How the market’s inflation fears are running ahead of reality

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

By Kriti Gupta and Nick Roberts

As we look ahead to the remainder of 2026 and the dynamics shaping the world in our Mid-Year Outlook, it’s clear that artificial intelligence, global fragmentation and inflation will continue to permeate throughout economies and the markets.

Inflation in particular is all the more likely to resettle at a stickier zone, potentially for years to come. Energy prices will likely command a more permanent geopolitical risk premium, while supply chains will be rerouted to guarantee national energy security – and not necessarily at the lowest possible cost. Even if inflation isn’t currently an outsized risk, it is becoming more of a factor.

America’s tightrope walk

There is a renewed premium on bringing supply chains closer to the end consumer, building and adopting new technology, and securing it all. Whether it’s countries and governments or corporations and ordinary citizens – there is a willingness to pay more in preparation of an economic shock, something that has become more and more common. That inherent demand worldwide means inflation is likely to become more tilted to price changes in physical goods rather than wages and labor.

Now, add on the impact of the conflict in Iran and the Strait of Hormuz. Recent memory would suggest that higher energy prices would push central banks to hike interest rates in response. At least, that’s what the market is pricing. Investors started 2026 expecting the Federal Reserve (Fed) to cut rates by half a percentage point. Those bets have evaporated, and 30-year U.S. bond yields have breached 5% again. But a shift in messaging from the Fed toward a renewed hiking cycle is unlikely to materialize.

History shows – with the exceptions of the 1970s and 2022 – the Federal Reserve is more likely to ease rates into oil shocks for fear of demand destruction from prolonged higher energy prices.

But in the face of continued robust economic data and higher headline inflation currently running at 3.3% year-over-year, the Fed is more likely to be on hold. Despite not cutting rates, this could still end up being stimulative to risk assets as inflation-adjusted rates fall.

Canary in the coal mine

How do you know when it’s time to hike? The early signal might lie in Latin America.

Due to the region’s exposure to commodity fluctuations, monetary policy has been more reactive to inflationary risk. Over the past few decades, and decisively since the COVID-19 pandemic, core Latin American central banks have shifted from policy takers to cycle leaders, leading both tightening and easing phases.

Before the turn of the century, they were largely policy takers – constrained by weak inflation credibility, currency vulnerabilities and the need to shadow the Federal Reserve.

After a series of institutional changes related to target inflation frameworks, operational independence and floating exchange rates, Latin American central banks became more credible. By the financial crisis, they developed the ability to ease counter-cyclically without destabilizing their currency – a delicate balance.

But after the COVID-19 pandemic, a period that saw roaring demand after the economy reopened, Latin American central banks were the first to kick off what would later be known as one of the sharpest tightening cycles in history.

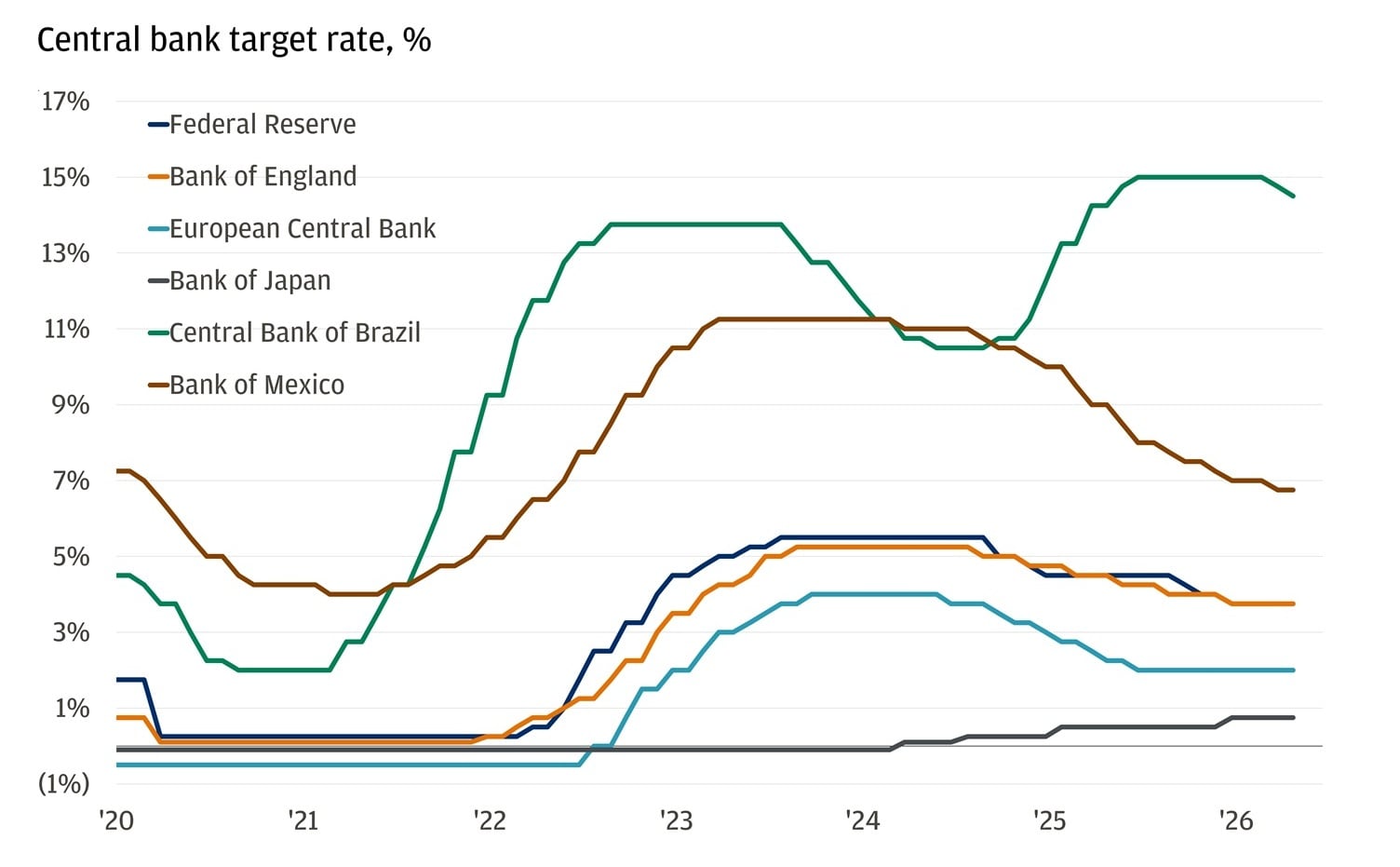

The Bank of Brazil started raising rates in March of 2021. The Bank of Mexico followed in June of the same year. Six months later, the Bank of England – known for being more responsive among G-10 central banks – also hiked rates followed by the Federal Reserve and eventually the European Central Bank.

It happened again as rates normalized. The two largest Latin American economies started cutting rates first, setting a new tone and going from policy takers to cycle leaders in both directions.

LatAm central banks have been ahead of the curve

The implication is structural: Latin America no longer imports global monetary cycles to the degree it has historically. Instead, it increasingly provides signals on inflation credibility, real‑rate turning points and policy normalization – especially as commodity prices drive the impulse.

And right now, inflation is within the bands of tolerance across most major Latin American economies. In using Latin American monetary policy as a guiding light of potential changes in global rates, the message is clear: We’re not there yet.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Pressure point

Already facing a more subdued growth outlook, economies navigating trade shocks on the back of higher energy prices – like the U.K. and Eurozone – have seen markets pricing as many as three rate hikes in this year from their respective central banks.

The policy rate repricing has pushed longer-dated bond yields to new highs in the United Kingdom. Whereas in other parts of the world, there are more factors to consider, the 70-basis-point move in 10-year gilt yields is largely linked to the inflationary impact of the war. For the fifth year running, inflation sits well above the Bank of England’s 2% target.

A quick resolution to the war and subsequent fall in commodity prices could see yields fall sharply in the U.K. and Eurozone as market expectations for rate hikes unwind. While a prolonged conflict may exert further upward pressure on yields, it also comes with downside risks to growth, serving as a cap to surging bond yields.

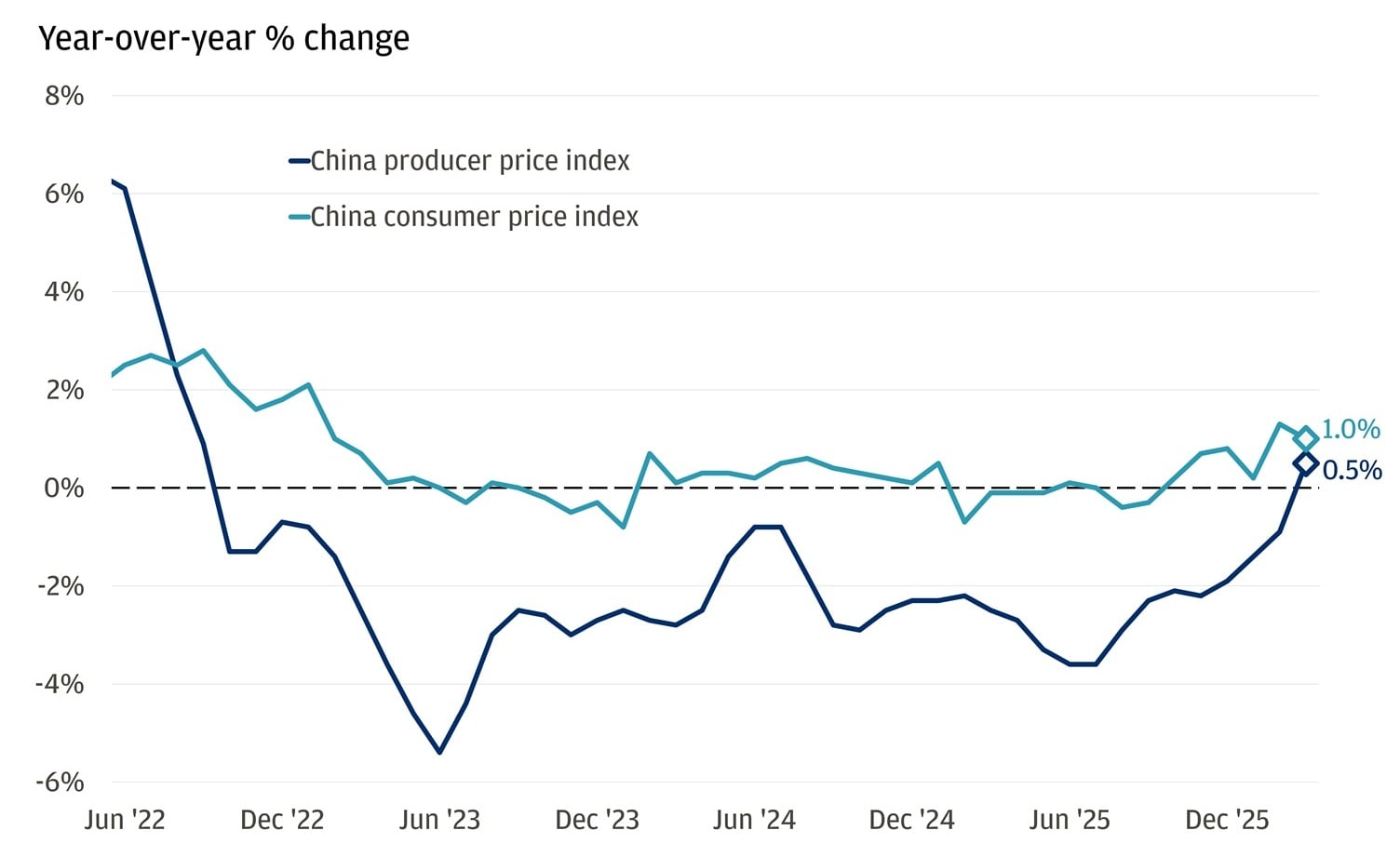

The exception: A note on China

China stands apart: It does not face inflation risk but instead exports deflationary pressure. Given China's scale and role as the largest manufacturer in the world, that matters globally.

Consumer inflation in the country remains subdued while producer prices continue to reflect excess capacity and weak pricing power. Marry that with a housing slump and declining export prices, and the dynamic has a tendency to spill over into global markets if persistent – exerting downward pressure on global goods inflation through manufacturing, exports and supply chains.

China’s inflation measures are near zero

All market and economic data as of 05/08/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank