Exploring mutual funds (and how to invest in them)

- Mutual funds allow investors to buy shares of a larger fund containing multiple securities like stocks, bonds and other assets.

- Some mutual funds are actively managed, while others are passively managed.

- Passively managed funds aim to track the market through the performance of a market index like the S&P 500.

- Actively managed funds are controlled by a manager or a management team whose mandate is to outperform (or beat) the market or index.

- Investors who are closer to retirement may want a comparatively low-risk, low-reward mutual fund. Conversely, younger investors might opt for a comparatively high-risk, high-reward fund.

A mutual fund is a cornerstone for investors seeking straightforward opportunities to diversify and grow their wealth. They offer a range of investment strategies, management styles and asset allocations, making them suitable for different risk appetites and financial goals. Let’s look at how mutual funds work, the types available and how they might fit into your investment strategy.

What is a mutual fund?

A mutual fund is a professionally-managed investment that pools together your money, along with other investors’ money, to invest in a portfolio of securities, like stocks or bonds. Around 71 million American households use mutual funds to invest for their long-term goals. When you invest in a mutual fund, you’re buying a share of the fund that equals a portion of ownership in its holdings. As the fund’s total holdings rise and fall over time, the value of your investment also goes up or down. If the underlying stocks or bonds pay dividends or income, you receive your share of that too.

How does a mutual fund work?

A mutual fund is a way for investors to pool their money together to buy securities like stocks and bonds. When you make a mutual fund investment, you are buying a share, or a percentage, of that fund. You do not directly own the stocks that the fund purchases. As the fund’s total holdings increase and decrease in value over time, the value of your share of the fund also fluctuates.

Mutual fund orders are generally executed once per day after the market closes at 4 p.m. ET. Shares of a mutual fund can usually be bought or sold through a brokerage, an advisor or directly through the fund. Mutual fund shares tend to be very liquid, meaning they can be easily bought or sold.

Types of mutual funds

There are several different types of mutual funds, each with their own potential advantages and disadvantages. Certain mutual funds focus on one specific kind of asset, like stocks or bonds, while others invest in an array of asset types. That said, there are four main types of mutual funds that are generally popular with investors:

- Stock funds: Also known as equity funds, these focus on investing primarily in stocks.

- Bond funds: Also called fixed-income funds, these invest mainly in bonds or other debt securities.

- Balanced funds: These invest in a mixture of stocks, bonds and other securities to help diversify.

- Money market funds: These invest in short-term investments mostly issued by the U.S. government or U.S. corporations with high credit ratings.

Active vs. passive mutual funds

Some mutual funds are actively managed, while others are passively managed. Passively managed funds aim to track the market through the performance of a market index like the S&P 500. Meanwhile, actively managed funds are operated by a manager or management team tasked with making decisions that aim to outperform the market.

Active management often results in more turnover (buying and selling) within the fund’s portfolio. However, outperformance is not guaranteed, and some passive funds may sometimes deliver better returns than active ones. Additionally, increased management costs mean an actively managed mutual fund’s expense ratio is often higher than a passive fund.

Index funds vs. mutual funds

Index funds are a type of passive mutual fund. These funds are a compilation of stocks or bonds listed on a specific index. The risks and returns of these funds track the risks and returns of the index they follow. For example, if an investor owns an S&P 500 index fund and the S&P 500 rises by 2% on a given day, their index fund will likely be up by a similar amount.

Get up to $1,000

When you open a J.P. Morgan Self-Directed Investing account, you get a trading experience that puts you in control and up to $1,000 in cash bonus.

Mutual funds vs. ETFs

Mutual funds and exchange-traded funds (ETF) both help diversify your portfolio, but their structures offer different benefits and challenges. Mutual funds are only traded at the end-of-day net asset value (NAV), whereas ETFs can be bought and sold like individual stocks, giving investors more flexibility to act on market movements throughout the day.

ETFs usually have lower expense ratios and minimum investment requirements, too, making them potentially more accessible than some mutual funds. However, many mutual funds have the potential benefit of increased oversight and more hands-on management. In the mutual funds vs. ETFs debate, there’s no right or wrong answer, and a qualified financial advisor can help highlight which option may be suited to your specific goals and financial circumstances.

Mutual funds vs. ETFs

Mutual funds | ETFs (Exchange-traded funds) |

|---|---|

Basic mechanics | |

Mutual funds buy a diversified portfolio of securities by pooling together money from multiple investors. | ETFs also pool investor funds but are traded more like stocks on an exchange. |

Trading frequency | |

Mutual funds are generally bought and sold after the market closes, which means that investors can only trade based on the NAV calculated at the close. | ETFs can be bought and sold throughout the day at market prices, potentially allowing investors to take advantage of intraday price movements. |

Investment minimums | |

Mutual funds often require a minimum investment amount. | ETFs typically have no minimum investment other than the price of a single share. |

Fees and expenses | |

Mutual funds generally have higher expense ratios due to management and operational costs. | ETFs tend to have lower expense ratios, particularly passive ETFs, though brokerage fees may apply. |

Tax efficiency | |

Mutual funds are generally less tax-efficient due to frequent portfolio adjustments, which can result in taxable events like capital gains distributions. | ETFs are often more tax efficient due to their trading structure, as shares are exchanged directly on the market without requiring frequent internal portfolio adjustments. |

Benefits of investing in mutual funds

One immediate benefit of a mutual fund is the increased diversification. However, mutual funds may generate returns of their own in a number of ways. The three main ways that investors earn money from mutual funds are:

- Dividend payments: When securities in a fund’s portfolio generate dividends, a proportional amount of that is often passed on to investors in the fund.

- Capital gains: When a fund sells a security which has gone up in price, the difference between the purchase price and the selling price is known as capital gains. This amount, minus any ancillary costs, is distributed to investors proportionally.

- Net asset value: Like stocks, if the price of mutual fund shares rises, the value of your investment rises too, and you would make more money upon selling the shares.

How to invest in mutual funds

Here are three key steps to consider when looking to invest in a mutual fund:

Know your budget

It’s generally recommended, before investing, to review your financial situation and determine how much you’re willing to invest. This might help you identify suitable mutual funds to invest in that align with your budget and financial circumstances.

Choose active or passive

It might be helpful to first decide if you want an actively managed fund that aims to outperform the market for a premium or a passively managed fund that seeks to replicate the performance of its target index at a lower cost. Both options present opportunities and considerations of their own.

Understand risk tolerance

Next, it may be wise to consider your investment goals and risk appetite. For example, you may want to consider your time horizon. Longer time horizons offer opportunities to weather market swings and recover from potential losses, encouraging some investors to take more risks for potentially higher rewards.

If you’re closer to retirement, for example, you might prefer lower-risk, lower-reward funds or target-date funds that adjust risk based on age. Alternatively, investors with longer time horizons might be more comfortable with funds targeting more volatile investment options.

Research mutual funds

Before settling on any mutual funds to invest in, it’s generally recommended to thoroughly research your available options. A mutual fund’s expense ratio, its minimum investment requirements and its management style are all key elements that could potentially impact your returns.

Risks of investing in mutual funds

Like any other type of asset, mutual funds pose potential drawbacks for investors, and it’s important to be aware of the risks before making mutual funds a part of your strategy. First and foremost, the holdings of the mutual fund could decrease in value – lowering the value of your shares in the fund. Other key mutual fund risks include:

- Fund mismanagement: Mutual fund managers may engage in strategies like unnecessary trading or window dressing – transactions designed to give the appearance of better fund performance – that could hinder long-term returns.

- Tax and trading inefficiencies: As a mutual fund shareholder, you have little control over the timing of any distributions you receive from the fund and the resulting tax liabilities. In addition, since mutual funds change hands only once per day, after the markets close, they may be less suitable for strategies that require quick trade execution.

- Expenses and fees: The expenses and fees charged by a mutual fund can limit your investment returns. See the next section for details on the types of costs to keep an eye on.

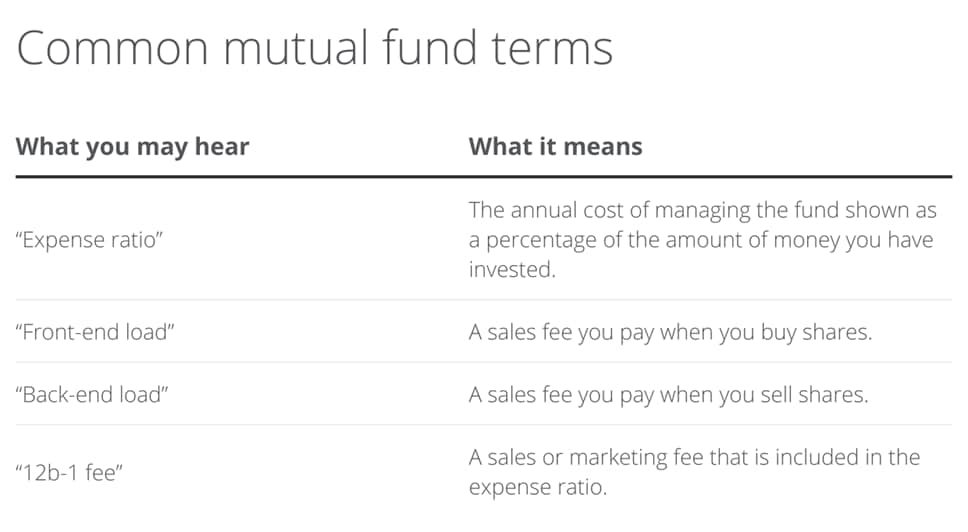

Translating fee jargon

Mutual funds may charge several different fees. Here are some of the fees that you may hear or read about and what they mean:

Common mutual fund terms

Bottom line

Mutual funds offer a diverse range of opportunities for investors to align their investments with their financial goals. Whether you’re seeking market-matching index funds or active management aimed at beating benchmarks, mutual funds aim to provide flexible strategies for every investment strategy. For more tailored guidance, consider consulting a qualified financial advisor who can help you navigate the options and find appropriate funds to complement your portfolio.

Frequently asked questions about mutual funds

Money market funds are a type of mutual fund focused on investing in highly liquid, short-term securities. They are typically managed with the goal of maintaining steady asset value and providing income in the form of interest earnings.

Bond funds are a type of investment fund focused on investing in bonds (government, corporate and municipal) and other debt instruments such as mortgage-backed securities (MBS).

Dividend payments are portions of a company’s or fund’s earnings that are regularly distributed to shareholders as a reliable return on an investment, independent of interest earned. Often associated with large, stable “blue chip” companies, not every investment provides dividends, and rules for distribution may vary.

NAV, or net asset value, is the value of a fund’s assets (i.e., stocks, bonds, cash) minus the value of its liabilities (i.e., operating expenses or debts), divided by the total number of outstanding shares. NAV is often used as an indicator of a fund’s performance.

The Standard & Poor’s 500 Index, commonly referred to as the S&P 500, is an index measuring the stock performance of the 500 largest companies listed on the U.S. exchange, based on market capitalization.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.