The defensive playbook isn’t your average inflation roadmap

Markets are pricing in a familiar fear: With volatile oil prices hinging on developments around the conflict in Iran and the uncertainty weighing on equity bulls, investors are instinctively falling back on the inflation playbook – buy energy and consumer staples.

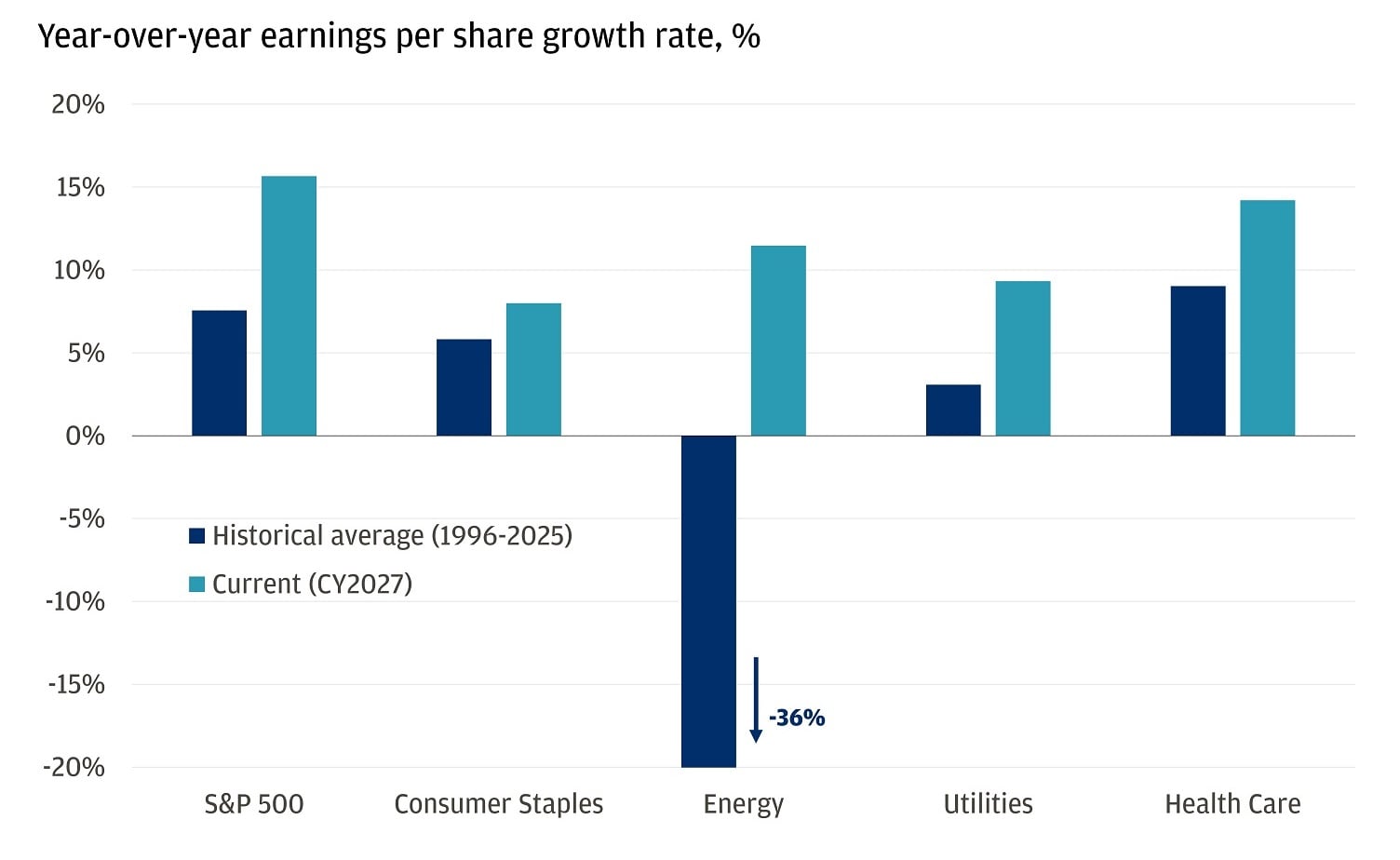

It’s a script investors know well as geopolitical risk rattles the markets. But this cycle looks different than previous iterations, especially if the conflict deescalates. Earnings growth expectations and limited exposure to energy price volatility point to a quieter, and more compelling, defensive trade: utilities and healthcare. With relatively low valuations, the sectors offer investors a more defensive posture for a stock market bottom.

The tried and tested path

It’s conventional wisdom: When oil prices rise, energy stocks rally. When growth fears mount, consumer staples companies provide shelter. They’re the things consumers need regardless of economic conditions – the basics. That framework is deeply ingrained, but perhaps becoming increasingly outdated.

For most of 2022, energy was the only positive sector in the S&P 500. But after the market bottomed, investors rotated out of energy and embraced every other sector. Fast forward to 2026 and the same familiar market reflex is kicking in. Worries around being late-cycle, facing sticky inflation and the potential for higher rates are driving a bid for energy stocks yet again. The sector has already seen a 36% rally in the first quarter of the year and an almost 10% rally just since the conflict in Iran began.

Whereas energy and consumer staples stocks benefit from the perceived risk of inflation, they are also directly exposed to the conflict in Iran through commodity prices or input costs, respectively. That distinction matters if tensions with Iran escalate or remain unresolved.

Why lean into energy shock exposure when you can be insulated instead?

There are other sectors that offer defensive characteristics with long-term growth prospects. Healthcare demand, by contrast, is largely insensitive to fuel prices altogether and remains mostly non‑cyclical. Innovation pipelines remain robust. And earnings growth is supported by demographics rather than discretionary spending. Now add on pricing power, and the sector’s long‑term earnings power has proven resilient across cycles.

Meanwhile, utilities have been benefitting from grid investment, electrification and data‑center demand. The energy needs of the tech sector haven’t gone away – perhaps that’s why the utilities sector, despite depreciating year-to-date, is selling off by less than half of the move seen in the consumer staples sector. Plus, with higher oil prices, utilities retain the flexibility to substitute natural gas for oil when economically advantageous.

And yet, the classically defensive sectors of healthcare and utilities continue to trade with broader risk sentiment – even as their earnings growth estimates top those of their “inflation playbook” counterparts.

Poised for above-average earnings growth

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

On sale

It’s not enough to have a compelling earnings story. Stock valuations must be attractive relative to that growth. And if there is a catalyst not embedded in the valuation, all the better.

Valuations across oil and gas companies sit well above long‑term averages, supported by years of capital discipline and shareholder return policies. With the Strait of Hormuz effectively closed, and oil supply therefore trapped, demand is disproportionately higher. Naturally, earnings expectations will reflect the resulting higher global price.

But it works in the other direction too. A de-escalation and the consequent oil price reduction yields the possibility of earnings revisions. Note, the crude futures curve continues to price oil below $80 per barrel in the back half of the year.

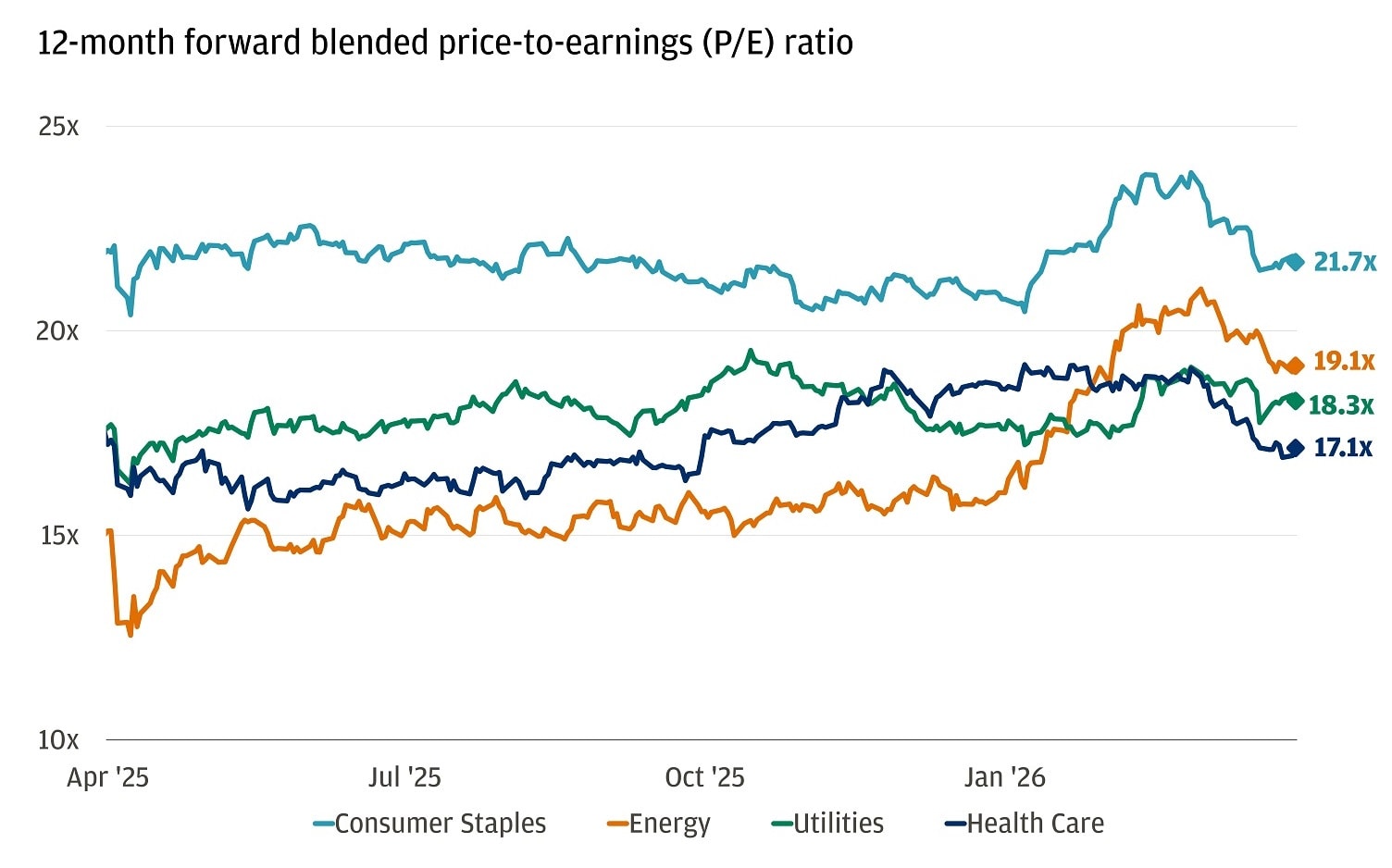

Consumer staples tell a similar story. Once the quintessential safety trade, the sector now faces margin pressure from lingering input costs, waning pricing power and a consumer that is increasingly value‑conscious. Now add on earnings growth expectations sitting below the market average and elevated valuations (relative to history).

Inflation-exposed sectors trade at rich valuations

The bigger valuation gap is overseas

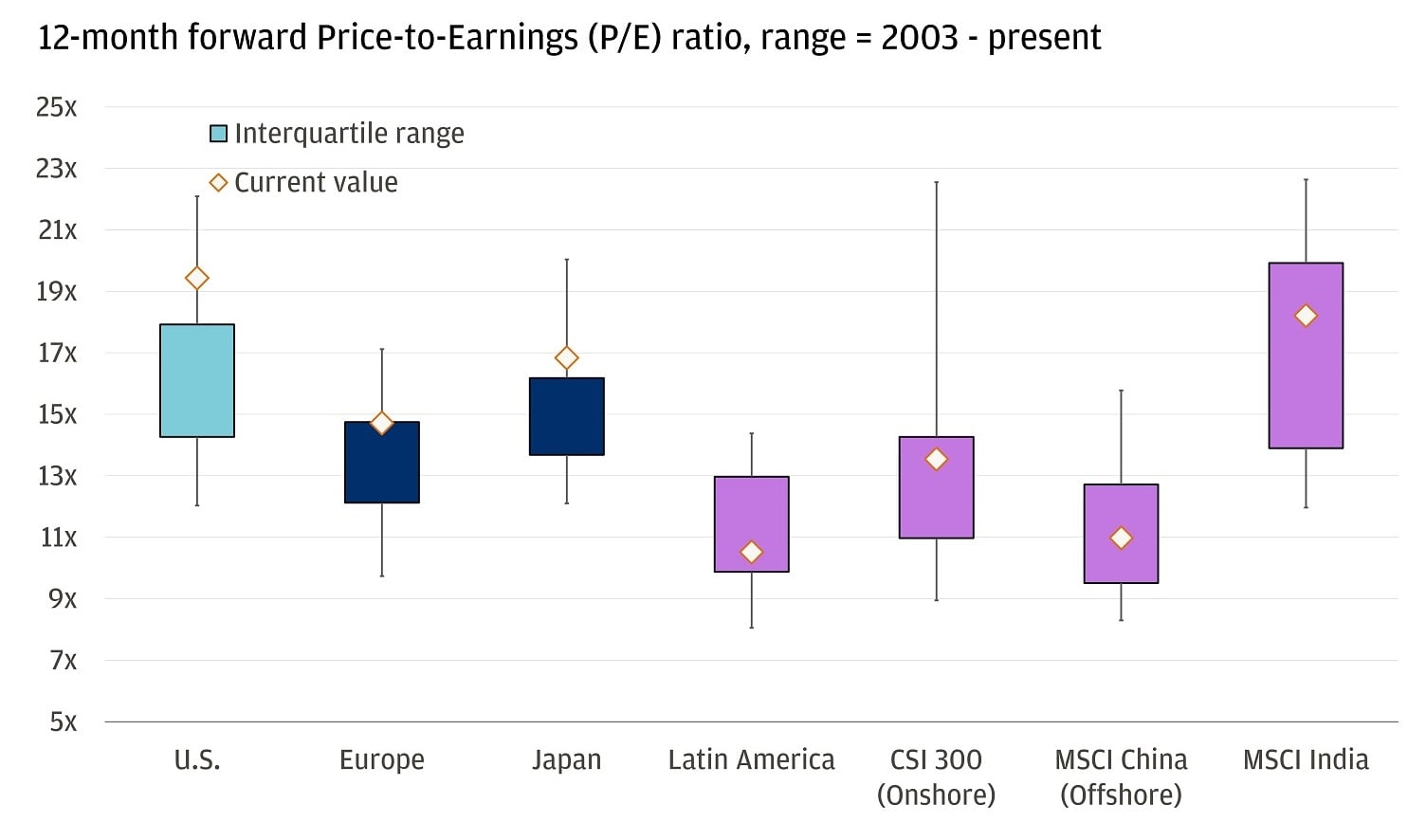

In times of geopolitical crisis, it’s common to see sentiment overshoot fundamentals. And it’s not just an S&P 500 story. When it comes to what regions may be poised for a recovery, take a look at Latin America.

Despite posting macroeconomic resilience, stable inflation, fiscal consolidation, nearshoring and energy independence, the MSCI Emerging Markets Latin America Index has dropped over 12% since the conflict in Iran began. Latin America’s valuation discount is less about deteriorating fundamentals and more about a higher risk and currency discount being applied to the region. But even as earnings are being revised upward, the region has faced a similar sentiment-driven drop primed to bounce back upon conflict resolution.

Now add in valuations. The index is trading at a roughly 10.2 forward multiple, which not only screens cheap against major peers, but also compared to its own historical average of about 11.5. Compared to the broader emerging market group, it’s trading at a 51% discount. That’s the largest valuation gap in 20 years. Even Europe, which is far more vulnerable to the fallout of higher energy prices and will need a longer recovery time, trades at a higher premium.

Inflation-exposed sectors trade at rich valuations

All market and economic data as of 04/02/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Executive Director, Global Investment Strategist, J.P. Morgan Private Bank

Global Investment Strategist