Debunking the “Sell America” trade: Why Europe’s move could fall short

By Kriti Gupta

Tensions ran high after the White House’s most recent threat of higher tariffs on European trading partners, sparking fears of potential retaliation and shaking global investors’ faith in American assets. This isn’t Liberation Day 2.0, but it is emblematic of how markets – and policymakers – are working to digest and react to a splintering global order. Although the conflict has since simmered, it’s worth noting that the two largest tools at Europe’s disposal to fight back may not be deployable at all. And therein lies the flaw in the “Sell-America” trade.

What is the 'Sell-America' trade?

After the Trump administration first announced tariffs on the United States’ trading partners in April 2025, the S&P 500 dropped 12%, the dollar weakened 6% and long-end yields rose over 40 basis points. And so was born the “Sell-America” trade: When global investors flee American assets and the stock market, bond market and dollar all sell off at once. Having them all move in the same direction at once is rare.

Recent market volatility rhymed with the fallout of Liberation Day and resurrected a familiar pattern. But as we saw at the end of the week, the panic was short-lived. In comparison to Liberation Day, these recent market moves at peak volatility were only 15%–20% of the post-tariff announcement reaction.

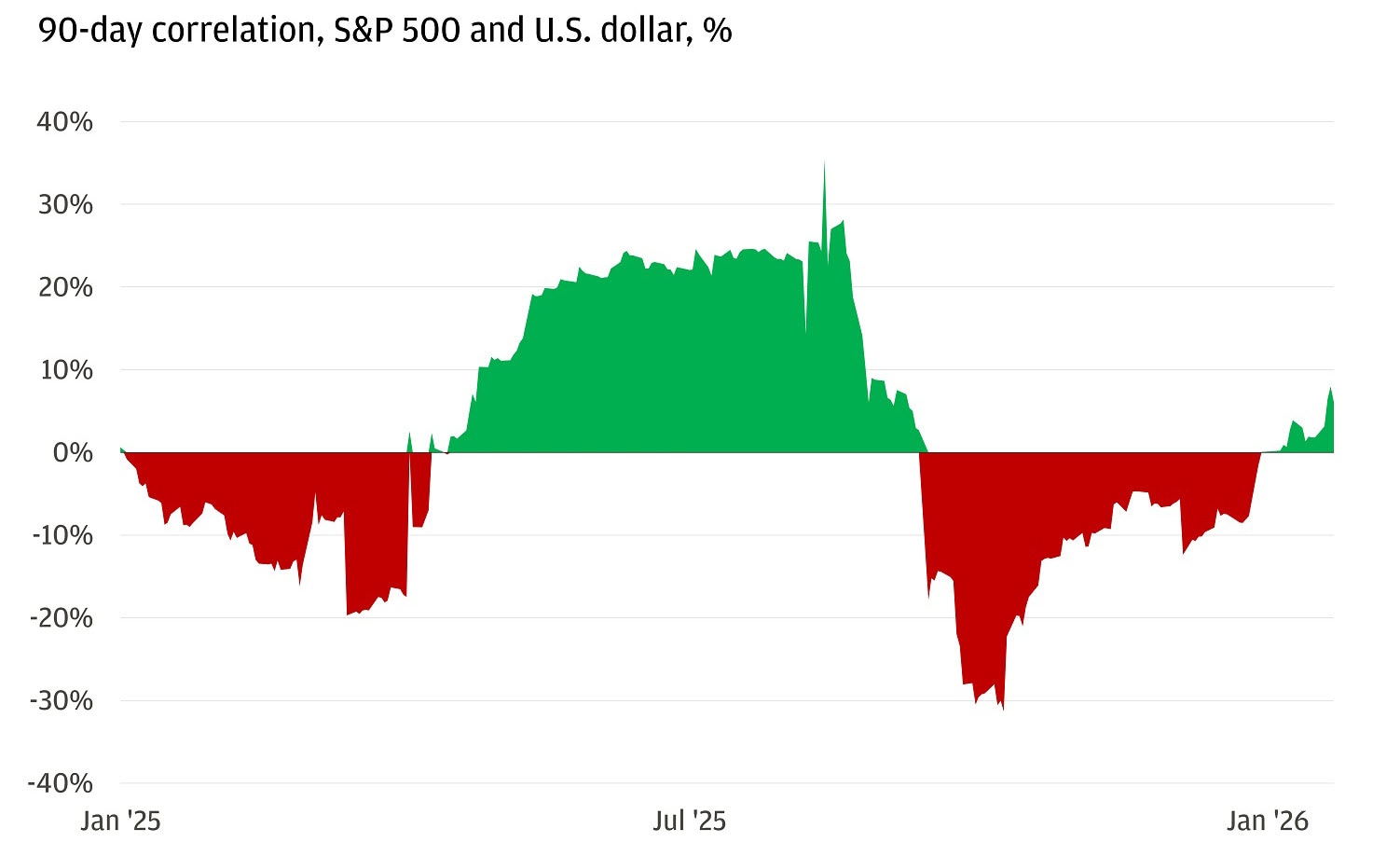

To see if “Sell-America” sticks, watch the 90-day correlation between the dollar and the S&P 500. If it’s positive, it means that investors are trading U.S. assets as one, the clearest indication that jitters remain and could reemerge.

Positive correlation for the first time since September

Tuesday’s sell-off showed that investors are still skittish about the trade war. But it’s more than just the tariffs. It’s the potential for escalation. Rest assured, the tools Europe has to retaliate are highly unlikely to be deployed, which limits the potential damage that trade war saber-rattling can have on markets.

Europe’s trade bazooka: The weapon that can’t be used

Three months after Liberation Day, the United States and EU had agreed to a tariff rate of 15%, half of the amount Washington initially suggested. While some decried the EU for capitulating, the markets rallied. And corporations rejoiced – not at the rate, but at the certainty. But the worries center around more than just tariffs on physical goods. There’s a bazooka in our midst, and it’s aimed at services.

There is a growing chorus in Europe advocating for the use of Europe’s “Anti-Coercion Instrument” (ACI), more commonly known as its “trade bazooka.” Initially created to address trade with China, it’s a mechanism that enables restrictions on the physical imports and exports of goods across EU borders. But more alarmingly, it could escalate the trade war to services (an arena in which the United States holds a trade surplus with Europe). It could effectively cut off American financial services and technology from the EU’s 450 million customers. Untested and risky, it’s previously been thought of as unthinkable to use. Most recently, it resurfaced as a plausible tool in the arsenal.

Since the global trade war has largely focused on goods and manufacturing, services have mostly remained untouched. European restrictions on U.S. services would be extremely damaging for the United States, but here’s the twist: It could do more damage to Europe itself. The disruption to financial markets and the real economy could be cataclysmic, given the EU imports about 483 billion euros in services from the U.S., including scientific and technical services, telecommunications, technology and intellectual property, according to 2024 data. A disruption of this scale in the world’s largest bilateral trade and investment relationship is simply too large a recoil. Not to mention, it can take up to a year to implement.

Even a marginal increase in the likelihood of its use can rattle investors. But while it adds to near-term fears, the trade bazooka is unlikely to be unleashed.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

The Treasury’s nightmare: A European fire sale of American bonds

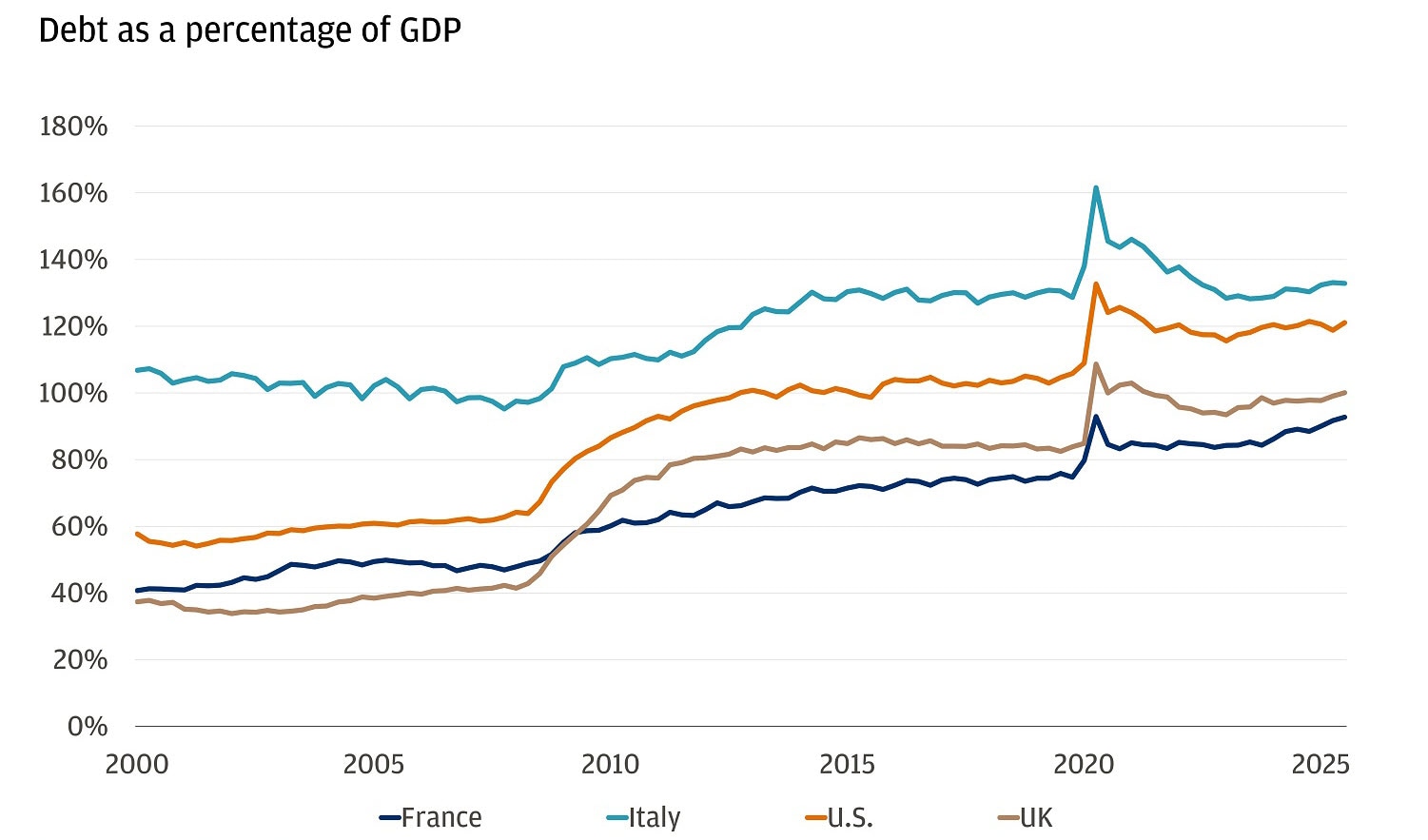

The other leverage that Europe has is a fire sale of American bonds, a longstanding fear and one of the United States’ largest economic vulnerabilities. The EU collectively holds about $8 trillion of Treasuries, roughly 24% of the $34 trillion market. The bloc is the largest financier of American borrowing, so selling the assets would flood the market and create a surge in U.S. bond yields. Mission accomplished?

Probably not. The cost would, again, be too great. For the rest of the world, yield curves would steepen, global borrowing rates would surge and sovereign debt burdens would be that much harder to pay down and refinance. It would be a nightmare for countries like France, which boasts the largest sovereign bond market in Europe by debt outstanding and has a growing deficit, with no end (or budget) in sight.

Rising debt loads add to rate sensitivity

It’s a move that would need to be done at scale to do damage, but would ultimately hurt both sides of the Atlantic even if solely aimed at Washington. That’s why when Danish pension operator AkademikerPension said it would sell $100 million of its Treasury holdings, the market didn’t blink. It’s an amount that can be easily absorbed and carries more symbolism than impact.

The bottom line: Don’t sell America

There will inevitably be more strain in the transatlantic alliance. The conversation around tariffs is far from over. As soon as next month, 93 billion euros worth of European retaliatory tariffs are due to come back into effect after being frozen since last summer. It remains noise.

The worst-case threats are unlikely to materialize. The U.S. and EU are simply too interdependent and breaking that relationship would come at too great a cost for both parties. This sobering fact limits the scope of any retaliatory measures and offers some powerful reassurance.

In an era of global fragmentation, European efforts to rebuild defense and infrastructure capabilities could benefit industrial stocks in the region. And the U.S., despite policy uncertainty, remains a high-conviction investment opportunity. It boasts a healthy consumer, maneuverability in monetary policy, energy independence, dominance in capital markets and the massive tailwind that is the artificial intelligence (AI) buildout. And that momentum isn’t going anywhere.

All market and economic data as of 01/23/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.