January jobs report shows 130,000 new jobs, slightly lower unemployment: What it signals for 2026

Editorial staff, J.P. Morgan Wealth Management

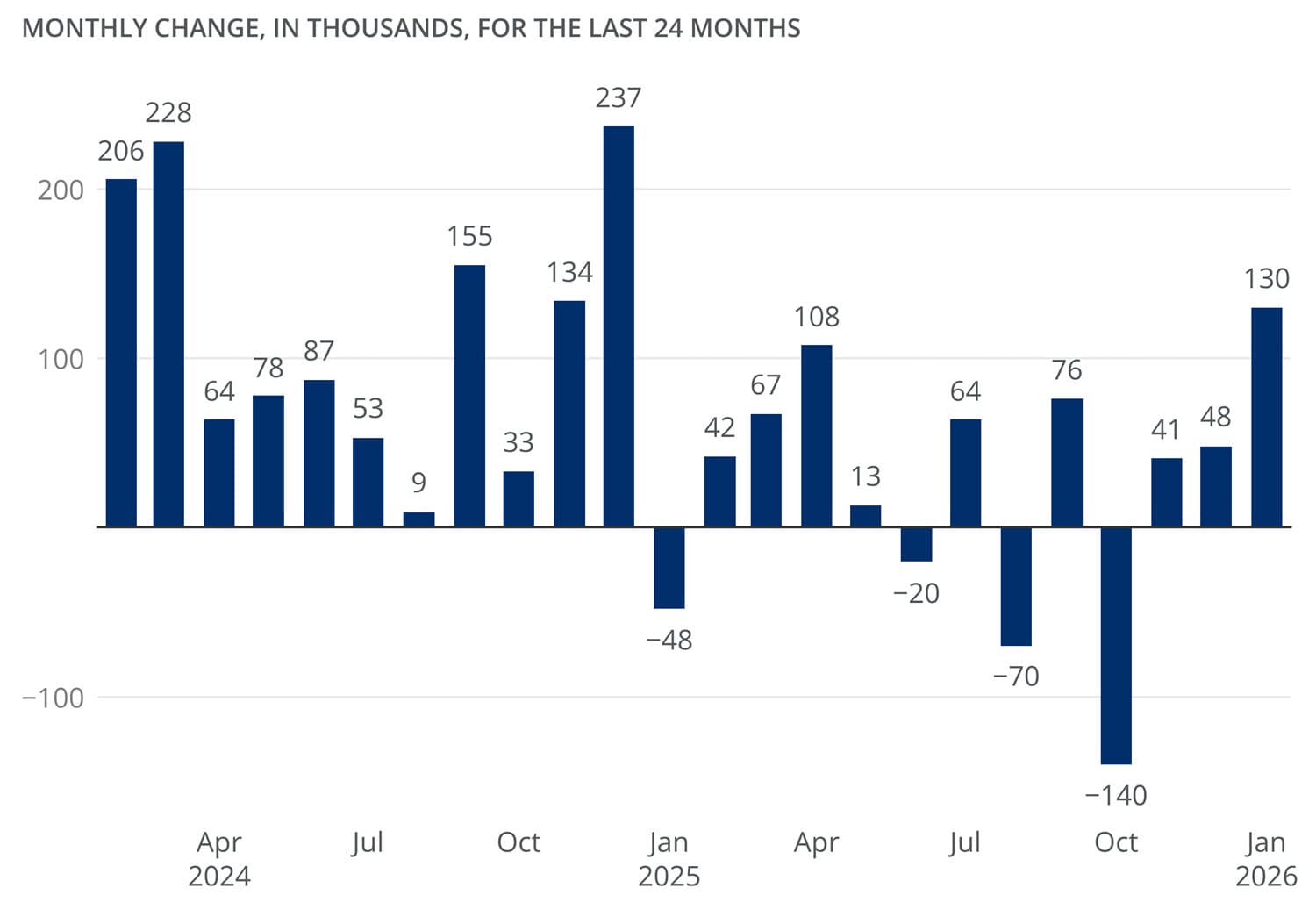

- Employers added 130,000 jobs in January – more than the expected 65,000 – with companies in health care, social assistance and construction leading in number of hires. Meanwhile, the federal government and financial activities sectors saw job declines.

- Notably, the private sector added 172,000 jobs, beating estimates of 68,000, with 124,000 of those added in health care.

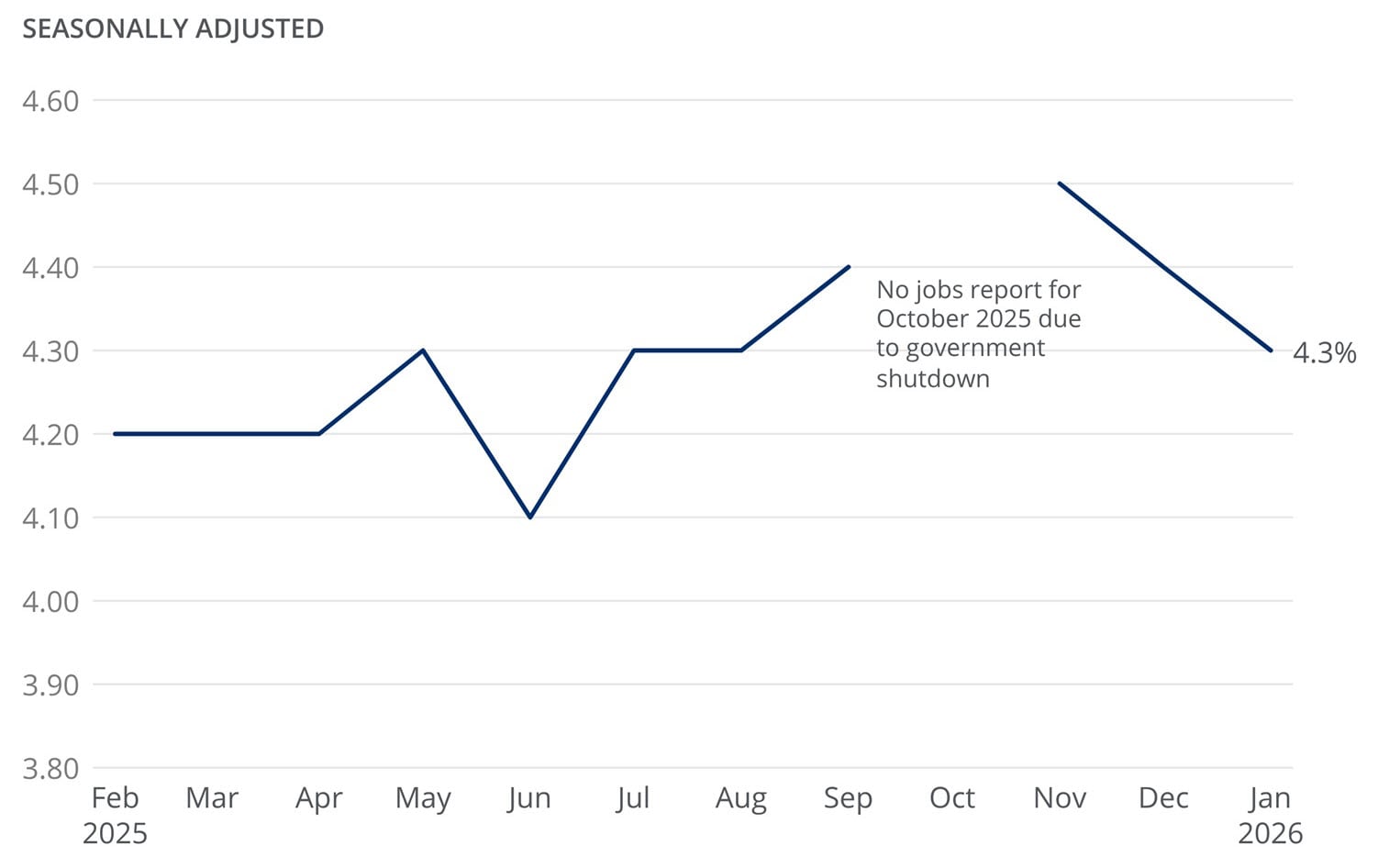

- Unemployment in January dropped slightly to 4.3%, from 4.4% in December, while year-over-year average hourly earnings growth remained constant at 3.7%.

- As the first jobs report of 2026, January’s numbers reveal the labor market is showing signs of troughing. Our strategists see further stabilization through 2026 as cyclical growth improves.

After a delay caused by a brief government shutdown, the release of the January Employment Situation provides a glimpse into how employers started the year. The numbers look better than expected, with 130,000 jobs added, average hourly earnings growing by 0.4% month over month and a slightly lower unemployment rate of 4.3%. The private sector alone added 172,000 jobs.

U.S. Nonfarm Payroll Employment

Employers in health care, social assistance and construction continued to add people to their payrolls, while jobs in the federal government and financial activities sectors declined. At least some of the decline in government positions can be explained by employees who voluntarily resigned as part of the deferred resignation program, which allowed them to work through a specified end date such as the end of 2025.

The January jobs report also included revised numbers for 2025. The average number of jobs added per month was revised down from 50,000 to 15,000, after total jobs added in 2025 came to 181,000 – much lower than the previously estimated 584,000. Despite the negative revisions to payroll gains throughout last year, our strategists are encouraged by the January report, which signaled positive revisions to private sector job gains in November and December, along with the strong January figure. All told, the average monthly gain in payrolls over the past three months is close to 100,000, a notable improvement from the three-month average payroll gain in August 2025, which was near zero.

What does the jobs report tell us every month?

Every month, the U.S. Department of Labor’s Bureau of Labor Statistics (BLS) runs two big surveys. One asks households whether people are working or looking for work (the Household Survey) – that’s where the unemployment rate comes from. The other asks companies and government agencies how many people are on their payrolls and what they’re paying them (the Establishment Survey) – that’s where the headline jobs number and wage data come from. Because one survey talks to workers and the other talks to employers, they can sometimes tell different stories, especially when things are shifting.

The jobs report matters because it shows whether people are finding work and earning more. When lots of jobs are being created and unemployment is low, for example, people typically have more money to spend. Alternatively, high demand for workers and a limited supply of available workers can drive wages upward, along with prices at stores and restaurants. And when the unemployment rate is high and companies continue to shed jobs, the larger economy suffers.

The Federal Reserve (Fed) watches this data closely when deciding whether to raise or lower the federal funds rate, hoping to keep as many people employed as possible without letting the cost of living spiral out of control.

Following the Fed’s January meeting, the Federal Open Market Committee (FOMC) decided to leave its benchmark interest rate unchanged at 3.50%–3.75% after three quarter-point rate cuts in late 2025. At that time, Fed Chair Jerome Powell said the FOMC would continue to make “decisions on a meeting-by-meeting basis,” regularly checking new data – including BLS’s monthly jobs report – to determine if the economy needs more help or not. If unemployment spikes quickly – which it hasn’t done so far – the Fed will face harder choices about whether to cut rates again, even if inflation isn’t all the way back down to its 2% target. There will be one more jobs report before the Fed’s next meeting.

Interested in working with an advisor?

Work 1:1 with our advisors to help build a personalized financial strategy that’s built around you.

Unemployment rate by month

The unemployment rate has crept up from the historically low levels of a couple years ago. The rate is still not near what it might be during a recession, and our strategists are encouraged by the past few months, which have shown a slight decline.

Here’s a snapshot of how unemployment has trended over the past year:

Unemployment Rate: Last 12 Months

Will the job market improve in 2026?

A few things have made businesses cautious: uncertainty about tariffs and trade, stricter immigration rules that have reduced the number of workers available and big investments in technology that haven’t yet made the overall economy more productive. The recent phenomenon of modest hiring is likely to continue in early 2026, with unemployment probably topping out around 4.5%.

Looking toward the second half of 2026, there are a few reasons to think hiring may improve slightly. Tax changes (in particular, larger tax refunds) could put more money in people’s pockets, and lower borrowing costs stemming from the Fed’s 2025 rate cuts could make borrowing cheaper. Businesses should have more clarity around trade policies, and if technology investments start paying off in real productivity gains, companies might feel more comfortable staffing up.

When is the next jobs report?

The BLS typically releases the Employment Situation Summary on the first Friday of each month. The next jobs report, covering employment data from February 2026, is scheduled for release on March 6 at 8:30 a.m. ET. The report is published early in the morning to give investors and policymakers time to digest the data before financial markets open.

The bottom line

After a brief shutdown-related delay, the January jobs report has some good news – more jobs than anticipated and lower unemployment. February’s employment situation, scheduled for release in a little over three weeks, will be a critical piece of information for the Fed as its March meeting approaches.

While the uncertainty may continue for a little while, investors’ outlooks should be buoyed by the ongoing resilience of the labor market. Investors should also keep an eye on their long-term goals instead of reacting to short-term volatility.

If you need support, talk to a J.P. Morgan financial professional to learn how to best manage your cash flows in this evolving economy.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management