Fall in focus: 5 things investors should watch

Global Investment Strategist

How are markets reacting to the latest world news?

August slipped away like a bottle of wine (congrats, Taylor!).

Over the summer, the S&P 500 rose +9% and U.S. Treasury yields moved lower across the curve with 2-year and 30-year yields down about 25 basis points and 20 basis points, respectively.

Around the world, it was a similar story. In U.S. dollar terms, onshore China equities gained +17% since June and European equities added +4% (and are up +25% so far this year), helped by a softer dollar.

What’s driving the tape? Growth cooled but didn’t crack and tariff pass-through nudged inflation higher without derailing earnings. Corporate America did the heavy lifting and companies kept leaning into investment around artificial intelligence (AI). The Federal Reserve (Fed) is widely expected to cut rates at its next meeting in three weeks.

Sentiment improved given inflation pressures look manageable, profits are growing and policy looks set to ease. Risks remain – valuations are full, tariff-driven inflation could still come and investors fret about Fed independence – but for now, markets are looking through near-term noise and positioning for the forces that matter most over the long term.

Today’s note focuses on what’s ahead. Here are five things to watch heading into the final months of 2025.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Five market dynamics for investors to watch this fall

The Fed’s cutting cycle

At the Jackson Hole conference, Fed Chair Jerome Powell all but confirmed that the Fed is likely to lower rates at their meeting in September. Over the summer, hiring slowed and prices firmed: Payrolls averaged about 35,000 a month while headline inflation nudged up from roughly 2.4% to 2.7% year-over-year by July. Tariff pass-through showed up most clearly in goods – even as cheaper gasoline capped the headline print.

The Fed’s message has been consistent: If inflation expectations stay anchored, it won’t overreact to tariff-driven bumps and will keep a close eye on the labor market, where both demand and supply have cooled. At Jackson Hole, Powell essentially doubled down on that – “the balance of risks are shifting,” with downside risks to employment rising. So, the Fed won’t let one-off price moves drive policy.

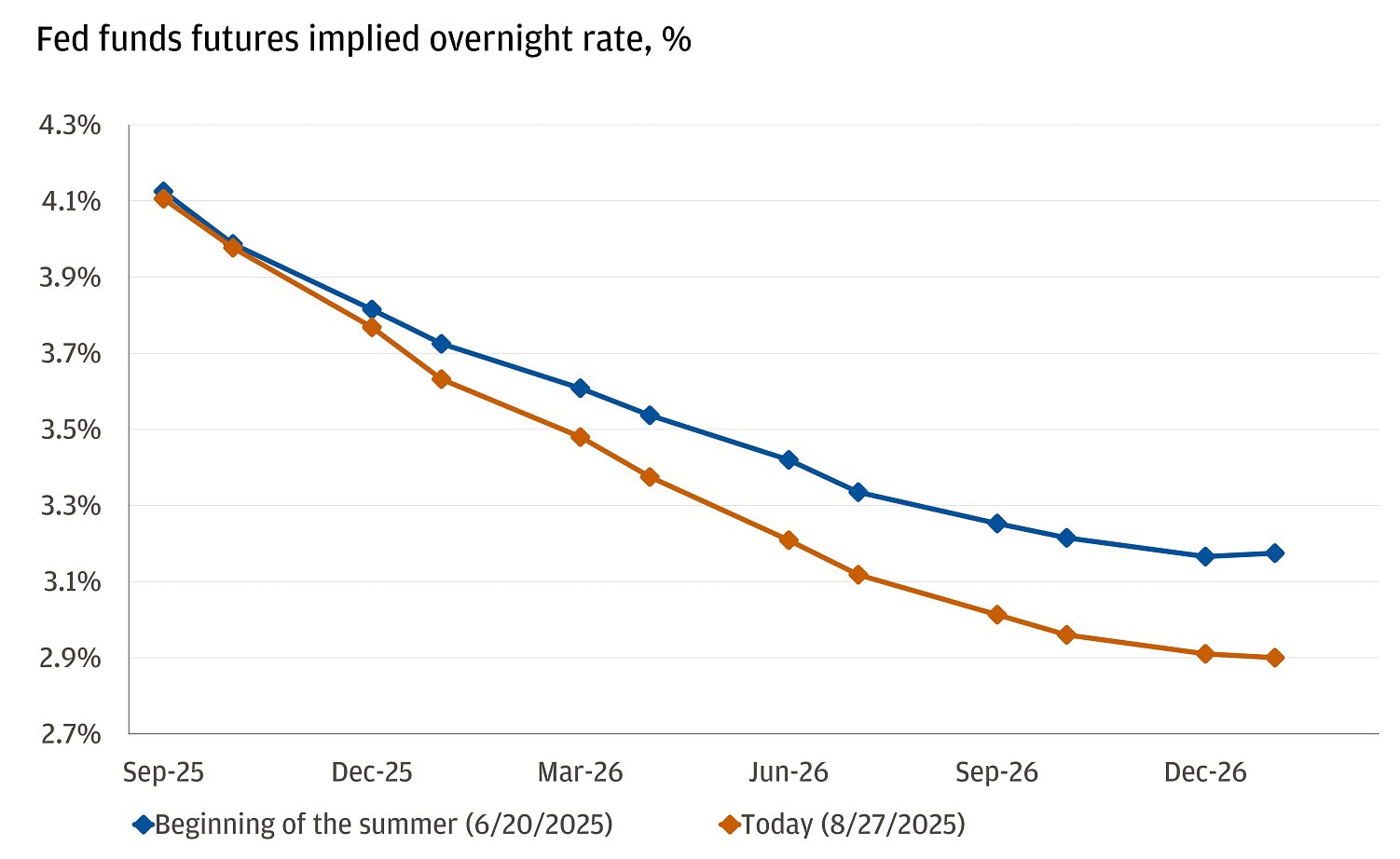

Markets largely agree on the near term: Odds of a September cut sit around 90%, and pricing implies nearly 50 basis points of easing by year-end. The only two things standing in the way of a September cut are the August jobs report (released on September 5) and August Consumer Price Index data (released on September 11). Unless there’s a significant surprise in either, cuts are likely coming. If expectations remain anchored and labor data soften further, we think the Fed cuts once more after September this year. Post-Jackson Hole, markets still see fed funds around 3.8% by year-end, 3.2% by mid-2026 and 3% by the end of 2026.

The Fed’s bias is towards easing, and markets agree

Bottom line: Slower growth plus firmer inflation prints have the Fed threading the needle. For now, the policy bias is toward easing, so long as expectations stay stable and the labor market cools rather than cracks.

Corporate profits

Two numbers tell the story here:

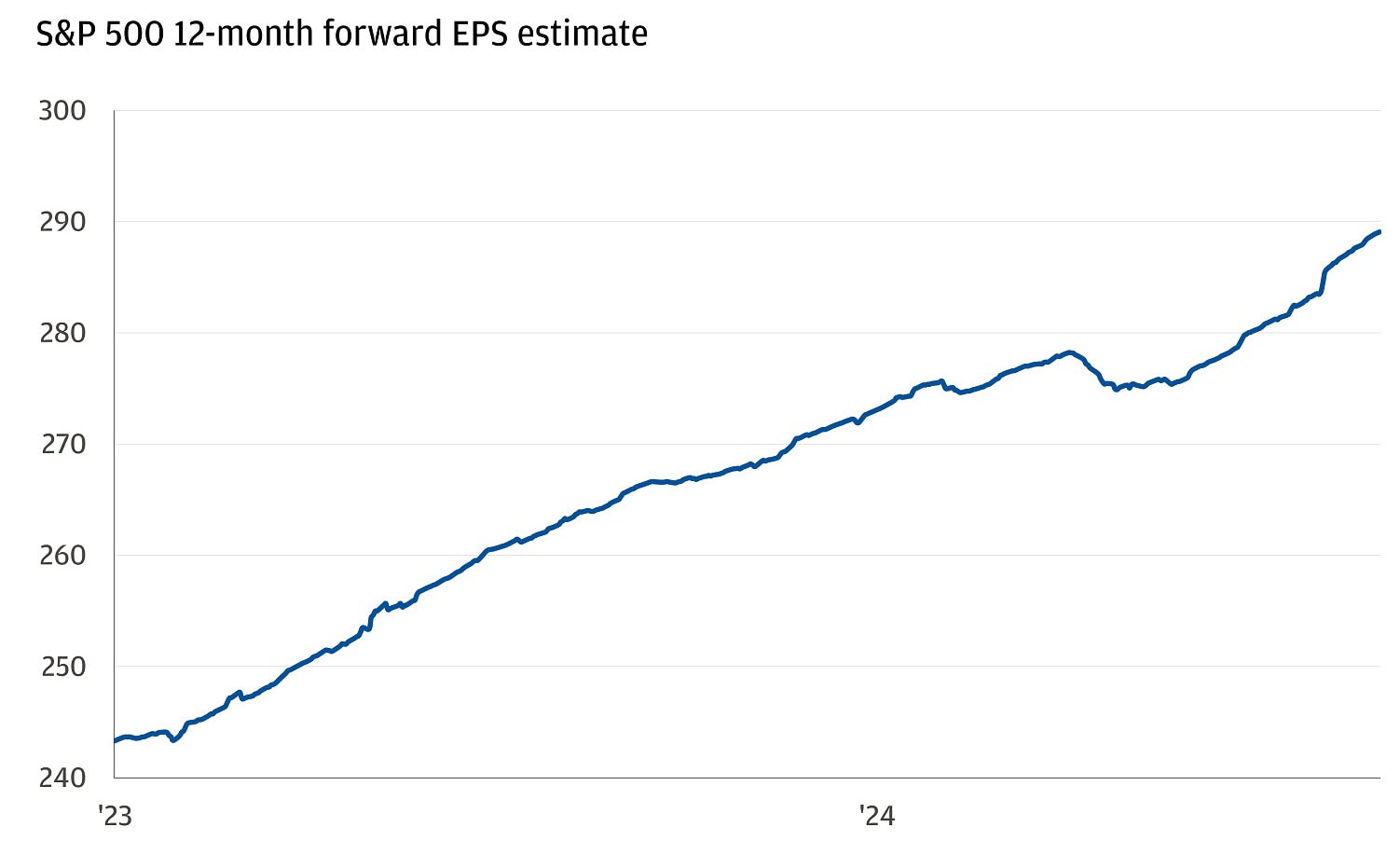

- As of June 30, investors expected Q2 S&P 500 earnings growth of 4.9%. With 95% of companies having reported, that number is running near 12% – with Nvidia’s beating the latest in a string of upside surprises.

- Net profit margins are at 12.8% for Q2 – up from 12.7% last quarter and 12.2% a year ago, and above the five-year average (roughly 11.8%). In other words, margins have continued to expand despite dramatically higher tariffs.

Earnings estimates continue to climb

What that says: C-suites delivered. Even with slower growth and tariff headlines, companies protected pricing, managed costs and kept profitability in place. We’ll be watching Q3 earnings closely – consensus assumes a dip, but that was the setup for Q2 as well.

A few tailwinds are likely to help into year-end – tariff policy is clearer than earlier in the year, trimming planning risk. Sectors like tech and utilities should benefit from ongoing AI investments and data-center capital expenditure (capex), plus support from that One Big Beautiful Bill – while a Fed cut (and a gentler path thereafter) would be a clear catalyst for rate-sensitive growth leaders.

AI capex super-cycle – still on; power is the bottleneck

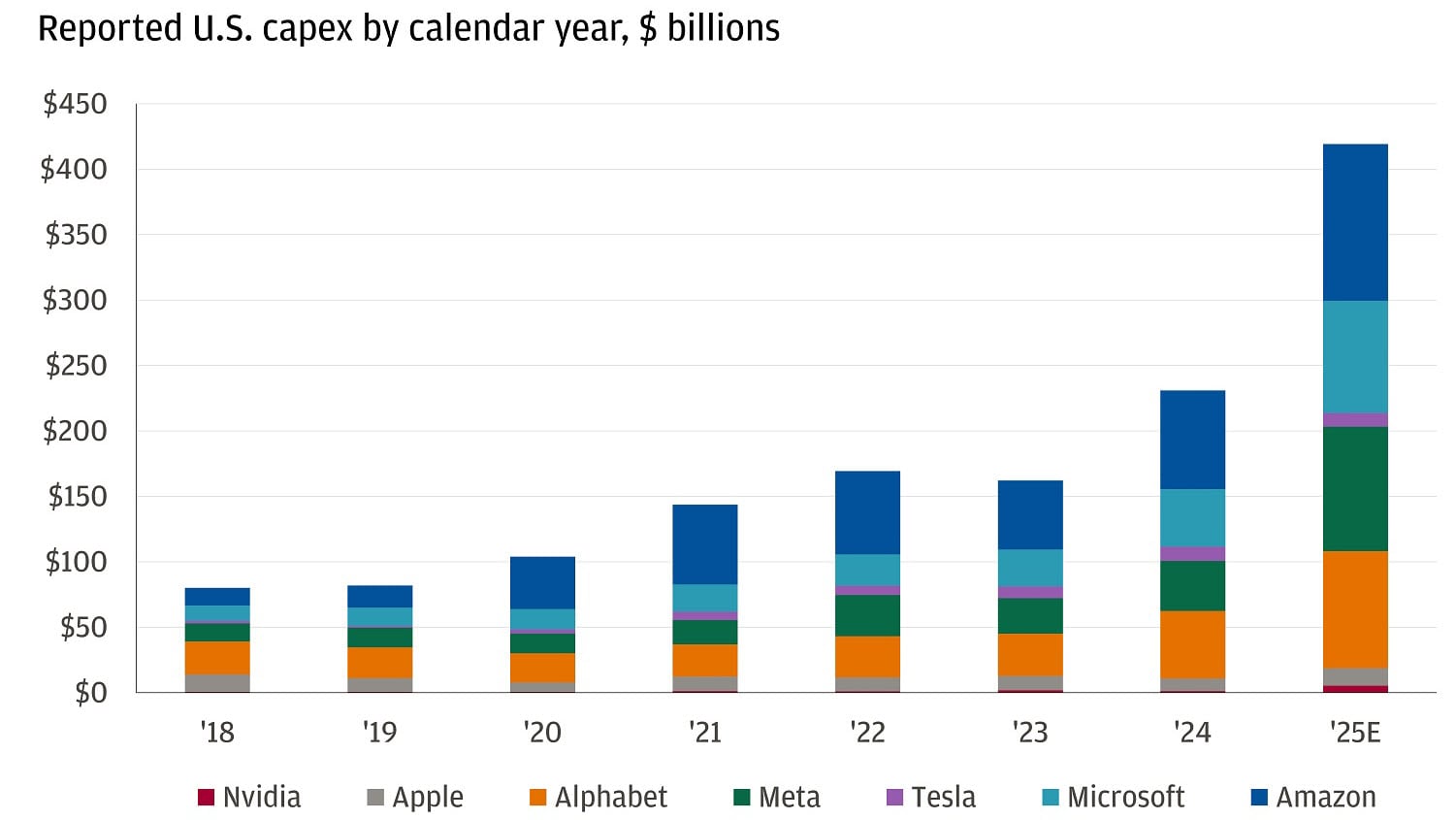

Even as some doubted whether hyperscalers would stick to their capex plans, they’ve raised spending expectations, keeping data-center buildouts and AI spend front and center.

Microsoft flagged a record $30 billion capex this quarter and has telegraphed $80 billion for fiscal year 2025. Alphabet lifted its 2025 capex plan to $85 billion, Meta raised 2025 capex to between $66 and $72 billion and Amazon indicated full-year spend around $118 billion at its current run rate. We estimate capex will increase about 80% year-over-year as AI builds accelerate.

Hyperscalers continue to boost capex plans

The limiting factor might be power supply. After nearly two decades of flat power demand, U.S. electricity use is expected to grow on a roughly 2.5% compound annual growth rate (CAGR) through 2030 – about 800 terawatt hours of additional load this decade – roughly Texas and California’s combined annual generation. Data centers are the single biggest driver – about one percentage point of that 2.5% CAGR, nearly half of total growth.

And the U.S. is the epicenter. “Data Center Alley” (Northern Virginia) anchors a footprint that’s now approximately 45% of global data-center power demand. U.S. data centers are roughly 4% of total electricity use today and are set to approach 9% by 2035. The pinch point is supply: Nine of 13 regional power markets are already in or near critical tightness for 2025; in five years, all but one are expected to sit below comfortable thresholds.

Bottom line: The capex super-cycle is intact, but power availability and interconnect timelines will pace it. We see opportunity in the picks-and-shovels: utilities with load growth, grid and power suppliers and AI enablers.

Europe: Stronger euro, new capex, defense momentum

Growth is modest and inflation has cooled, but the euro’s recent strength is a headwind for big exporters. As a rule of thumb, a 10% appreciation of the euro reduces earnings per share (EPS) by approximately 4% for Europe’s 50 largest companies. That foreign exchange (FX) bite shows up first in guidance from globally exposed sectors – hence we like the domestic story (as Europe addresses some of its longstanding issues, less FX drag).

On the other side of the ledger, public policy is crowding in private investment – from energy grids and clean tech to semis and manufacturing. Think of the “Made in Germany” push: targeted incentives and guarantees spurring capex and rebuilding capacity. Those programs are fueling new orders and backlog, giving industrials multi-year revenue visibility, even if near-term sales growth is modest. Many of these projects ramp up in 2026.

Defense remains a clear bright spot. With multi-year budgets firming, we expect a potential step-up in guidance from several defense primes in the future as production scales and backlog converts.

Bottom line: A firmer euro is a drag for exporters, but capex tailwinds and defense demand help balance the tape. Added plus: the 15% U.S. tariff on EU goods – well below earlier threats – brings much-needed clarity, which should lift business and consumer confidence and improve planning for 2025 and 2026.

China: Structural strains, tech upside taking shape

China’s economy has structural challenges, but the tech sector is a bright spot. July’s net new loans turned negative – the first monthly contraction in about 20 years – which means borrowers repaid more than banks lent, a clear sign of weak private-sector credit appetite amid ongoing property stress.

The rest of the economic dashboard points the same way. Inflation was 0% year-over-year, home prices fell again (the declines are milder, but the downtrend isn’t broken), youth unemployment climbed and industrial output slowed while manufacturing PMIs (Purchasing Managers Index) dipped below 50. The main driver: A negative wealth effect from the housing downturn and a softer labor market that’s keeping spending in check.

We’re a bit more optimistic on Chinese technology. Valuations remain attractive versus global peers, the regulatory backdrop has stabilized and the domestic AI stack keeps advancing – DeepSeek underscored that innovation can continue even with constraints. Tariff policies are more predictable, reducing planning risks for hardware and supply-chain companies. Select large platforms and infrastructure enablers with strong balance sheets and clear cloud/AI monetization strategies are well-positioned, while sustained outperformance will likely require a more durable recovery in economic fundamentals and earnings.

The bottom line

As fall rolls in, markets are juggling a Fed that’s leaning toward easing, profits that keep surprising, an AI capex wave running into power bottlenecks, Europe’s stronger euro offset by fresh capex and defense momentum and China’s macro chill alongside a tech thaw. In other words, plenty of moving parts, but also plenty of ways to play them. The coming season brings both challenges and catalysts – speak with your J.P. Morgan advisor to make sure your portfolio is ready for what’s on the horizon.

All market and economic data as of 08/28/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist