August inflation ticks up slightly: Is the Federal Reserve still on track for a rate cut?

Editorial staff, J.P. Morgan Wealth Management

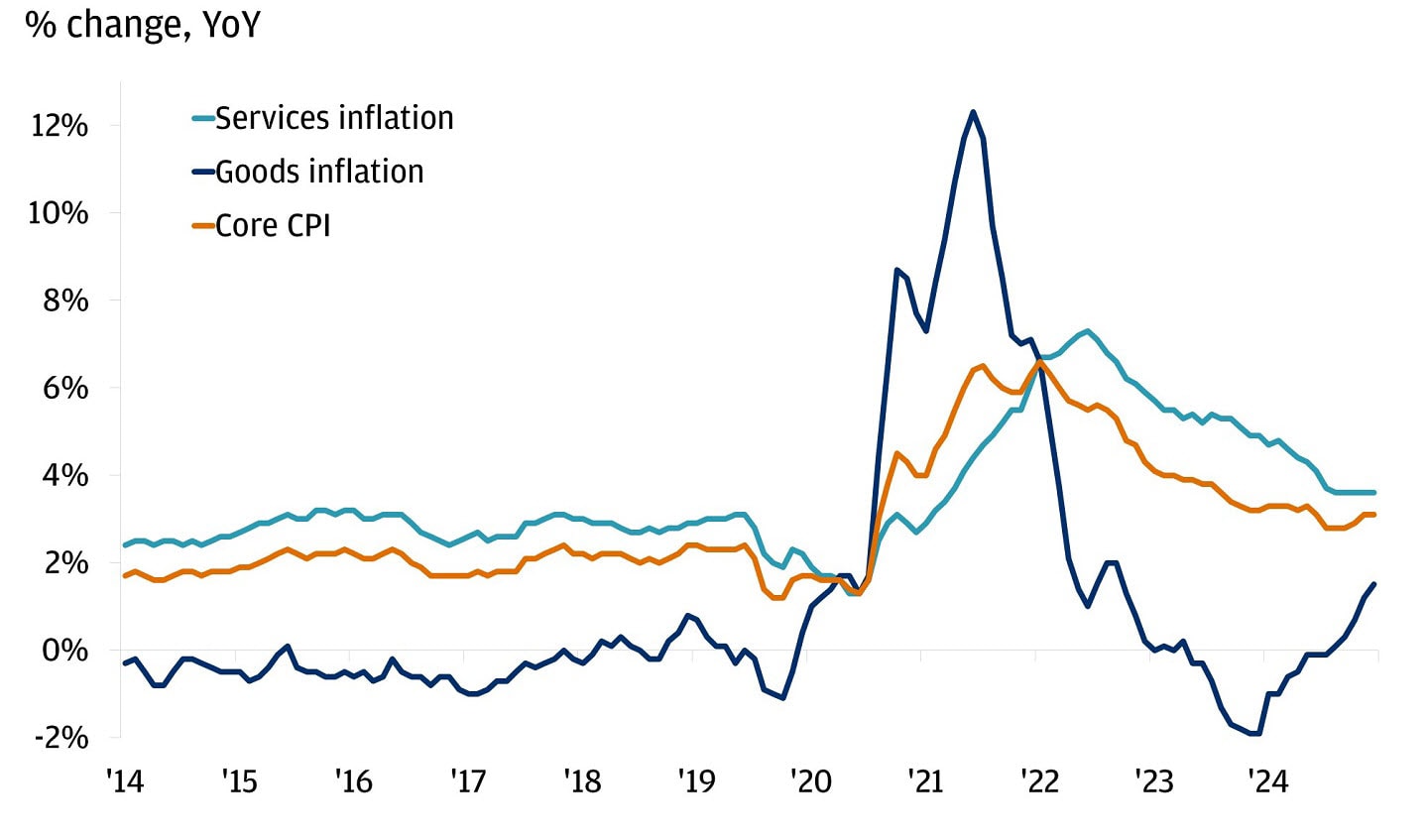

- Headline CPI rose 0.4% in August and 2.9% year-over-year; core CPI rose 0.3% and 3.1% year-over-year, up slightly from 2.7% in July.

- Housing costs climbed 0.4% month-over-month, the largest factor in driving inflation in August.

- Following the inflation data release, our strategists still believe a Federal Reserve rate cut is forthcoming at its meeting next week.

The cost of living climbed even faster in August, with grocery bills, in particular, putting strain on household budgets. The August 2025 Consumer Price Index (CPI) from the Bureau of Labor Statistics increased 0.4% from July and 2.9% from a year earlier.

Core CPI, which excludes more volatile food and energy prices, rose 0.3% for the month and held steady at 3.1% over the past year, remaining well above the Federal Reserve's 2% target for annual inflation.

August CPI print is in-line with expectations

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

What does the August CPI data mean for inflation this year?

The August report shows inflationary pressure remains beyond just the tariff-affected goods categories. Food and energy costs, which have provided some relief during earlier summer months, both accelerated in August.

Housing costs also picked up pace, contributing the largest share to the monthly increase. Despite the monthly increase, our strategists continue to see housing costs on a disinflationary path going forward.

Inflation might remain above the Federal Reserve (Fed)’s 2% target for several more quarters. The policy target is designed to keep prices stable while allowing for moderate economic growth. Too much inflation erodes purchasing power, while too little can signal weak demand and slow growth.

How did prices change for consumers in August?

Rent and housing costs accelerated again

Shelter prices, which make up about one-third of the inflation calculation, rose 0.4% in August. This marked the largest monthly increase in the past year and the biggest single factor driving overall inflation higher. Owners' equivalent rent rose 0.4% in August and 4% over the past year, while rent of primary residence increased 0.3% for the month and 3.5% for the year.

Fuel and energy costs climbed in August after cooling earlier in the summer

Gasoline prices jumped 1.9% in August after falling 2.2% in July, pushing the overall energy index up 0.7%. Natural gas prices fell 1.6%, while electricity costs rose slightly by 0.2%. The steep reverse in energy prices wiped out some of the biggest relief to household budgets this summer when gas prices declined.

Grocery bills surged last month

After a brief break, food costs started accelerating again with families paying notably more for fresh produce and other staples, likely, at least in part, driven by tariffs. The 0.6% monthly increase in grocery prices represents an annual pace of over 7%. If sustained, that’s well above wage growth for most households.

Restaurant prices continued their steady climb as well, increasing 0.3% as full-service meals rose 0.4%, leading families to reconsider eating out.

It's also getting more expensive to travel

Hotel prices climbed 2.6% after getting cheaper earlier in the summer, and airline fares surged 5.9% for the month, likely reflecting seasonal travel demand patterns and capacity constraints.

Did tariffs create more inflation in August?

Businesses continued a gradual pass-through of tariff costs to consumers last month, but the effects are still moderate. Price changes were mixed in the main product categories that tend to be more exposed to tariffs.

Apparel prices rose 0.5% in August, five times faster than in July, while the cost of household furnishings and supplies increased by just 0.1% after climbing 0.7% in the prior month. Toys and footwear got even cheaper after earlier price declines. Appliances got 0.4% more expensive after becoming more affordable in July. New vehicle prices also increased 0.3% after remaining flat in July.

The impact of these new import taxes may take time to flow through to customers, even though they started taking effect months ago.

Elyse Ausenbaugh, Head of Investment Strategy for J.P. Morgan Wealth Management, believes that any tariff-related price increases could be short-lived.

“The inflation pick-up in goods categories stemming from tariffs shouldn’t derail the Fed’s easing bias,” Ausenbaugh said. “There is evidence from the tariff episode in President Trump’s first term that suggests the impact could indeed be temporary. More important is the trend we continue to see in the services sector, where there are few signs that price pressures are reaccelerating.”

How does August’s CPI data affect the Federal Reserve?

While the headline CPI raises some concerns about food and energy costs, core inflation for August was still in line with expectations and should give policymakers room to lower interest rates. Our strategists still expect the Federal Reserve to cut rates by 25 basis points at its September 17 meeting, particularly given recent employment data pointing to a steep slowdown in hiring.

“The path for the Fed to deliver what the market is expecting looks clear from our perspective,” Ausenbaugh said. “With inflation printing in-line with expectations and the labor market not giving us signs of improvement, a cut is in order.”

The average monthly job gains over the past three months have fallen to just 29,000, the slowest pace since the recovery from the Global Financial Crisis, excluding the pandemic period. With unemployment rising to 4.3% and hiring momentum clearly waning, Fed policymakers appear ready to provide “insurance” cuts to support continued economic expansion.

What does the August CPI data mean for investors?

The August inflation data doesn't alter our strategists' fundamental approach to portfolio positioning, though it does highlight the importance of maintaining diversification across asset classes and geographies in the current environment.

With the Fed expected to cut interest rates despite higher inflation, our strategists suggest that investors consider diversifying beyond traditional fixed income. They see opportunities in investment-grade corporate bonds, longer-duration municipal bonds and hybrid securities like bank preferreds. These positions can help investors lock in current yields before cash rates decline.

“We’ve been encouraging investors to dust off their ‘Fed rate cutting playbooks,’” Ausenbaugh said. “Amid our expectation that these cuts will play out in a no-recession backdrop, the evolving environment is one in which we see potential for continued equity outperformance in the U.S. and abroad, and a renewed urgency to address reinvestment risk on cash and ultra-short term fixed income positions.”

For equity investors, the combination of persistent inflation and anticipated Fed easing creates a complex backdrop. Valuations remain elevated across many sectors, and our strategists continue to expect periods of volatility as markets navigate policy uncertainty and economic transitions.

As always, consult with a J.P. Morgan advisor to understand what this data could mean for your portfolio.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Editorial staff, J.P. Morgan Wealth Management