Are Americans too pessimistic? Comparing consumer sentiment to the real US economy in 2026

Global Investment Strategist

- Americans’ pessimism is understandable – even if it doesn’t align with current economic conditions. Prices for everyday essentials still seem high compared to pre-pandemic norms, borrowing is more expensive than it was a few years ago and job-switching confidence has cooled. Together, these pressures can drive “bad vibes.”

- The economy can seem weak while markets hold up – because they respond to different things. Households generally focus on the cost of living and job security, while markets are forward-looking and earnings-driven. This gap helps explain why sentiment can slump even as growth and equities remain resilient.

- For investors, the goal isn’t to trade the mood – it’s to watch the signals that turn stress into fundamentals. The most important watchpoints in 2026 are whether inflation spreads beyond energy, whether labor market conditions meaningfully deteriorate and whether household credit stress (like delinquencies) continues to broaden.

Summer in America is generally a season of optimism. Airports are packed, restaurant patios are bustling, and friends and family are gathering at outdoor celebrations. This year, World Cup matches add another layer of energy to the national mood. On the surface, the economy looks lively.

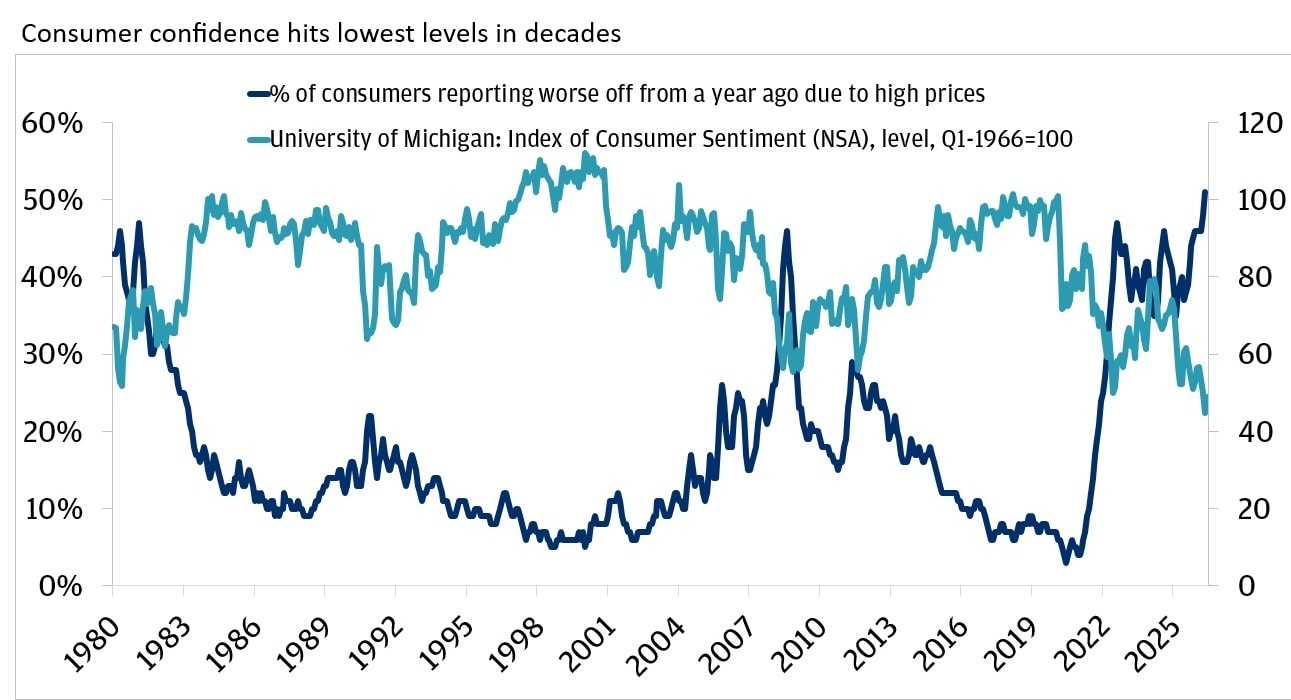

Yet beneath the summer buzz, a different story is taking shape. Multiple consumer surveys suggest Americans are feeling increasingly uneasy about their financial situation. According to the Federal Reserve Bank of New York’s Survey of Consumer Expectations, over 43% of households feel "somewhat worse off" or "much worse off" compared to a year ago, the highest reading since January 2023. The University of Michigan’s Consumer Sentiment Index – a monthly survey tracking financial confidence across U.S. households – saw one of its weakest readings in decades, sitting nearly 20% below where it stood a year ago and at levels historically associated with recessions.

How Americans feel about the economy matters. When households believe they are worse off, they may pull back on discretionary spending, delay major purchases or become more cautious with investments – decisions that can ultimately ripple through the broader economy.

And yet the broader economy reveals a more resilient narrative. Real consumer spending continues to expand, the U.S. economy is still growing and equities remain near all-time highs. The economy can seem weak while markets hold up. This disconnect between how the economy seems and how it is performing is often referred to as a “vibecession.”

Americans are feeling the pinch: What’s driving the ‘vibecession’?

At the start of 2026, we examined how “affordability” explains much of the gap between economic data and consumer sentiment. That dynamic remains firmly in place as we near the midpoint of the year. According to the University of Michigan, over 50% of consumers report being worse off compared to a year ago due to high prices.

May consumer confidence hits lowest level in decades partially driven by high prices

For many households, the issue is not that prices are still rising rapidly; it’s that they never come back down. The pace of inflation has certainly slowed from its June 2022 peak of 9.1%, but the level of prices (particularly for essentials like housing, food and energy) remains elevated compared to the pre-pandemic baseline. Indeed, it’s price levels – not the rate of change – that can potentially shape how consumers experience the economy day to day.

Borrowing costs have amplified that pressure. Compared with the ultra-low rate environment of 2020–21, higher interest rates have helped push up the cost of financing for many Americans across mortgages, auto loans and credit cards, potentially tightening financial flexibility and weighing on some household budgets.

Energy volatility has also contributed to weakened sentiment. Gasoline prices have skyrocketed over the past year, up roughly 42% from May 2025 to May 2026 – largely because of oil supply concerns amid the conflict in the Middle East. Gas prices, displayed on large signs at fuel stations across the country, are one of the few economic variables households see in real time, and such visibility may in fact give them an outsized influence on consumer sentiment. Prices have moderated over the past few weeks, but the impact of higher prices is real.

At the same time, the labor market – while still healthy in aggregate – feels less secure at the margin for some. According to the New York Fed’s Survey of Consumer Expectations, confidence in the ability to find a new job within three months after a job loss has declined to levels comparable to those seen around April 2020. The recent labor market has been characterized as “low hire, low fire” – a dynamic that can feel stable for those who are employed but potentially increasingly difficult for job seekers. It can also weigh negatively on sentiment.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

What’s weighing the economy down? Changing interest rate expectations and geopolitical concerns are adding complexity

While the concept of a vibecession speaks to how people feel, similar forces also act as constraints on the economy. This year, fluctuating interest rate expectations and geopolitical concerns have shown up in force.

Earlier in the year, before the escalation in the Middle East, markets expected the Federal Reserve (Fed) to deliver nearly 50 basis points of rate cuts in 2026. That outlook has whipsawed, with markets now pricing in the possibility that rates remain higher for longer, and even the risk of potential hikes later this year as energy-driven inflation has helped cloud the Fed’s policy path.

The shift matters because higher interest rates can help keep borrowing costs elevated across the economy. Indeed, higher rates can potentially translate into higher monthly payments for households and elevated financing costs for businesses, potentially acting as a drag on economic activity.

It’s important to note, however, that not all inflation is the same. The recent pickup in inflation has been driven largely by energy, not by broad-based demand. In our view, for the Fed to hike rates, inflation would likely need to spread more broadly into wages and services. We don’t see that dynamic in place currently, which is why we currently believe the Fed will remain on hold this year.

Even so, a higher-for-longer rate environment implies that pressure from borrowing costs may not disappear quickly. Over time, that could act as a gradual squeeze on household balances and economic activity. At the same time, geopolitical risk remains a key uncertainty. Even if de-escalation is the most likely path, the events of the past several months demonstrate just how quickly energy prices can fluctuate.

What’s going right in the economy? Shock absorbers are helping to keep the expansion intact

Despite historically low sentiment and ongoing risks to the outlook, U.S. real gross domestic product (GDP) increased at an annualized rate of 1.6% in the first quarter of 2026, suggesting continued resilience.

We think it’s useful to view the economy through the lens of shocks and shock absorbers. The pressures that households are facing are real, but so are the mechanisms that help offset them.

Elevated energy prices stemming from the conflict in the Middle East represent a clear shock, particularly for lower-income households that spend a larger share of their take-home pay on fuel and utilities. A concern is that higher energy spending could crowd out other consumption, potentially reducing discretionary demand and slowing overall growth. Several factors in the economy are acting as shock absorbers, helping to cushion that blow.

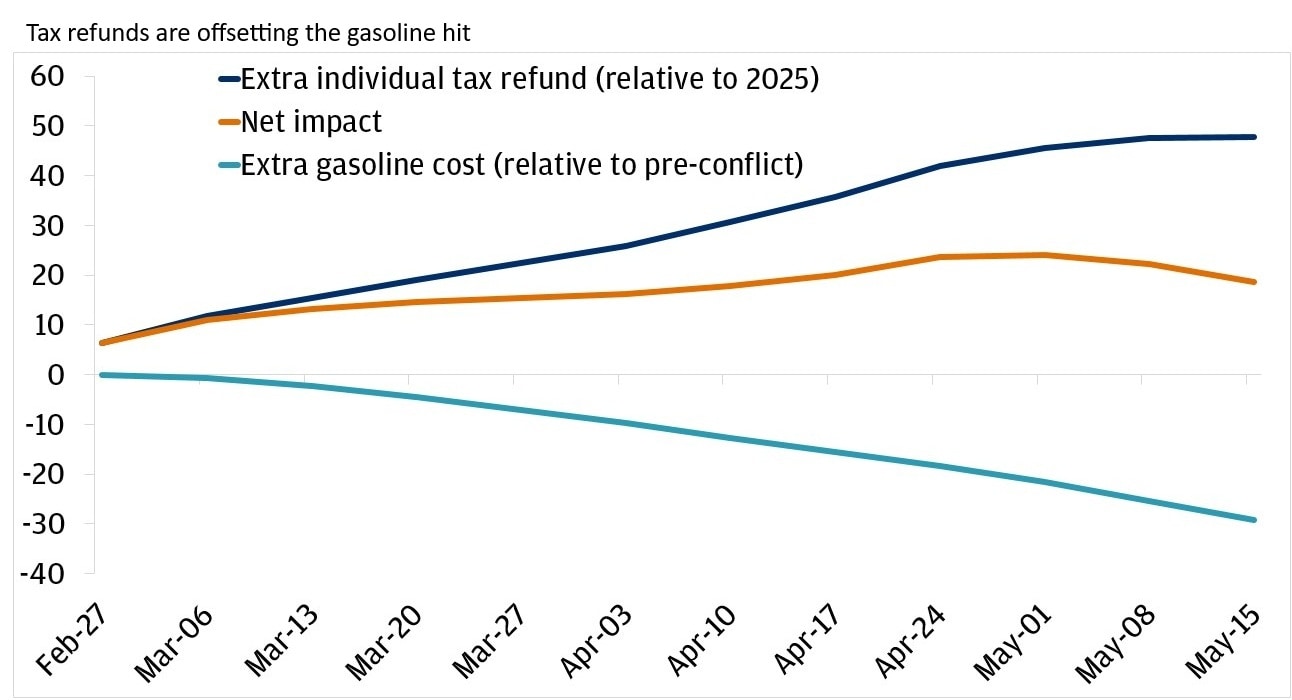

One example is the additional tax refunds some Americans received under the One Big Beautiful Bill Act, which have helped offset elevated gasoline prices.

Tax refunds are offsetting the gasoline hit

With tax season behind us, the boost from tax refunds is likely in the rearview mirror, but another positive catalyst for many Americans could be a continued de-escalation of the war and reopening of the Strait of Hormuz. Over the past couple of weeks, some pressures have eased, with the average national price of a regular gallon of gasoline below $4.00 for the first time since late March.

Against this backdrop, consumer spending is another factor at play. Higher-income households, which are less sensitive to higher energy prices and borrowing costs, account for nearly 60% of total consumer spending. This matters because their spending is less susceptible to energy price shocks. Even if lower-income households pull back, the overall level of consumption can remain resilient. This environment can help explain why the economy could be positioned for continued growth, even if sentiment remains weak.

In addition, the S&P 500 is trading near all-time highs, supported by a meaningful pickup in earnings – not just valuation expansion. The index delivered impressive Q1 2026 earnings results, reporting 28% year-over-year blended earnings growth, the strongest quarterly result since Q4 2021. A key driver behind this strength has been ongoing investment in artificial intelligence (AI) and the hardware that powers it, including semiconductors.

Importantly, it’s not just technology delivering impressive results, with 10 of the 11 industry sectors reporting positive Q1 earnings growth and 85% of S&P 500 companies reporting actual earnings per share above estimates. This environment of strong earnings may help explain why markets have been able to remain resilient even amid poor sentiment.

The pressures Americans are facing are real, but so are fundamental economic drivers

Americans aren’t wrong to feel cautious. The pressures they may be experiencing, from higher costs to tighter credit conditions, are real and meaningful, especially when compared to the pre-pandemic cost of living and rate environment.

However, data shows the broader economy might be more resilient than sentiment alone suggests. The current disconnect between weak sentiment and relatively solid fundamentals could persist, but it may be helpful to understand that households and financial markets are influenced by different things. Consumers often experience the economy through prices and job security, while markets tend to be forward-looking and focused on future earnings.

As investors, that distinction matters. Rather than making portfolio decisions based on vibes, the best course of action is often sticking to a plan and focusing on the fundamentals that can drive markets in the long term.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Global Investment Strategist