Middle East tensions challenge renewed investor confidence

J.P. Morgan Wealth Management

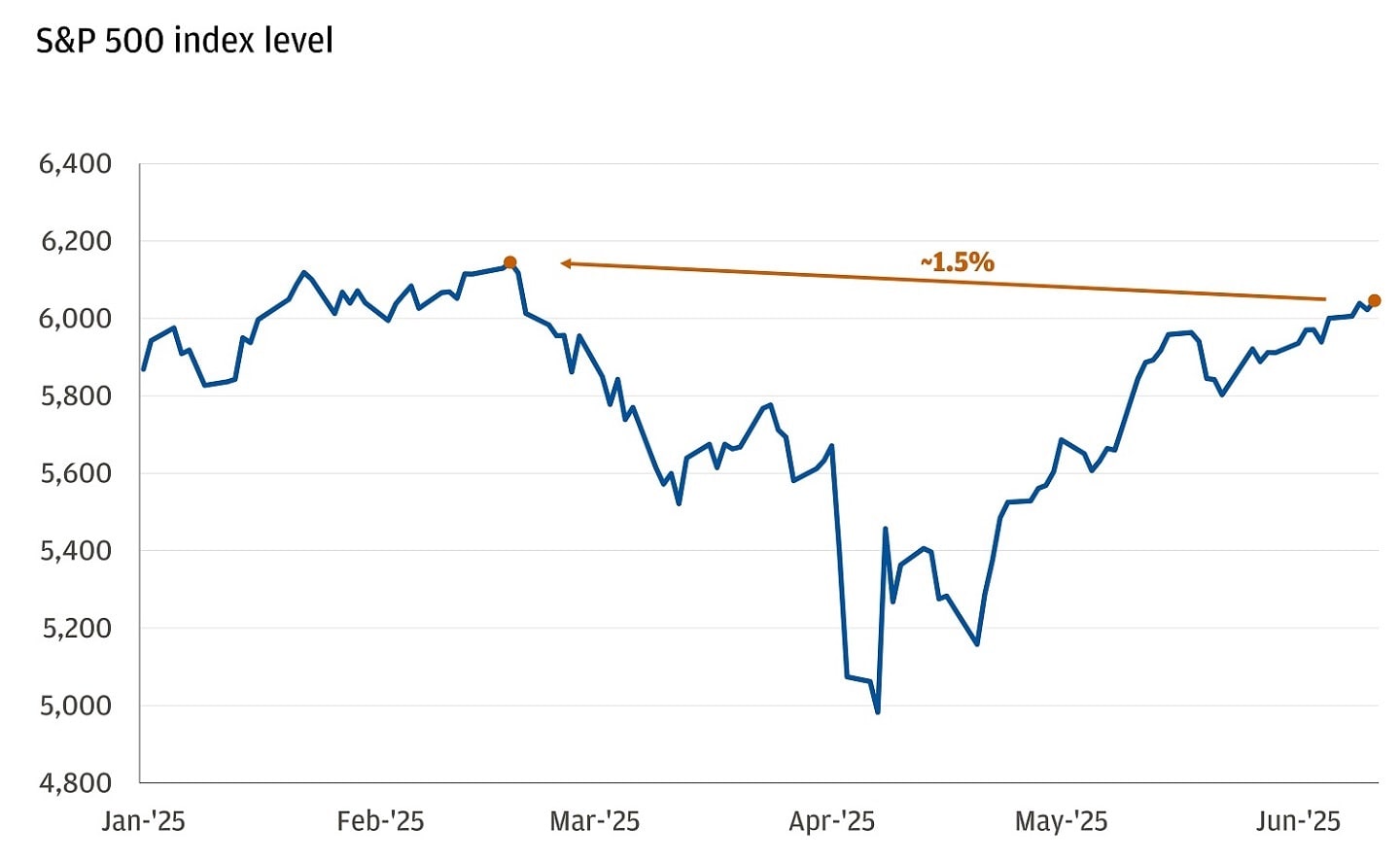

By Thursday’s close, most financial markets had fully rebounded from their April slump – an index of global stocks reached a record high, climbing over 20% from its lows. Likewise, the S&P 500 closed just 1.5% shy of its own all-time high.

But just as markets were getting comfortable with being uncomfortable, as we anticipated in our Mid-Year Outlook, a new geopolitical risk has emerged. Intensification of Middle East tensions now has investors on edge, with Israel launching attacks on Iran’s nuclear and military facilities, while Iran vowed retaliation.

The S&P 500 is about 1.5% away from all-time highs

As of 9:30 AM in New York, Brent oil prices are up over 7%, after earlier surging as much as 13% in the biggest intraday jump since March 2022, amid growing fears of a broader conflict. This has cascaded across other global markets, albeit less dramatically. European equities are down over 1% and U.S. equities declined 0.7%. Safe-haven assets like gold (+1.8%) and government bonds have rallied, while the dollar has reversed some of its recent declines after hitting a three-year low yesterday.

Our view, supported by history, is that geopolitical events typically have a limited impact on broad markets, but this is a risk worthy of attention. Below, we assess the threat that Middle East conflict poses to our view and offer our thoughts on why we believe the economy and markets should be able to withstand this geopolitical shock over the medium term.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

What we know so far

Israel launched a series of attacks on Iran, targeting nuclear and military facilities. While oil facilities haven’t been directly hit, Israel has vowed more action in the coming days, and Iran said that it will retaliate ”harshly.” The U.S. was quick to distance itself, noting no involvement in the attacks.

What we’re watching

The nature of the response from here will be telling. The conflict could escalate into one with a larger economic footprint.

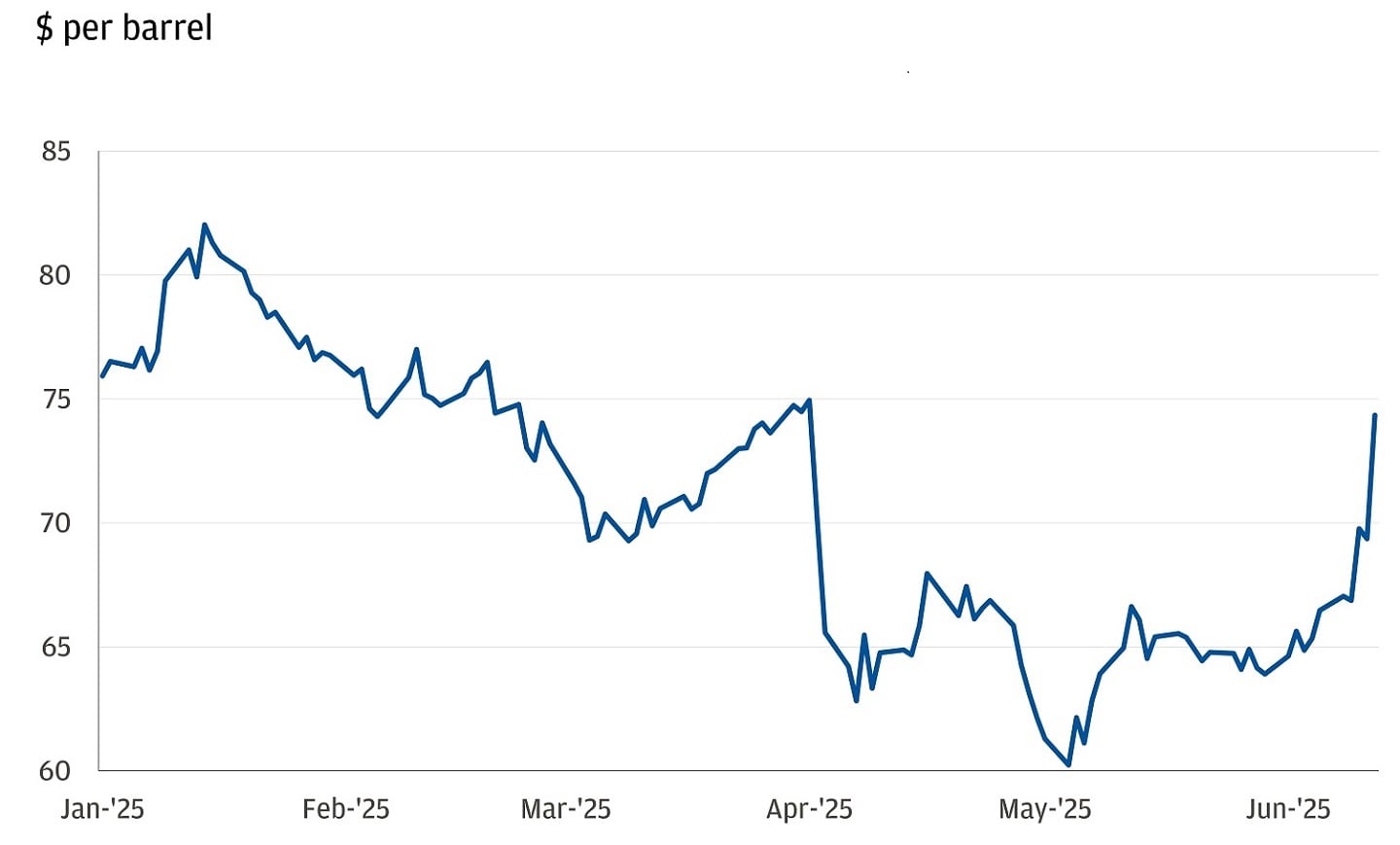

Iran is a smaller yet significant oil supplier, contributing about 4% to global production. The real risk, however, lies in conflict spillover to the broader region or key transit routes like the Strait of Hormuz, the critical choke point through which around 20% of global crude oil passes. The Middle East accounts for roughly a third of global oil production and regional players taking sides could complicate the energy supply picture. In turn, higher energy prices could disrupt sentiment, spending and investment, complicating the task of central bankers. Yet, it’s worth noting the bigger picture shows easing inflation – for instance, even with the recent spike, oil prices remain 10% below January’s highs.

Oil price have shot up, but still below January high

If we do see a significant disruption, the energy supply chain appears to have more capacity to absorb the shock than in decades past. For instance, such events would likely prompt other oil producers to increase supply. OPEC+ has spare capacity and U.S. production has demonstrated flexibility, largely thanks to the boom in shale fracking.

Why we’re comfortable with our view

Here are three pieces of evidence from this week that suggest the economy and markets can power through geopolitical risk.

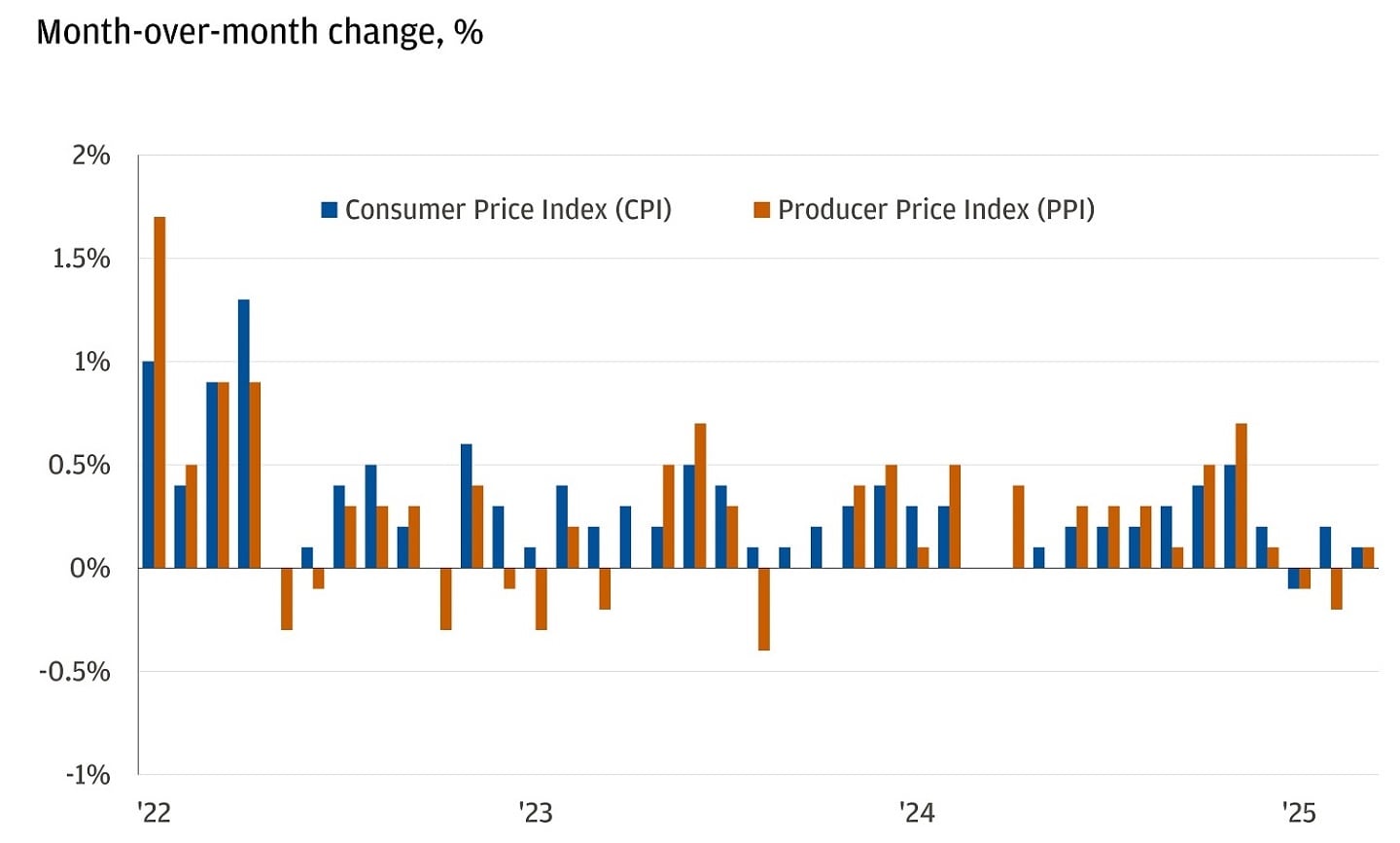

1. Inflation is trending down: This week, the Consumer Price Index and Producer Price Index (CPI and PPI) both decelerated to 0.1% month-over-month, despite expectations of 0.2%. If consumers were bearing the cost of tariffs, it would likely appear in the inflation data.

CPI and PPI are trending down

U.S. businesses, entering the year with elevated profit margins, might be absorbing the impact. They could also be postponing price increases by selling existing inventory ramped up ahead of tariffs, delaying the inflationary impact.

While it is still possible that some inflation will show up later in the summer, the fact we have not seen an impact so far is encouraging. It’s becoming increasingly evident that the economy is more resilient to higher tariff rates and general uncertainty than some anticipated and we maintain our belief that it can continue to expand.

2. Tariff talk is focused on cutting deals: Following U.S.-China talks in London, President Donald Trump announced a completed trade framework with China. Key aspects of the agreement include China’s pledge to expedite shipments of rare earths crucial for U.S. auto and defense industries and Washington’s easing of Chinese student visas and some export controls. Restrictions on advanced chips persist.

Tariff talk this week wasn’t all positive. A federal court ruled the administration could continue to enforce global tariffs while the appeal process proceeds, and Trump also warned that reciprocal tariff letters would be sent to countries within the next one to two weeks. Trade uncertainty is likely to persist, but the tone of trade talks has been focused on cutting deals.

3. The bond market has stopped selling off: After rising 35 basis points over the past two months, 30-year Treasury yields have fallen by 12 basis points this week heading into Friday. Thursday’s closely watched 30-year Treasury auction attracted strong demand, suggesting that investors in long-term U.S. government debt are becoming more comfortable with the 'One Big Beautiful Bill' moving through Congress. With bond yields down and stocks up, the recent decline in the dollar is much less worrisome than when investors feared capital flight from the U.S.

Building resilient portfolios

Markets will continue to be tested, with uncertainty likely to carry through the summer and beyond.

In our analysis of geopolitical events over time, history shows that while these events don’t have lasting effects on globally diversified equities, they can significantly impact local markets. In the U.S., the labor market remains relatively steady and inflation is still working its way towards the Federal Reserve’s 2% target. All signs point to a resilient economy that wants to keep expanding despite geopolitical risk. We advocate for normal levels of risk in multi-asset portfolios and continue to see opportunity in specific sectors like financials and software. Meanwhile, recent events underscore the importance of building resilience in portfolios through diversification, particularly with uncorrelated assets like gold and infrastructure.

Reach out to your J.P. Morgan advisor to discuss how resilient your portfolio is to geopolitical risk.

All market and economic data as of 06/13/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

J.P. Morgan Wealth Management