$1.5 trillion goods trade is on the line in USMCA's first test

By: Nur Cristiani and Mary Sangurima

Annual goods trade of $1.5 trillion – roughly 5% of U.S. gross domestic product (GDP) – is dependent on the United States-Mexico-Canada Agreement (USMCA), the trade agreement that governs economic relations across North America. On July 1, the agreement enters its first formal review, kicking off what could become a multiyear negotiation over the rules governing North American supply chains. This review is poised to help shape the way companies in manufacturing, industrials, infrastructure and logistics choose to build, source and invest.

There are three key questions likely to be top of mind for investors:

Will the USMCA remain a trilateral agreement?

The first question is whether the review could eventually lead to a breakdown of the trilateral framework. While that risk cannot be dismissed, the economic and political hurdles remain high.

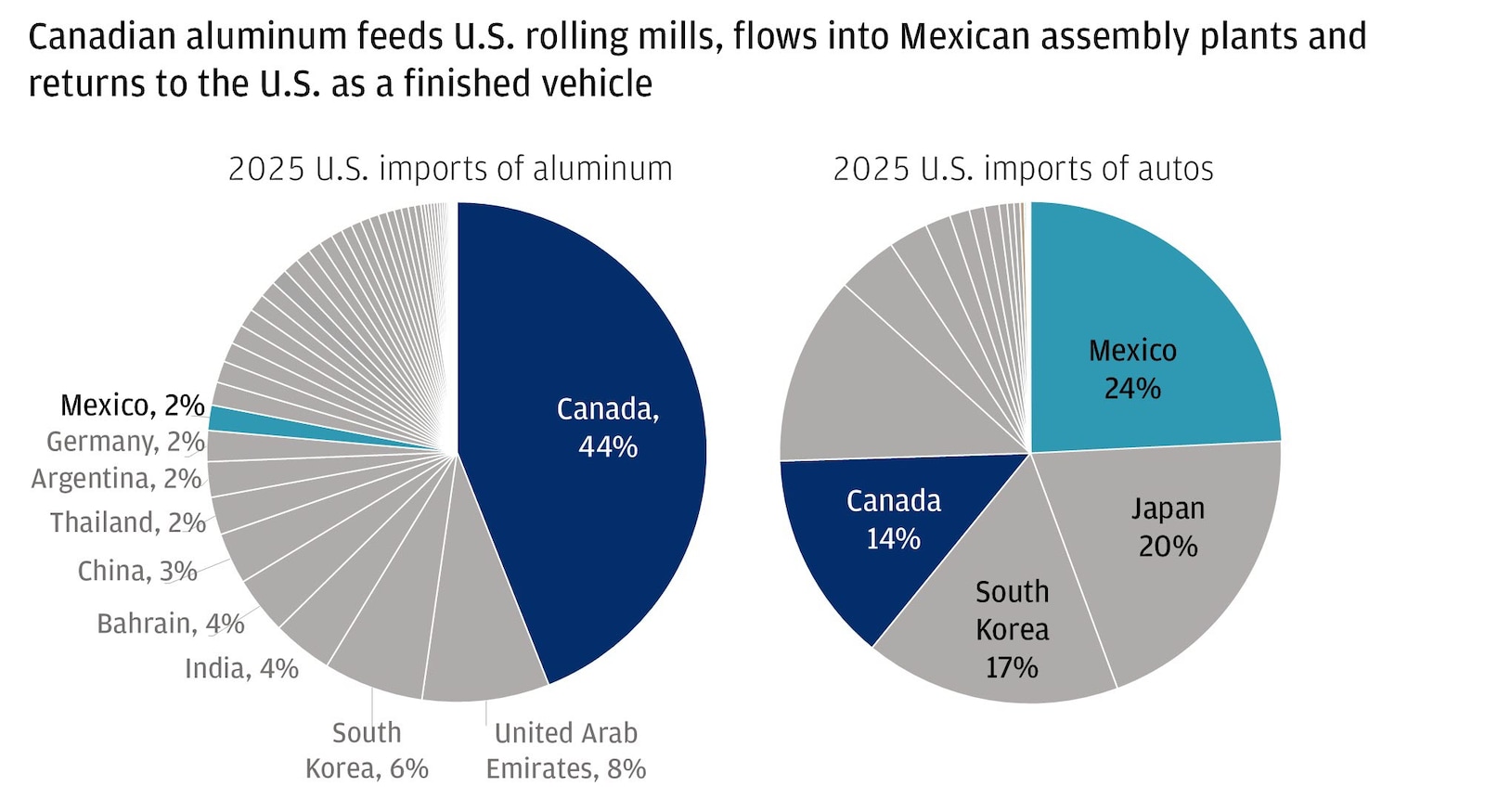

North American supply chains have become deeply integrated over the past three decades. Aluminum can move from Canada into U.S. processing facilities, auto components can flow into Mexican assembly plants and a single vehicle can cross borders multiple times before reaching consumers. Replacing the USMCA with separate bilateral agreements would require new negotiations, new legislation and years of implementation across all three countries.

North American supply chains are deeply integrated, and autos are the clearest example

The strategic costs could be even greater. A trilateral framework gives Washington leverage over broader regional priorities, including nearshoring, supply chain resilience, and Mexico’s trade relationship with China. A shift toward bilateral agreements could weaken that leverage while creating uncertainty for businesses that have spent years building supply chains around a single set of rules.

We believe the risk of outright termination is lower than it appears: if no agreement is reached this year, the USMCA does not lapse but shifts to annual reviews for the remainder of its 16 year term, continuing through its scheduled expiry in 2036, making the more likely outcome not a collapse, but continued negotiation within the existing framework.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

What is likely to be renegotiated?

At the center of the review is a debate over whether the USMCA is adequately preventing transshipment, or what some policymakers describe as a “backdoor” for China-linked imports entering the U.S. market. That debate is likely to shape discussions around autos, technology supply chains and energy.

Autos sit at the center of that discussion. While the USMCA increased regional content requirements from NAFTA levels, policymakers remain concerned that a meaningful share of components continues to originate outside North America. As a result, the review could bring tighter content rules, stricter verification requirements and greater scrutiny of how regional value is calculated.

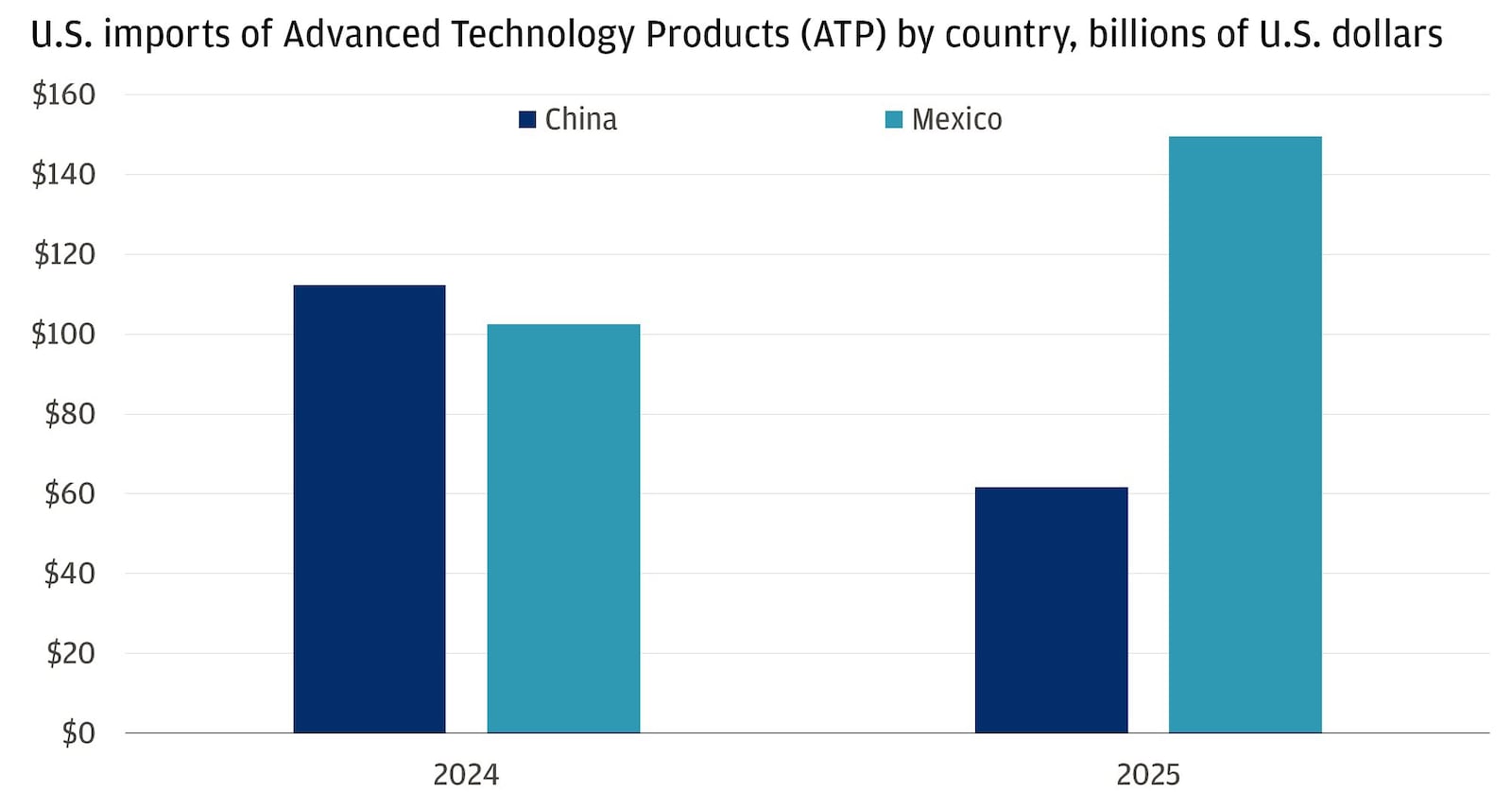

Technology supply chains are likely to face similar pressure. Mexico recently surpassed China as the leading exporter of Advanced Technology Products (ATP) to the United States. ATP is a U.S. government trade category that includes products such as semiconductors, computers, electronics, aerospace equipment and telecommunications hardware. While much of that growth reflects legitimate nearshoring activity, policymakers are increasingly focused on distinguishing North American manufacturing from simple assembly of imported components.

Mexico overtook China in advanced technology exports to the United States in 2025

Energy remains another potential pressure point. Ongoing disputes involving Mexico’s treatment of state-owned and private energy producers have raised broader questions about investment protections, market access and dispute settlement under the agreement.

Investment predictability is another area to watch. Mexico’s 2024 judicial reforms raised concerns among U.S. and Canadian businesses about the independence of courts and the enforcement of contracts and investment protections. For companies making long-term investments in factories, energy projects and infrastructure, legal certainty can matter as much as tariff rates.

Taken together, these debates suggest the review will focus less on expanding trade and more on tightening the rules around what qualifies for preferential treatment under the USMCA.

How will security shape the talks?

Trade may be the formal subject of the review, but security is becoming an increasingly important part of the conversation. The reason is simple: Nearshoring depends on more than trade rules. It also depends on whether companies feel confident investing across North America.

In recent years, Washington has placed greater emphasis on border security, migration, illicit trafficking and cartel activity in its relationship with Mexico. While these issues sit outside the USMCA itself, they increasingly shape the broader political environment in which trade negotiations take place.

As a result, the review is likely to extend beyond trade flows alone. The broader discussion may increasingly focus on the conditions needed to support investment, nearshoring and long-term economic integration across North America.

What comes next for North American integration

Our base case remains that the USMCA survives in its trilateral form. The review is more likely to result in tighter content requirements, greater scrutiny of China-linked imports, expanded labor enforcement, and continued debate around energy and investment protections than a fundamental rewrite of North American trade. But beyond July 1, the broader trade relationship is likely to continue being used as leverage on nontrade issues, adding a persistent layer of uncertainty to investment decisions across all three countries.

For investors, the implications extend beyond trade policy. North America has become an increasingly important destination for manufacturing, industrials and infrastructure investment as companies seek to diversify supply chains and reduce dependence on China. The review is unlikely to reverse those trends, but it may influence where capital is deployed and which companies are best positioned to benefit from the next phase of North American integration.

All market and economic data as of 06/18/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.