The world changed in 10 days: An oil unwind and a hawkish Fed

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

By: Kriti Gupta and Nick Roberts

In just 10 days, the world changed – Kevin Warsh’s debut as chair of the Federal Reserve (Fed) compounded with an oil unwind. The two tenets that have been driving financial markets for the past few months flipped.

On the back of the conflict in Iran, oil climbed as high as $126 per barrel in late March. Prices have fallen since by over 40% in about 60 days, with the steepest leg of that trade coming in the last few weeks. For everyday Americans, that has lowered the average national price of gasoline from a peak of over $4.50 per gallon to below $4.00 – a boon for those worried about energy prices potentially curbing consumer spending.

Perhaps the real sea change came from Kevin Warsh’s first Federal Open Market Committee (FOMC) meeting mid-June. Long perceived as someone with an easing bias, Warsh’s debut as Fed Chair marked a hawkish departure from expectations toward the end of his predecessor’s tenure. Investors had already largely priced out interest rate cuts ahead of his debut, in reaction to commodity-driven inflation and firmer economic data.

“Pencils with big erasers”

In theory, inflation running above the Fed’s 2% target provides little reason to cut interest rates. But during the late innings of Chair Powell's tenure, perceived weakness in the labor market allowed just that. And a series of “insurance cuts” helped power risk assets.

As a result, investors also flocked to real assets representing stores of value that wouldn’t be eroded by inflation. Take gold as an example. Its rise from $3,500 per troy ounce in September 2025 to a peak of just under $5,500 in January 2026 was symptomatic of this policy stance by the Fed.

Chair Warsh's debut at the June FOMC meeting broke that mold.

The policy statement of Warsh’s first meeting as chair was drastically shortened, with forward guidance eliminated and language interpreted as an easing bias removed. The Summary of Economic Projections (SEP) showed an upward revision to inflation and a hawkish tilt in the dot plot. The vote was framed as "unambiguous and unanimous" on delivering price stability, and marked a stark contrast with the Powell-era communication-heavy, guidance-dependent approach.

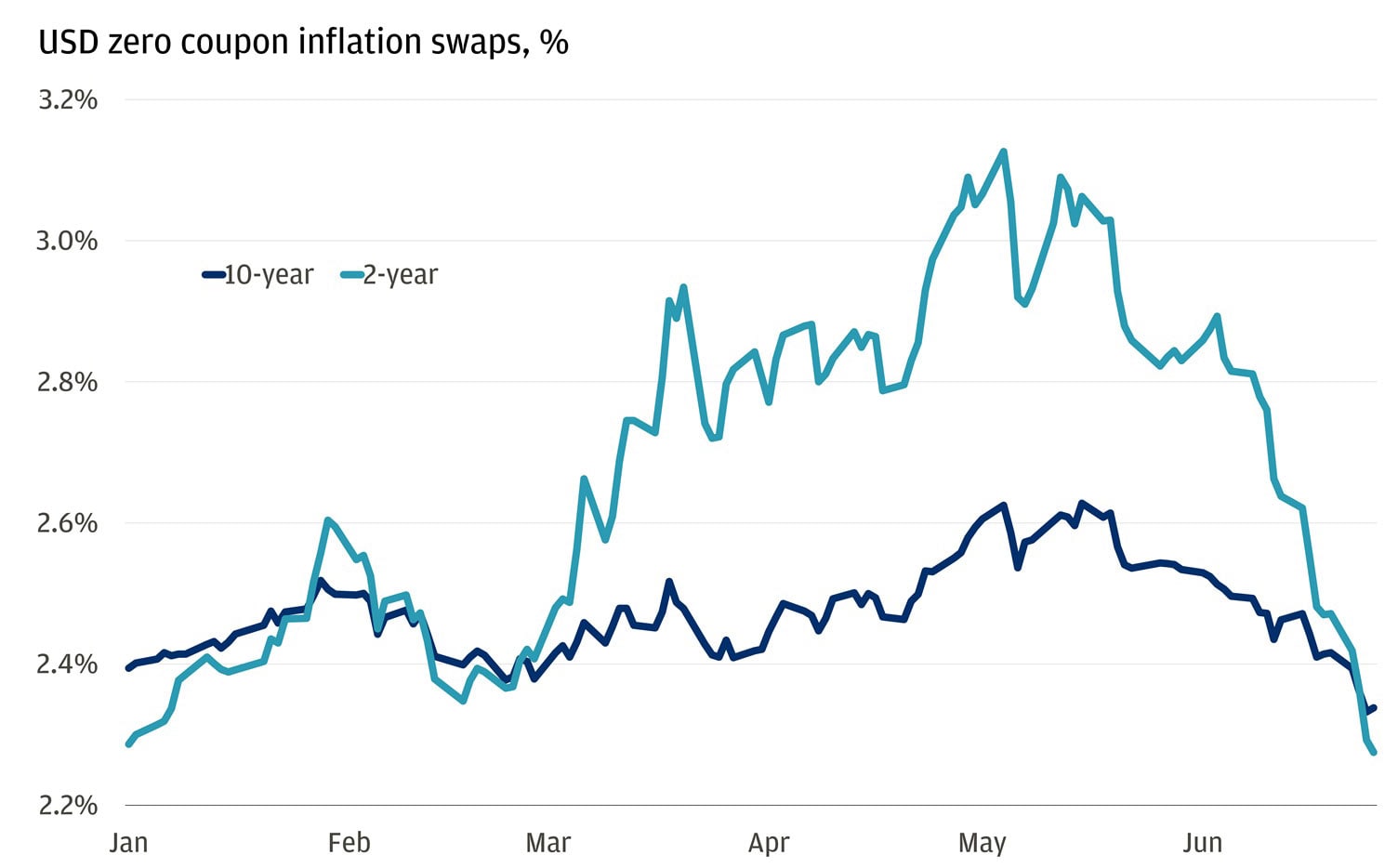

Chair Warsh went so far as to mention the forecasts were “coming in with pencils … with big erasers,” acknowledging the drivers of the global economy and the United States are changing quickly. But the idea of a Federal Reserve less willing to tolerate above-trend inflation is already having a material impact. Market-implied inflation expectations have fallen sharply, with both two-year and 10-year inflation swaps now below pre-conflict levels.

Inflation expectations are falling

In other words, a renewed willingness to hike interest rates (or even the absence of an easing bias) gives the bond market far greater conviction in lower long-term inflation – especially when faced with the prospect of higher oil prices.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Halved in 60 days

But what if higher energy prices aren’t a problem anymore?

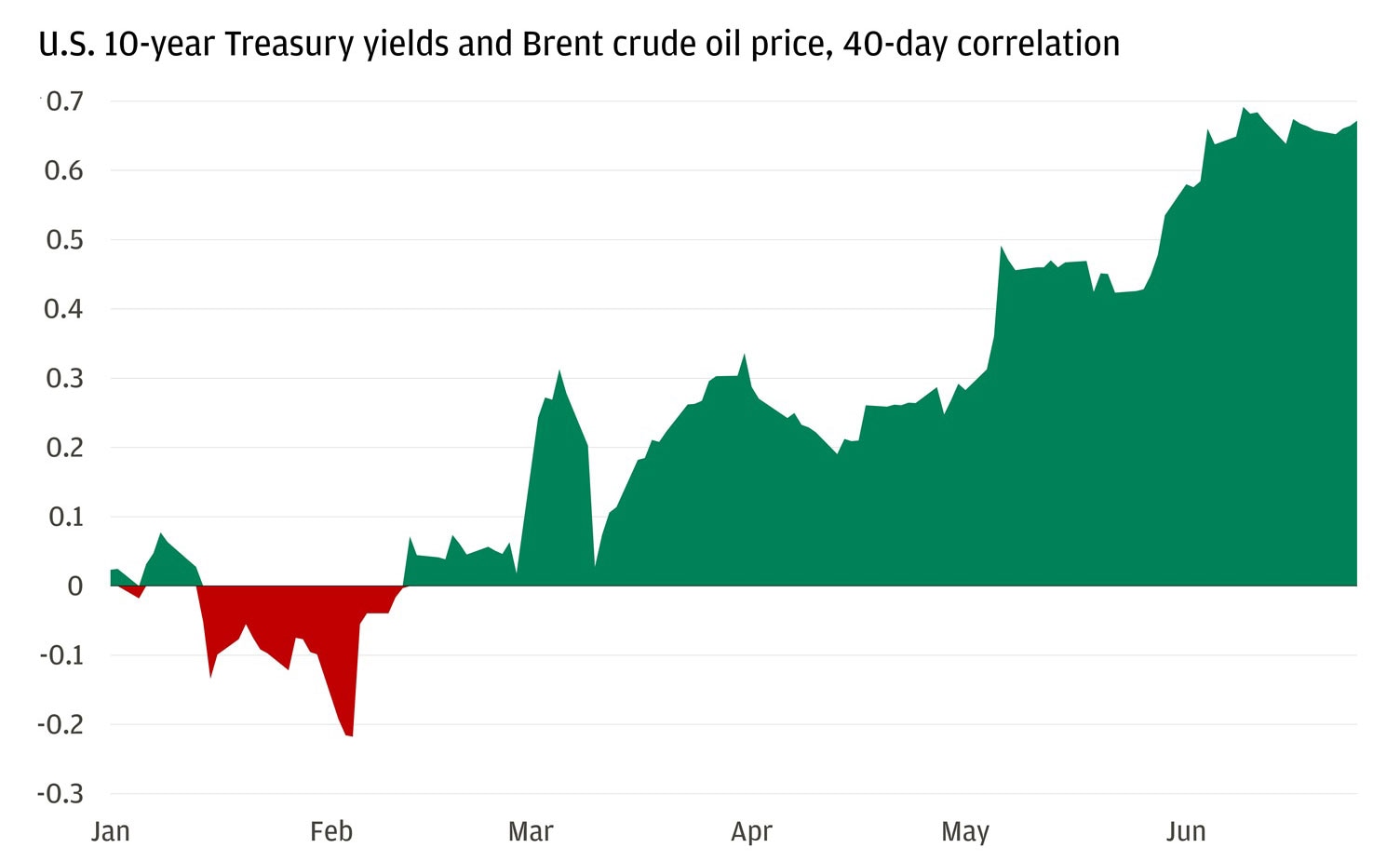

The last two inflation reports were primarily driven by the energy shock (making up almost half of the headline number), with nearly a $20-per-barrel drop in oil prices in June yet to be reflected in the latest inflation reports. Nationally, gasoline prices have already followed the decline in the benchmark, but the more notable move is in the bond market. Since the start of the conflict in Iran, the 40-day correlation between bond yields and oil prices has risen, with the two assets moving in lockstep. The logic is simple: Higher oil prices are inflationary and therefore part of the decision-making process for monetary policy, which is then reflected in the bond market.

Bond yields are increasingly moving in step with oil prices

But now, with lower oil prices and an interpretation of the Federal Reserve that veers hawkish, economic data and, specifically, the labor market, remains key. One of the biggest overhangs on the global economy is dissipating, and now investors are questioning whether higher oil prices are the only path to a Federal Reserve that takes a step toward tighter monetary policy, not looser. But with consistent economic growth and a firm labor market, the bar to hike remains high, especially as oil prices abate.

All market and economic data as of 06/26/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank