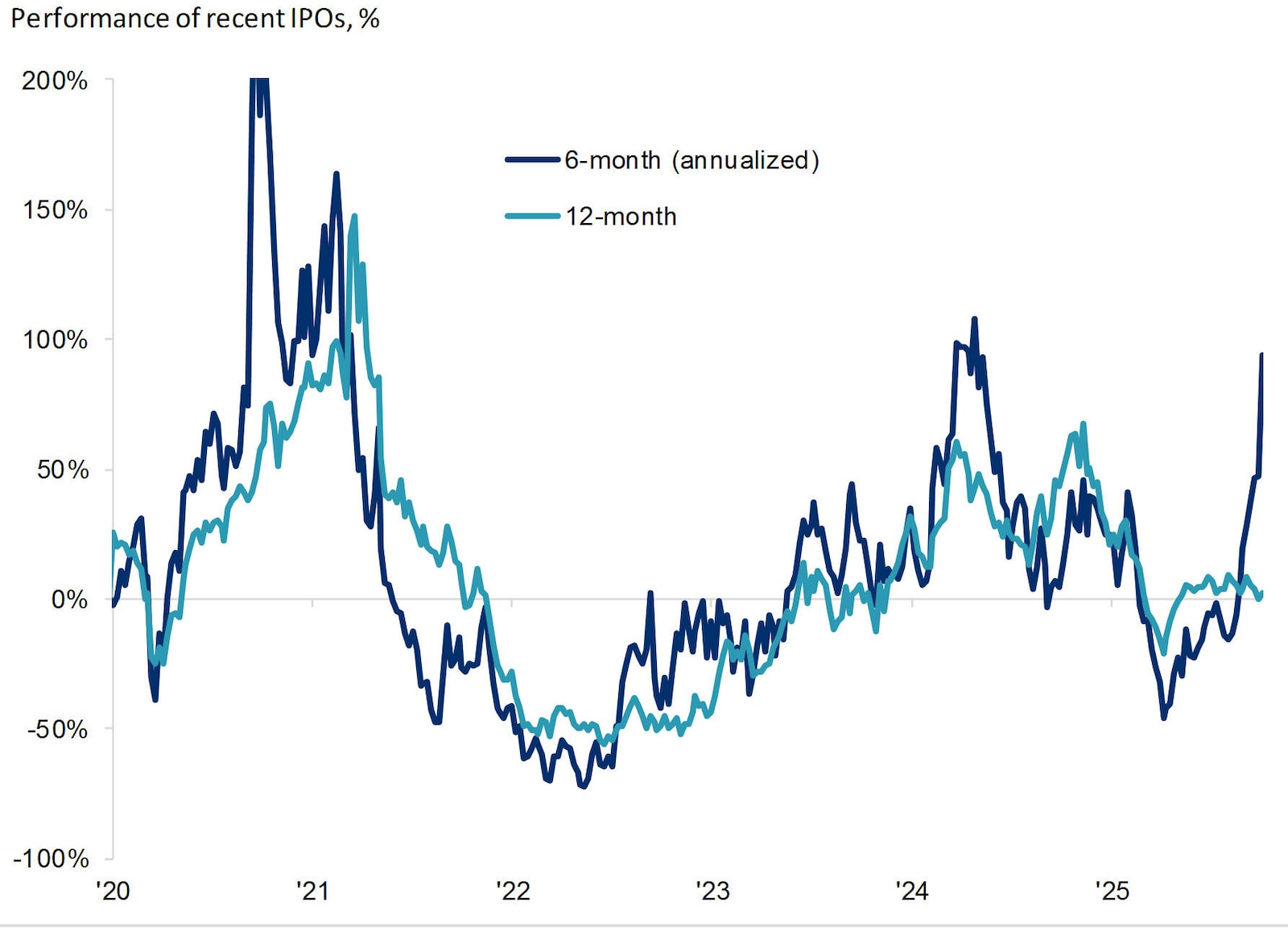

AI growth has sparked debate over whether a bubble is forming, and some signs are there. Exuberance is building, and valuations for private AI startups have surged well ahead of earnings. In public markets, though, revenue and profit growth are still leading the story: For example, Nvidia’s stock price has risen 13x over the past five years, but its earnings have increased 20x.

U.S. IPO performance showing more signs of exuberance

The bigger question may be who captures the long-term value. In past technology cycles, first movers didn’t always win. Railways, telecom and fiber optics all saw early investors lose money before the ecosystem had matured. Today’s large tech firms are growing earnings at an annual rate of 20%. Whether they maintain that lead depends on execution and adaptability.

Infrastructure remains a bottleneck. Power demand from AI data centers is expected to exceed the annual generation of Texas and California combined by decade’s end. Grid expansion has been slow, and about 70% of U.S. power transmission lines are more than 25 years old. Project delays and local resistance are already slowing development in some regions.

Get up to $1,000

When you open a J.P. Morgan Self-Directed Investing account, you get a trading experience that puts you in control and up to $1,000 in cash bonus.

Global fragmentation: Resilience over reach

AI growth isn’t the only force driving markets at the moment. Ausenbaugh notes there were “multiple signs of fragmentation in 2025, from significant trade policy changes and investment commitments to geopolitical conflicts and competition for technological leadership.”

How should investors respond? “As the world order – and perhaps market norms – shift, consider ways to bolster portfolio resilience and rebalance towards potential beneficiaries,” per Ausenbaugh.

Here are important areas to watch in the coming year:

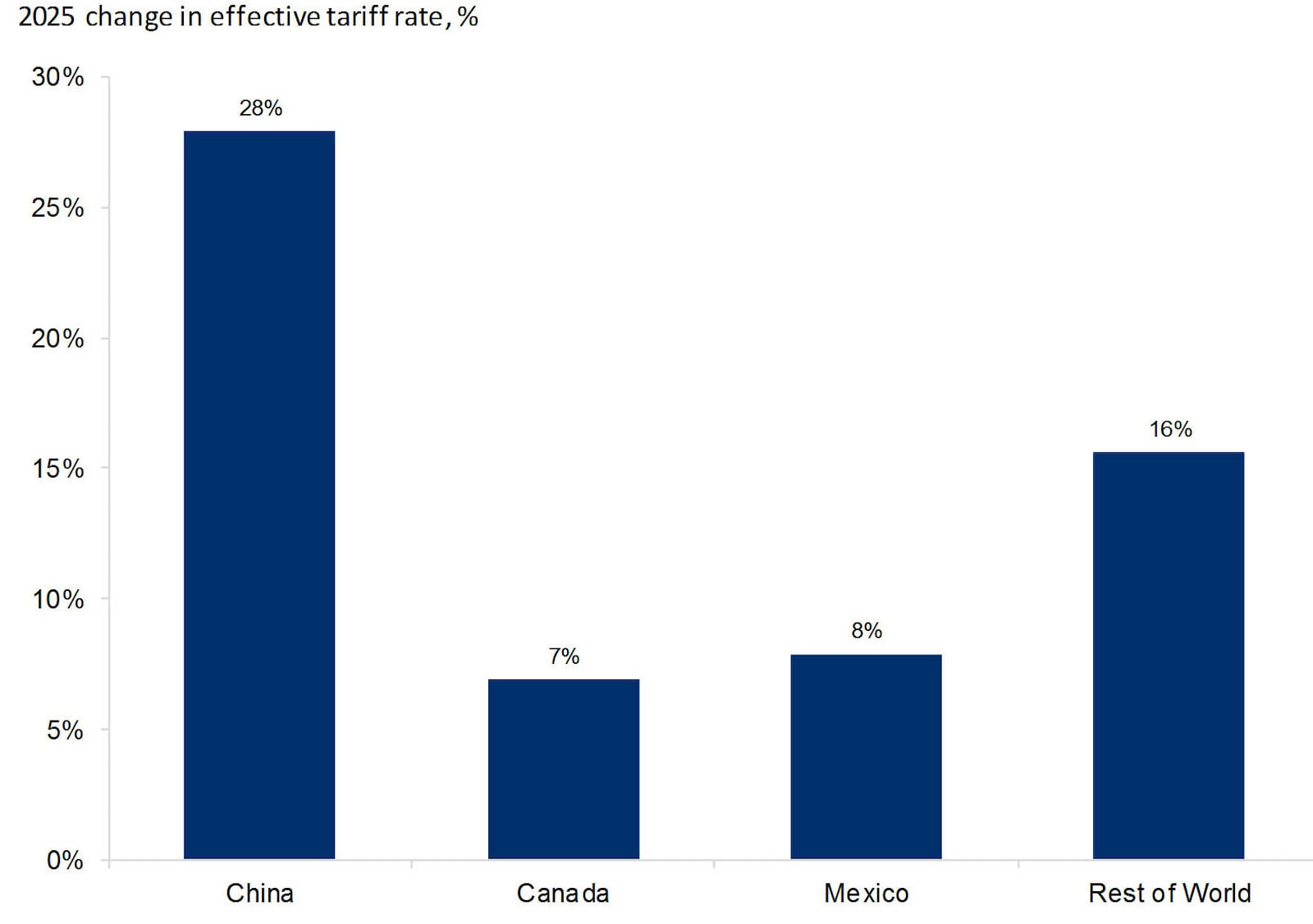

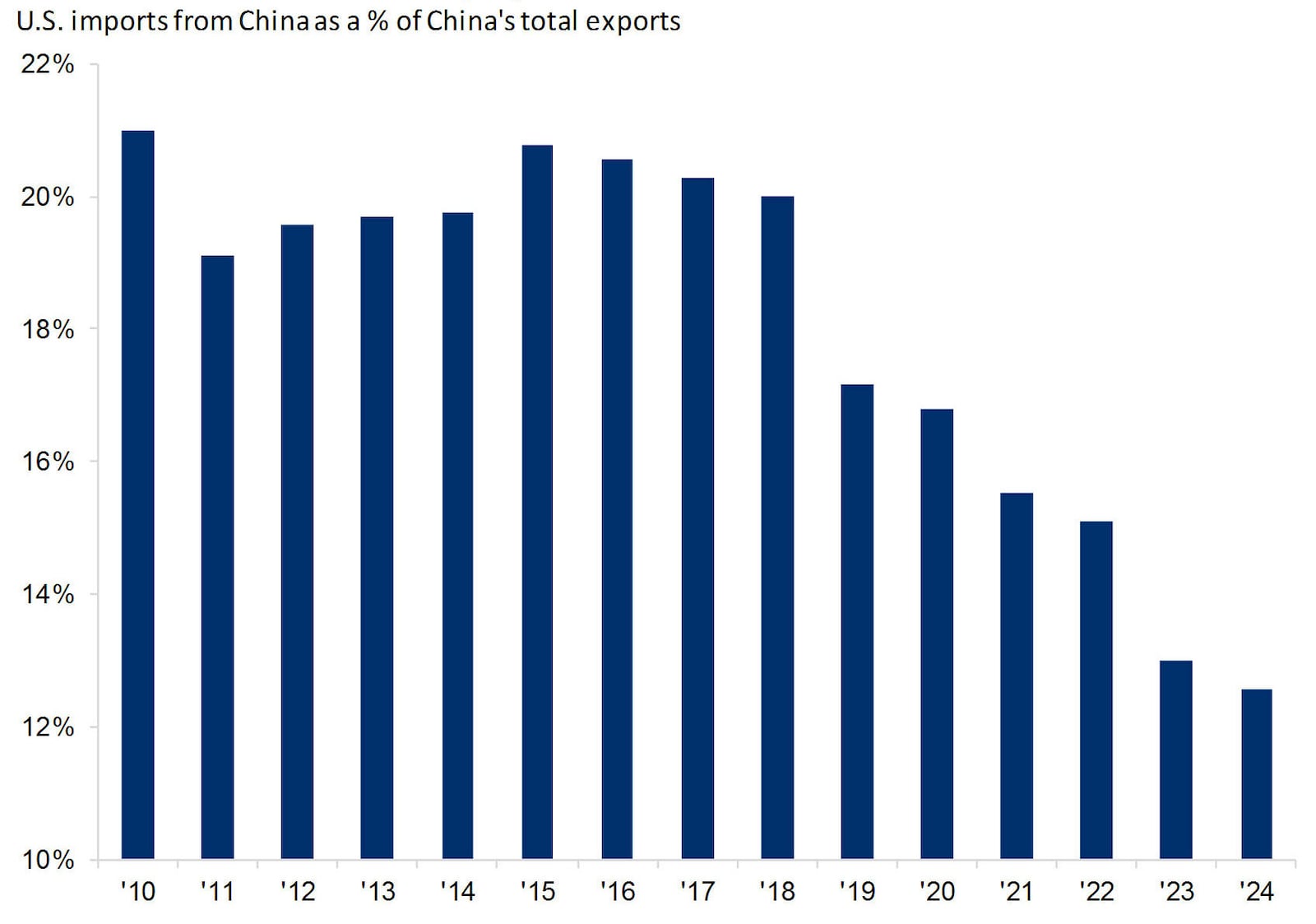

The era of seamless globalization has ended. Trade relationships once organized around efficiency are now influenced by tariff structures, political alliances and security concerns. Indeed, tariffs now affect nearly 70% of goods imported into the United States. Total U.S. imports from China have fallen from 22% in 2017 to 12% today; meanwhile, China’s share of U.S. Treasury holdings has dropped from 14% to around 6%.

The Trump administration seems to be carving out a North American trading bloc

The White House seems to be carving out a North American trading bloc

The U.S. and China have been decoupling since 2018

At the same time, new regional blocs are forming. Mexico is drawing manufacturing activity as firms seek proximity and greater trade certainty. Europe is increasing its defense spending. Tariff and regulatory barriers are creating clear winners and losers.

Energy is at the center of the shift. Natural gas plays a growing role in supporting power reliability in Europe and Japan. To meet its needs, the European Union has pledged to purchase $750 billion in U.S. energy through 2028. Attracting both public and private investment flows, energy and defense are emerging as critical components of regional strength.

Central banks and investors are turning to gold and digital assets as hedging tools. Indeed, gold prices are up nearly 40% in 2025. Meanwhile, cryptocurrency assets now have a market cap above $4 trillion – more than double from the previous year.

Inflation: More volatile, yet more persistent

Ausenbaugh notes that “investors didn’t have to worry much about inflation in the decade following the financial crisis, but that’s changed.” Today, inflation is structurally higher and more responsive to shocks than it was in the previous decade. “It is crucial to be intentional and assertive about managing inflation risk in financial plans going forward,” Ausenbaugh said.

Here’s what’s noteworthy when it comes to the current state of inflation:

Behavior has changed. Businesses adjust prices and wages more frequently, and consumers are forced to respond accordingly. Dynamic pricing tools allow real-time updates, making prices even more responsive to demand.

Capacity is limited. Housing, labor, power and raw materials all face structural shortages. Cement production, for example, is down 15% from its 2005 peak, limiting new building capacity. These gaps create pricing pressure that doesn’t ease quickly.

Policy may amplify inflation – not suppress it. Governments across developed economies used aggressive stimulus measures amid the COVID-19 crisis and may do so during the next downturn. Such interventions change the inflation risk profile for portfolios.

Traditional 60/40 portfolios are feeling the pressure. Portfolio volatility has nearly doubled since the pandemic. Bond yields have reset higher, but stock-bond correlations remain less reliable. This has called into question the 60/40 portfolio balance – a ratio of stocks to bonds broadly suggested by financial advisors for decades. Inflation-linked bonds, infrastructure, commodities and real assets are seeing renewed interest as potential stabilizers.

The bottom line

The outlook for 2026 reflects a shift in structure, not just in sentiment. AI is driving new rounds of investment and productivity but also raising real questions about capacity and returns. Fragmentation is changing how trade flows, how companies manage risk and where growth occurs. Inflation is back in focus as a key portfolio variable.

These forces aren’t moving in isolation, either: They’re interacting with one another, raising new questions about portfolio diversification, policy response and asset selection. The direction is clear, even if the outcomes are not. Positioning an investment portfolio with clarity, flexibility and an eye toward structural durability will matter now more than ever.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.