Is the momentum trade over?

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

By: Kriti Gupta and Nick Roberts

It’s a simple trade. Buy what has been winning, sell what’s been losing, and assume the trend continues. That’s momentum – something that has become one of the most implemented factors in portfolios. The classic academic version is a long/short portfolio: go long on the strongest performers over the prior three to 12 months and short the underperformers. In addition to strong earnings, it’s the force driving the stock market rally to new highs even in the face of geopolitical volatility. Will it last?

A tale as old as time

Over time, what makes up a basket of momentum stocks changes. It can be a variety of stocks, sectors or themes. In the late 1960s and early 1970s, it was a group of U.S. blue-chip stocks that investors deemed high-quality, growth companies that were posting durable earnings. Many of these companies were household names at the time, representing scale and consistent earnings growth – not to mention a way to capitalize on the economic boom in 1960s America.

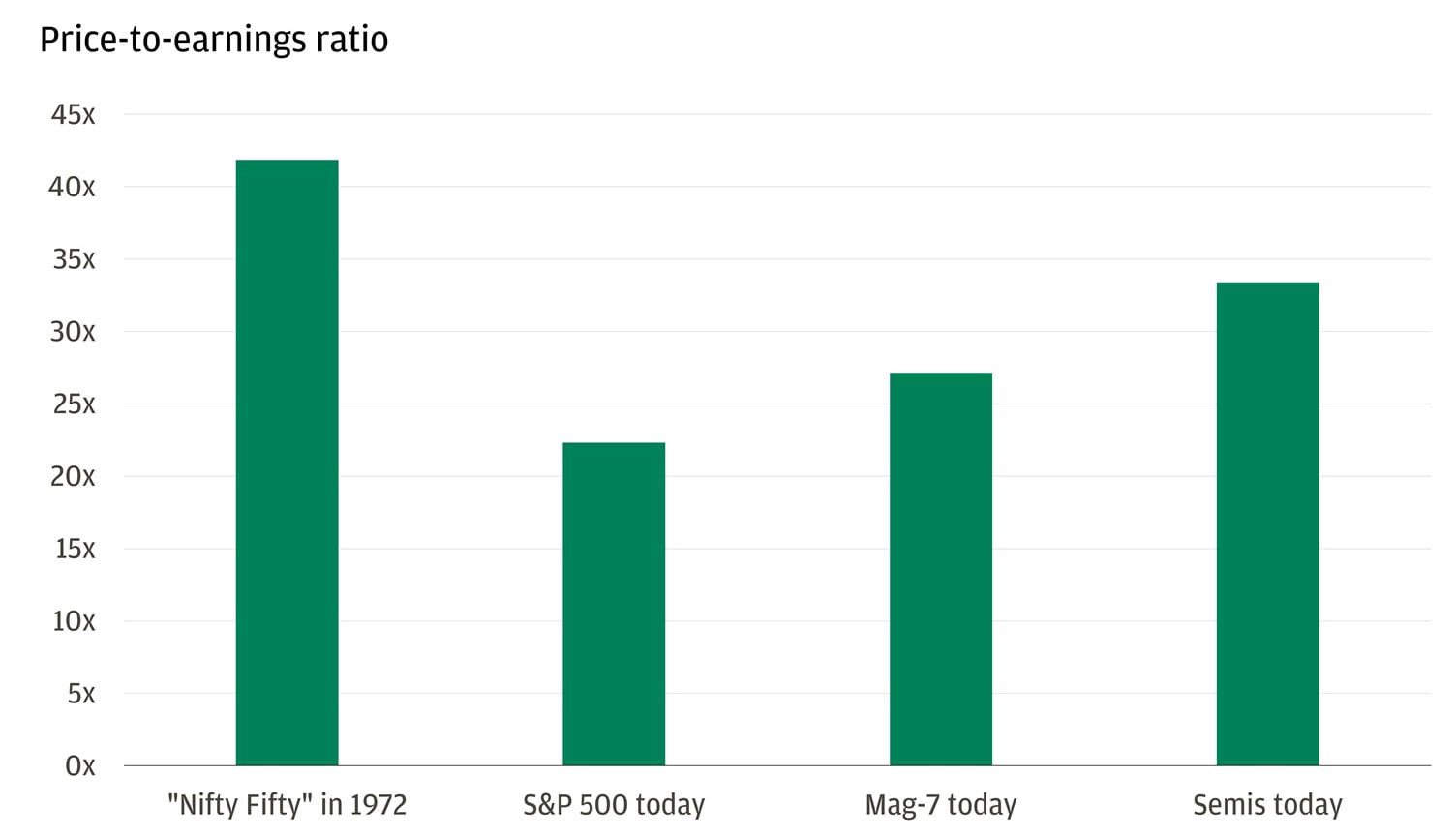

As they became more popular, they dominated investor flows – an early example of both concentration risk and momentum. The group started posting significant returns at valuations nearly double that of what the S&P 500 is trading at today on a price-to-earnings basis.

Valuations were nearly double in past momentum trades

Past performance is not a guarantee of future results. It is not possible to invest directly in an index.

Today, the momentum trade is all about artificial intelligence (AI). Investors are not just buying adopters of the technology but also leaning into scarcity around its buildout. That includes graphics processing units (GPUs), memory, networking equipment, power generation, grid infrastructure, cooling, transformers, copper, gas turbines and data center capacity. That trade came at the expense of enterprise software and commercial services – in other words, the sectors the market had decided AI would disrupt.

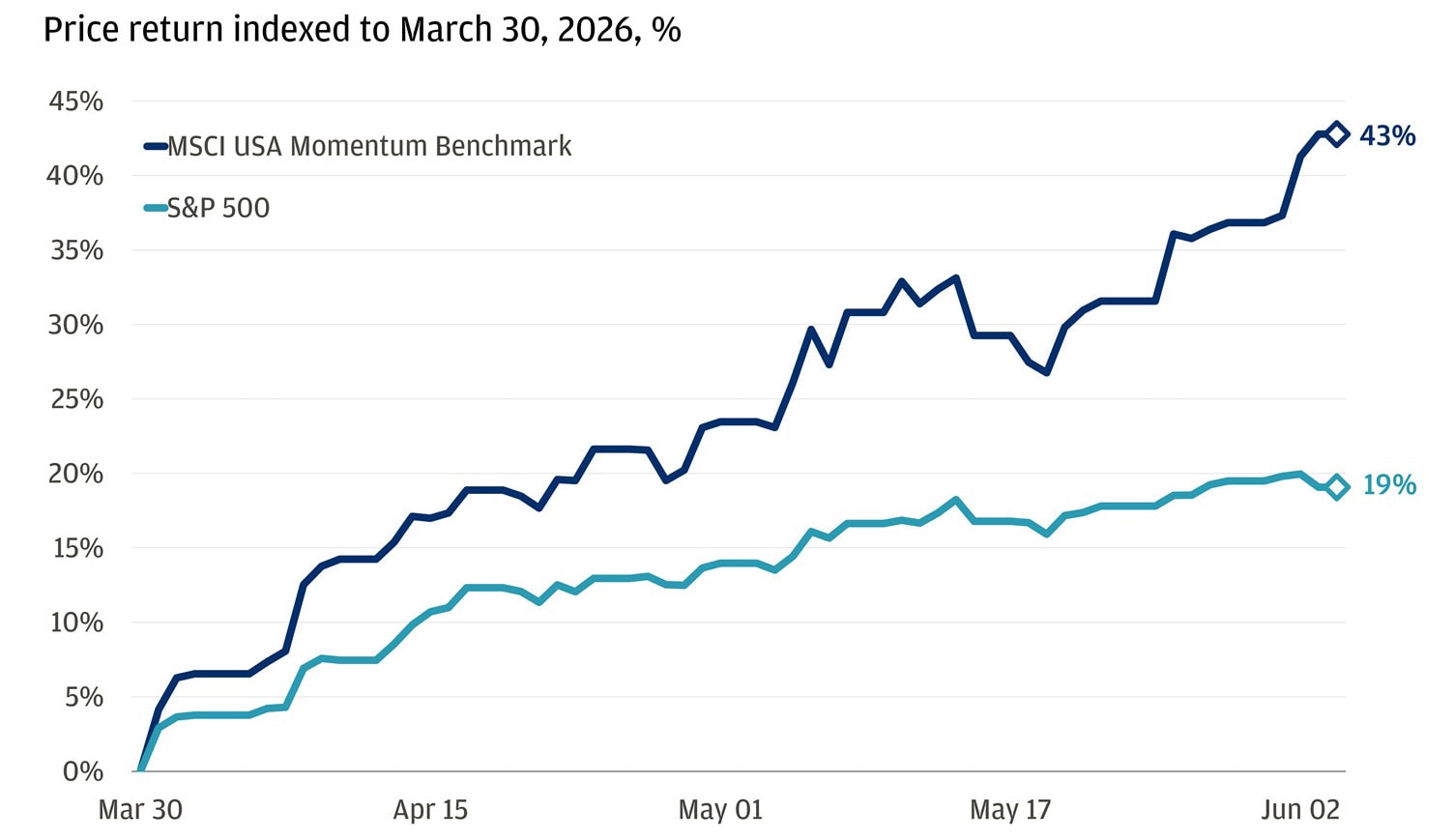

The outperformance from this winning cohort year to date has been historic. Momentum’s internal dispersion, which measures the gap between the outperformers and underperformers, is at its widest since 1990. While a basket of non-AI-related U.S. large-cap stocks has advanced 3.5% this year, a basket linked to AI data centers has returned 47%. The MSCI USA Momentum benchmark has gained 43% since the S&P 500 market low on March 30, marking a rebound more than double that of the index.

Momentum is driving performance as a factor and strategy

Past performance is not a guarantee of future results. It is not possible to invest directly in an index.

These gains are historic. Does that mean the rally is nearing its end? Not necessarily. Momentum-driven rallies can have legs. Historically, the one-year forward returns following a 100-day stretch with at least 20 all-time highs are no different from returns on any given day – suggesting this kind of momentum is not a warning sign. The pitfall arrives at inflection points, where drawdowns can be acute and sizeable, but it can also take years to get there.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

A moment for diversification

This isn’t an “abandon momentum” moment. The AI bottleneck is real, and the beneficiaries of the technological race still have fundamental support. But the trade has evolved, and for investors cautious of concentration risk, diversification remains a healthy portfolio construction philosophy. This is especially true now, as changes in geopolitics and macroeconomics have the potential to spur a rotation into unloved sectors.

Quiet summer trading activity could catalyze that rotation. Fewer people are trading, volatility often falls and the stock market can seem calm on the surface. But what may seem tranquil on the index level can mask changes in market leadership, at least temporarily. There may not be an outright drawdown or conflict-related market move, but a rotation in leadership in the short term can offer an opening for sector laggards like software, small caps, banks and other cyclical sectors to catch.

Another potential catalyst could be a true reopening of the Strait of Hormuz, or any de-escalation in the Middle East. That would in theory compress the risk premium built into oil prices, ease inflation fears and support consumer-facing sectors like airlines, transports, industrials and other cyclical exposure.

On an index level, it would prompt equity gains that go beyond just the tech sector and broaden out to other parts of the market. And that can be a healthy sign.

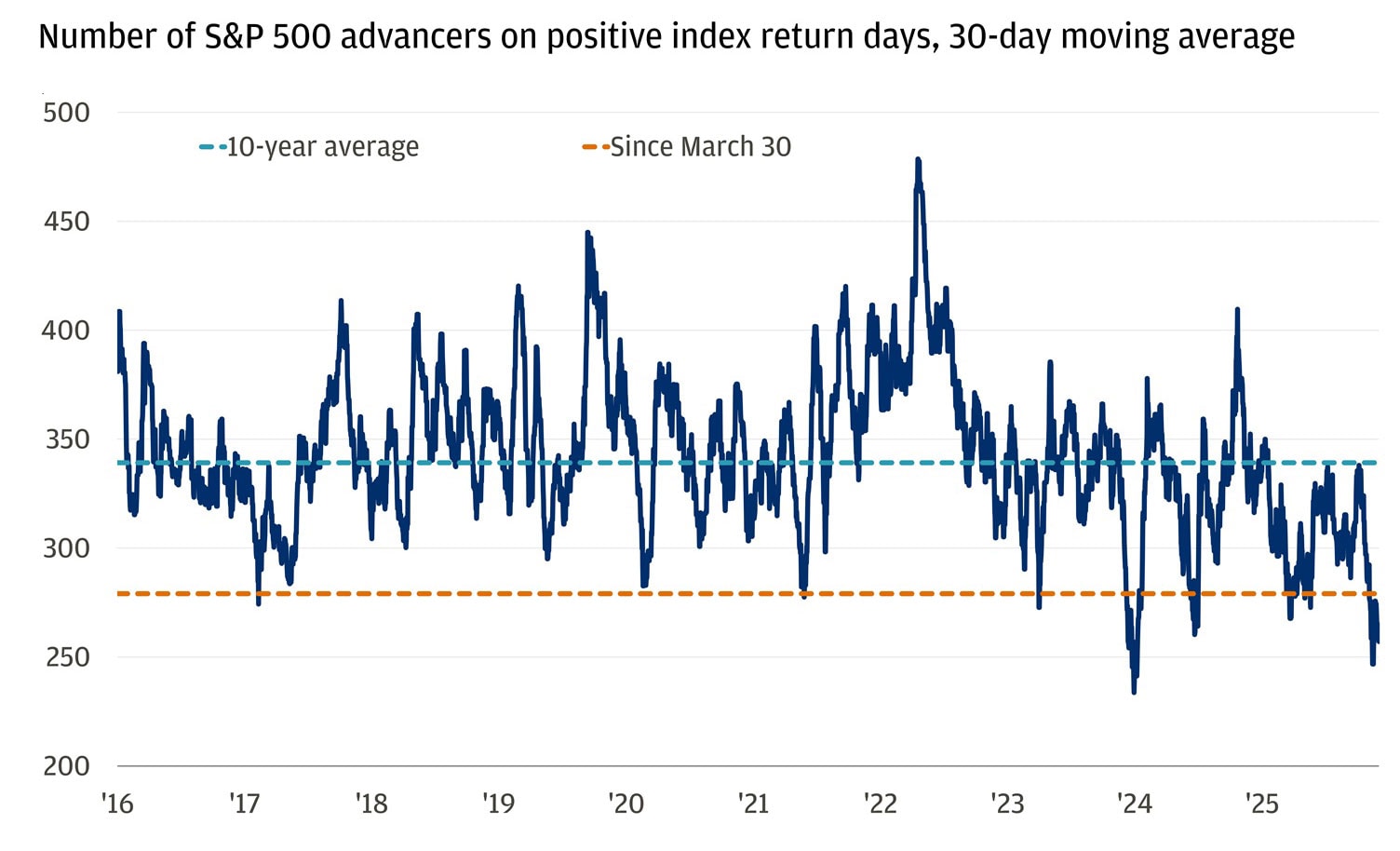

Breadth declined materially in the past two months

While momentum has delivered historic gains, the rally’s evolution and shifting market dynamics highlight the importance of diversification – giving investors a chance to benefit from new sector leadership as opportunities broaden beyond AI.

All market and economic data as of 06/05/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank