Emerging markets may offer more than meets the eye – selectivity matters

Global Investment Strategist

By Joshua Lewin and Federico Cuevas

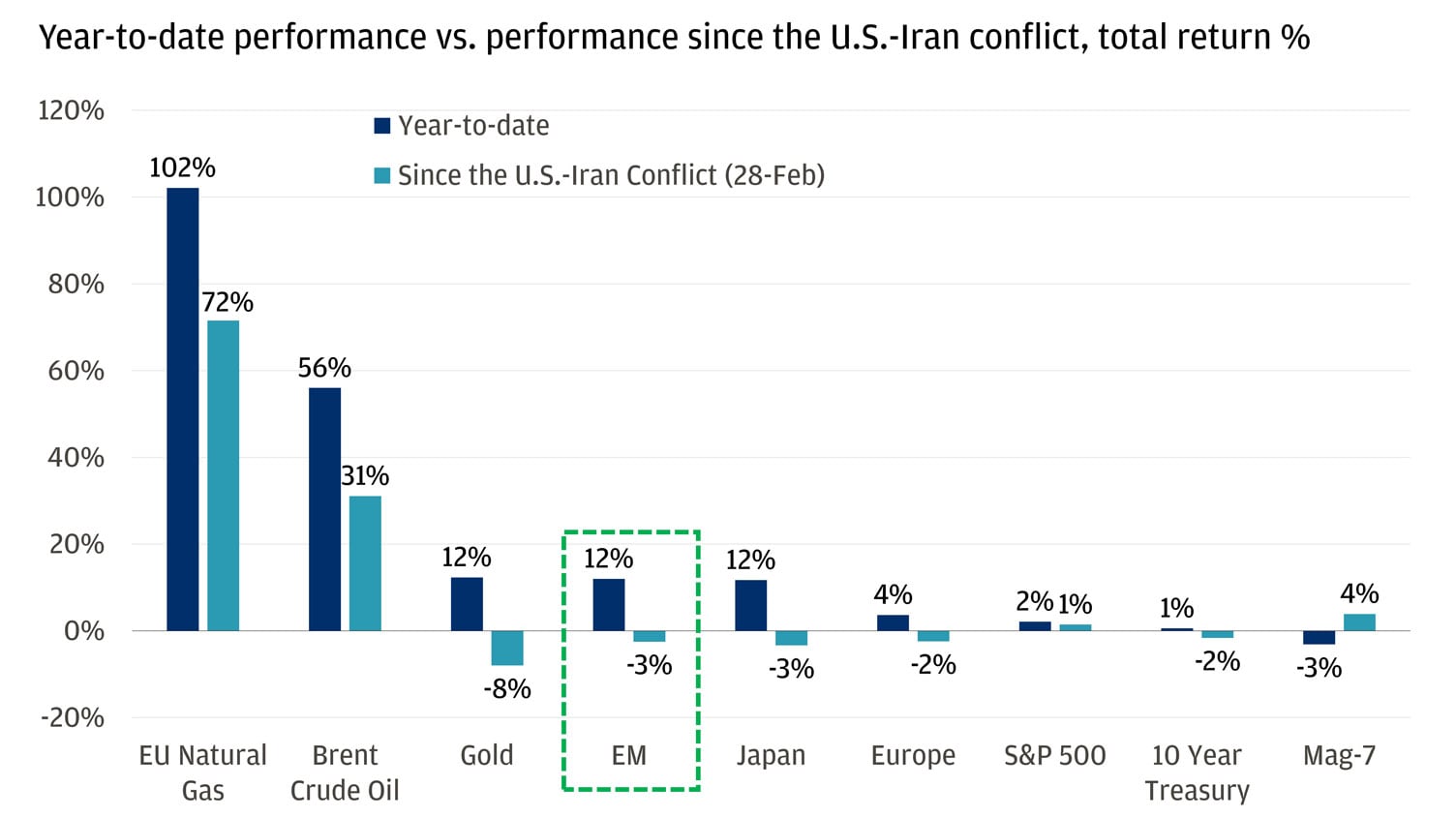

A rise in global conflict and pickup in market volatility would normally argue for caution on emerging markets (EMs). This riskier backdrop can feed inflation and pressure currencies, tighten financial conditions and reinforce the kind of risk-off positioning that tends to weigh on countries outside of the developed world. Yet that familiar playbook has not fully matched market behavior. Emerging markets have outperformed most developed-market peers through the war in Iran and year-to-date. This is because many economies are less capital reliant than they were in past cycles, the oil shock from Iran is not hitting every country the same way and some of the most important structural tailwinds for these markets remain in place.

As a result, we’re constructive – though selective – within emerging markets, with our strongest conviction in South Korea, Taiwan and parts of China. Latin America is also becoming increasingly relevant as the EM opportunity set broadens.

EM is a top 2026 performer, holding up during the conflict

Outlooks and past performance are no guarantee of future results. It is not possible to invest directly in an index.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

A larger shock absorber

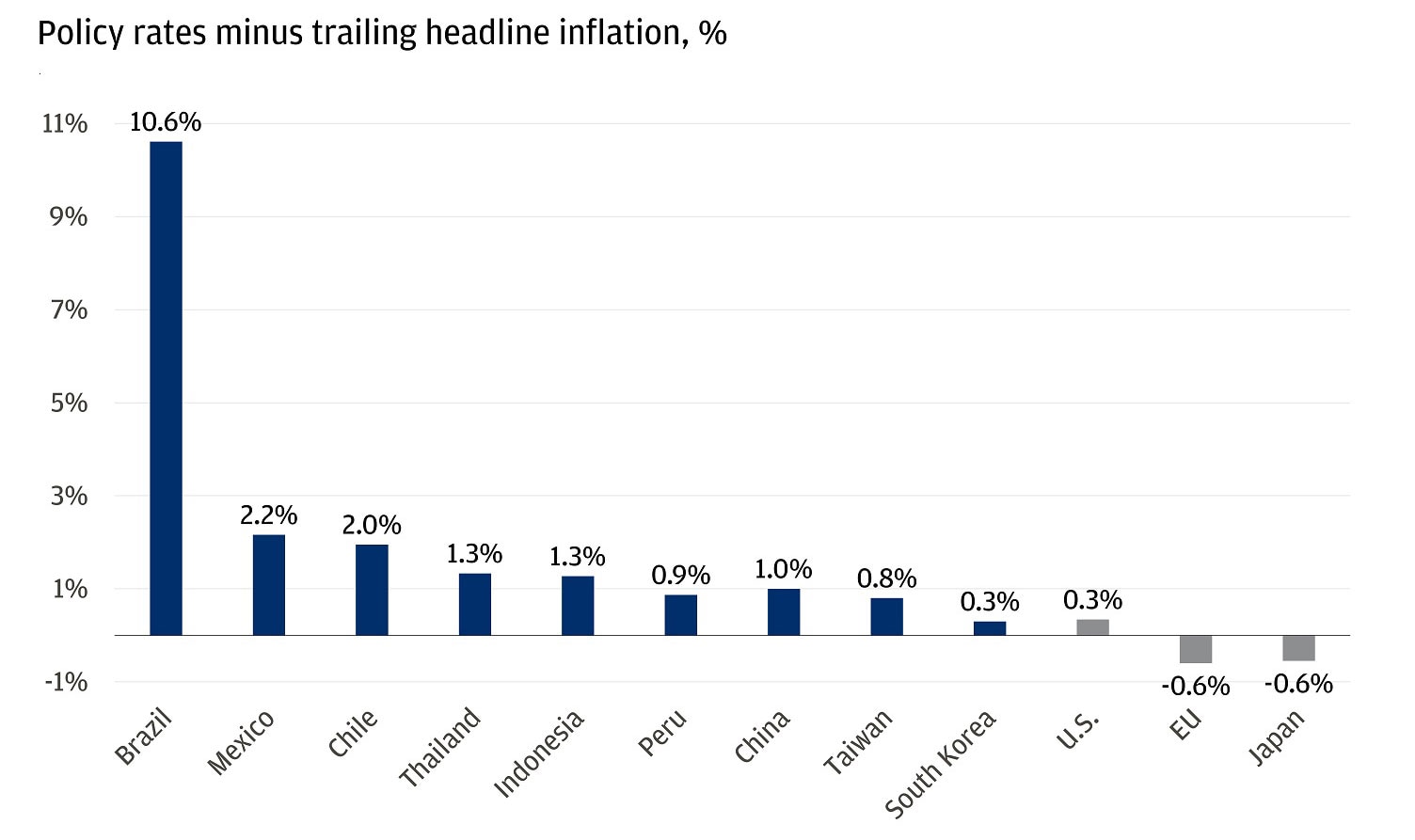

Many EMs entered this period with fewer vulnerabilities. Current account balances have improved relative to previous shocks, reducing a reliance on external financing. Reserve accumulation has also risen over time, providing dry powder to prevent an unmanaged foreign exchange (FX) sell-off. The Bank for International Settlements (BIS) notes that FX reserves climbed from about 5% of gross domestic product (GDP) in 1990 to nearly 30% by 2018. This cushion extends beyond reserves into policymaking: in parts of EMs, inflation has been brought under better control and central-bank credibility is stronger. This is reflected in positive real policy rates which are higher and more restrictive relative to history and relative to a number of more developed markets.

Several large EMs offer among the highest real policy rates

The oil shock matters, but exposure is uneven – and not just across EMs

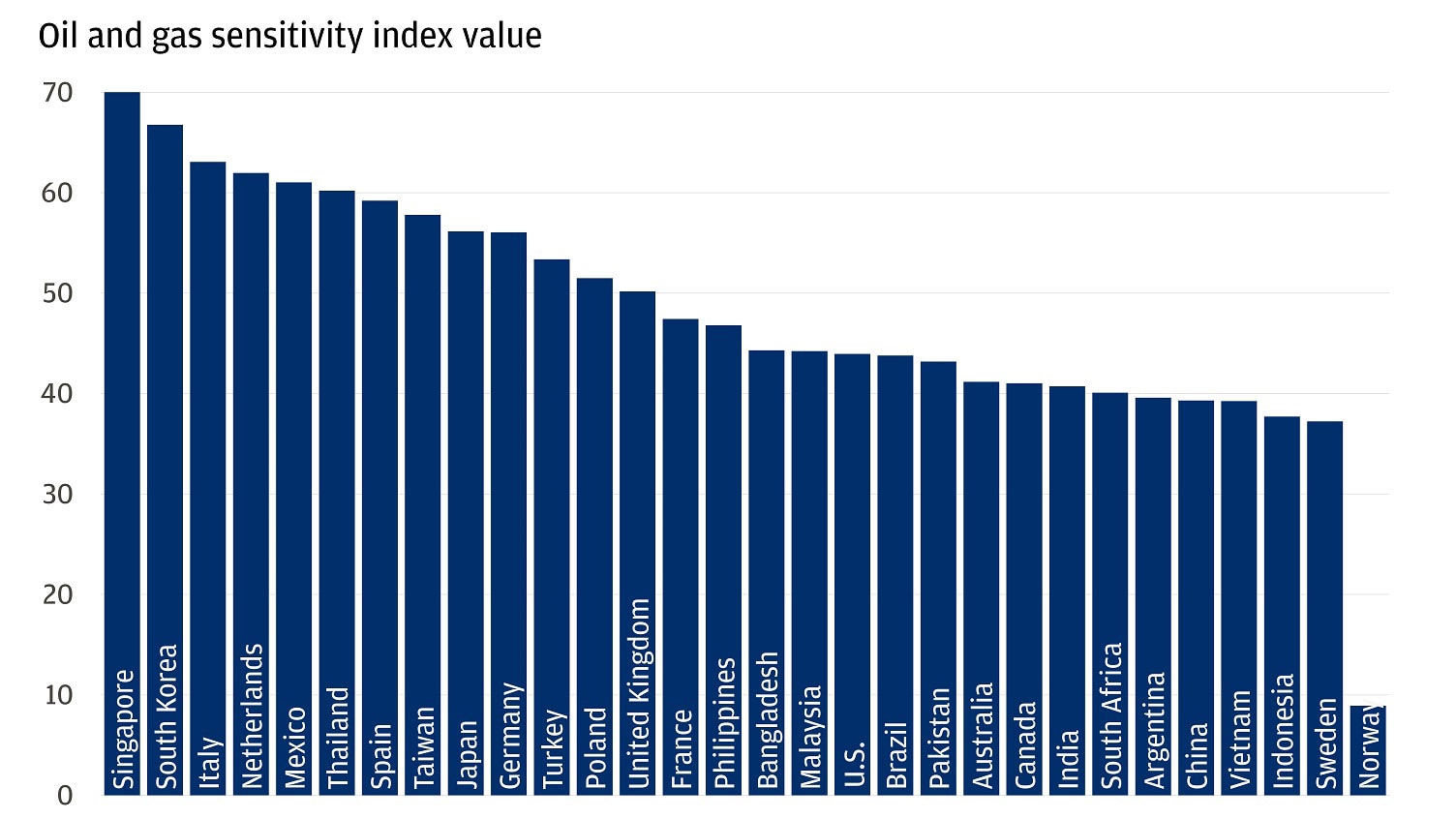

The second reason broad EM caution can miss the mark is that energy vulnerability is not uniform – and is arguably a greater challenge for some developed economies. Sensitivity to a prolonged Gulf conflict depends on more than energy imports alone: It also reflects how reliant an economy is on imported oil and gas, how large those fuels are in the domestic energy mix and how energy-intensive it is. On that basis, parts of Asia screen as more exposed, while parts of Latin America look materially less vulnerable. The contrast also extends beyond EMs. The EU still imports 57% of its energy needs, and its natural-gas import dependency rate remains above 85%, showing that external energy exposure remains significant in parts of Europe as well.

Oil & gas sensitivity varies among EMs

It’s not just the absence of a negative: Favorable tailwinds for EMs

Emerging markets stand to benefit from two of the larger structural forces we see driving markets today: the buildout of artificial intelligence (AI) and the global fragmentation that is reshaping supply chains and intensifying the push for critical inputs and resources. In Asia, Taiwan sits near the center of the manufacturing stack: TSMC represented 34% of the global “Foundry 2.0” industry in 2024, a category that includes chip manufacturing, advanced packaging, testing and mask-making. South Korea is similarly important, with Samsung and SK hynix together controlling about 68% of the global DRAM market (dynamic random-access memory; chips) in Q4 2025.

China is increasingly important as an AI end-market in its own right, with 515 million generative AI users as of June 2025, equal to 36.5% penetration, and rapid adoption of agentic AI likely to drive further growth. Chinese stocks have lagged the broader recovery as platform giants prioritize reinvestment over near-term profits, but with earnings now largely reset, profit growth is expected to accelerate through 2027.

Latin America’s structural support looks different, but no less strategic. Chile and Peru together account for nearly 40% of global copper production, while Brazil is emerging in nickel and rare earths, both critical for batteries and high-tech manufacturing. Mexico strengthens the case further: United States Census Bureau data shows it has overtaken China in exports of advanced technology products to the U.S. In a world focused on supply security, those advantages are increasing the region’s strategic importance.

All market and economic data as of 04/17/2026 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist