Delayed September jobs report beats forecasts while unemployment rate ticks up

Editorial staff, J.P. Morgan Wealth Management

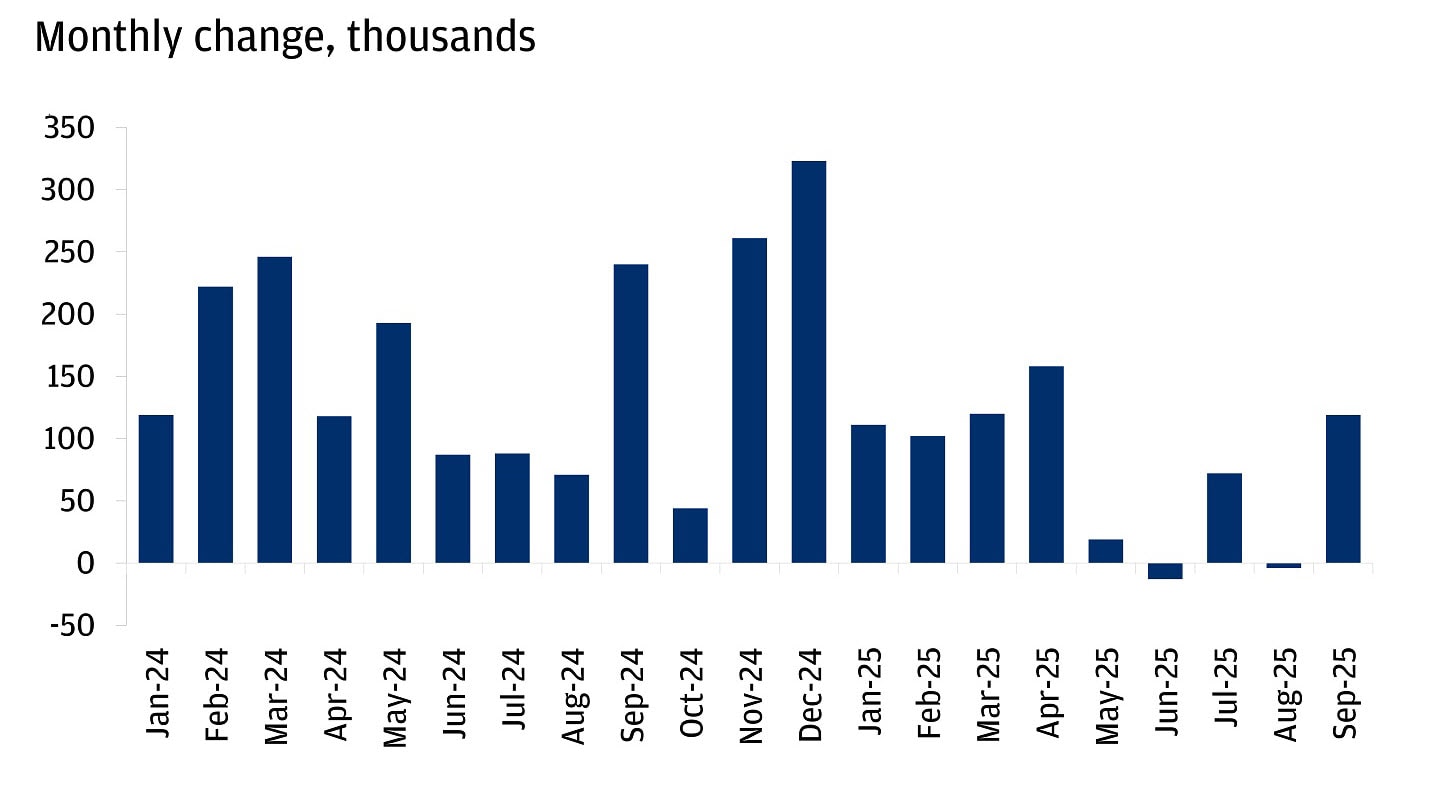

- The Bureau of Labor Statistics’ delayed September jobs report showed payroll growth of 119,000, beating many forecasts.

- September’s unemployment rate increased slightly to 4.4%, the highest it’s been since the middle of the pandemic.

- Wage growth held at 3.8% year over year, but some high-income earners, especially those in information services and financial activities, saw stronger gains than most lower-income workers.

Collection of official labor market data is back up and running after the longest shutdown of the federal government in U.S. history. The delayed September jobs report beat expectations to show the labor market has slowed but is steady. Employers added 119,000 jobs during the month, significantly up from the summer slump, which saw only 72,000 new jobs added in July and a loss of 4,000 in August after being revised down from 22,000.

Per Omar Anabtawi, a Global Investment Strategist at JPMorganChase: “For the hawks, the report showed a big upside surprise on the headline payroll number ... beating all 67 forecasts in Bloomberg’s survey. ... On the other hand, there was an unexpected uptick in the unemployment rate to 4.4%.”

U.S. nonfarm payroll employment

After the government shutdown caused a data blackout, official numbers are back

The recent 43-day shutdown of the federal government caused a “blackout” of some economic data, as Bureau of Labor Statistics (BLS) staff were furloughed and regular reporting was suspended. Federal data stymied included regular BLS nonfarm payrolls and Current Population Survey results, weekly jobless claims from the Department of Labor, and both the October Consumer Price Index (CPI) and Producer Price Index reports.

To fill the gap, investors and economists leaned on alternative sources such as state-level unemployment insurance filings, private-sector data from payroll and placement firms like ADP and Challenger, Gray & Christmas, and industry surveys. These became the only means for gauging the U.S. labor market during the blackout.

Even as regular government releases resume, fall 2025 may remain a blind spot in the historical record. For example, although September’s jobs numbers have now been released, the BLS has announced it will not publish the full October employment report. The agency explained that the extended shutdown disrupted the data collection process for October, resulting in incomplete survey responses and gaps that make it impossible to produce a reliable and accurate report.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

What does the September jobs report tell us?

The official labor market data for September points to a hiring market that is soft but certainly not collapsing.

Nonfarm payrolls rose by 119,000. Average hourly earnings increased 0.2% month over month and 3.8% year over year – higher than inflation but slower than earlier in the cycle. Unemployment, long accepted as a reliable indicator of overall labor market health, ticked up slightly from 4.3% to 4.4%.

The BLS figures line up with what private indicators were signaling in advance. The National Employment Report from ADP Research, for example, shows private employers added 42,000 jobs in October – the report’s first positive reading since July – while annual pay growth for job stayers held at 4.5%.

Data from small businesses echoes the mixed state of the labor market, too. The National Federation of Independent Business reported in October that 56% of small business owners were actively recruiting, especially in the construction and transportation fields. But salary increases have slowed down, and future pay hikes – while still planned – are being rolled out more cautiously.

Lingering concerns about the job market

Although September’s payroll gains exceeded expectations, recent months have brought a series of warning signs that have intensified concerns about the labor market. In October, Challenger, Gray & Christmas reported a 175% increase in job cut announcements compared to a year earlier, raising concerns about potential weakness. At the same time, the Federal Reserve Bank of Cleveland noted 39,006 Worker Adjustment and Retraining Notification Act (WARN) system notices – signaling upcoming layoffs – across 21 states in October. This represents the highest monthly total since August 2023 and of the highest readings since tracking began in 2006.

While layoffs have increased, hiring announcements have outpaced them, suggesting continued demand for workers. Additionally, intentions to hire among small businesses are showing signs of improvement, indicating resilience in the broader labor market.

What does the jobs report mean for the Federal Reserve – and potential future interest rate cuts – looking forward?

In October, the Federal Reserve (Fed) delivered a small but widely expected interest rate cut, setting the fed funds rate at a 3.75% to 4.00% range. The Federal Open Market Committee (FOMC) – which votes on interest rates – has signaled that it is closely watching the labor market when it comes to making its decision on future cuts, with its next decision on rates set for December.

Fed Chair Jerome Powell stated the following in remarks on October 29: “In this less dynamic and somewhat softer labor market, the downside risks to employment appear to have risen in recent months.” Still, he reinforced the Fed’s directive. “Inflation has eased significantly from its highs in mid-2022 but remains somewhat elevated relative to our 2 percent longer-run goal. ... Our monetary policy actions are guided by our dual mandate to promote maximum employment and stable prices for the American people.”

Fed officials have been openly divided on preferred next steps ahead of the upcoming meeting, and September’s jobs numbers may intensify divisions. On one hand, strong job growth suggests pausing rate cuts; on the other, rising unemployment may encourage easing.

The bottom line

The delayed September jobs report confirms patterns that private data had already revealed: The labor market has softened, layoffs are more visible and wage growth is slowing. Even so, the labor market is showing signs of resilience.

The key question going forward is whether October and November’s numbers will show continued hiring momentum or signs that September’s surge was temporary. The unemployment rate will also be closely watched.

Underlying metrics such as wage growth, labor force participation and revisions to prior data may be helpful to gauge where the labor market truly is as 2026 approaches.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Editorial staff, J.P. Morgan Wealth Management