U.S. policy uncertainty rises and European equities outperform

Head of Investment Strategy, J.P. Morgan Wealth Management

February kept investors on their toes: Uncertainty around the D.C. policy agenda persisted, economic data delivered a few surprises and international markets gained more outperformance momentum over the U.S.

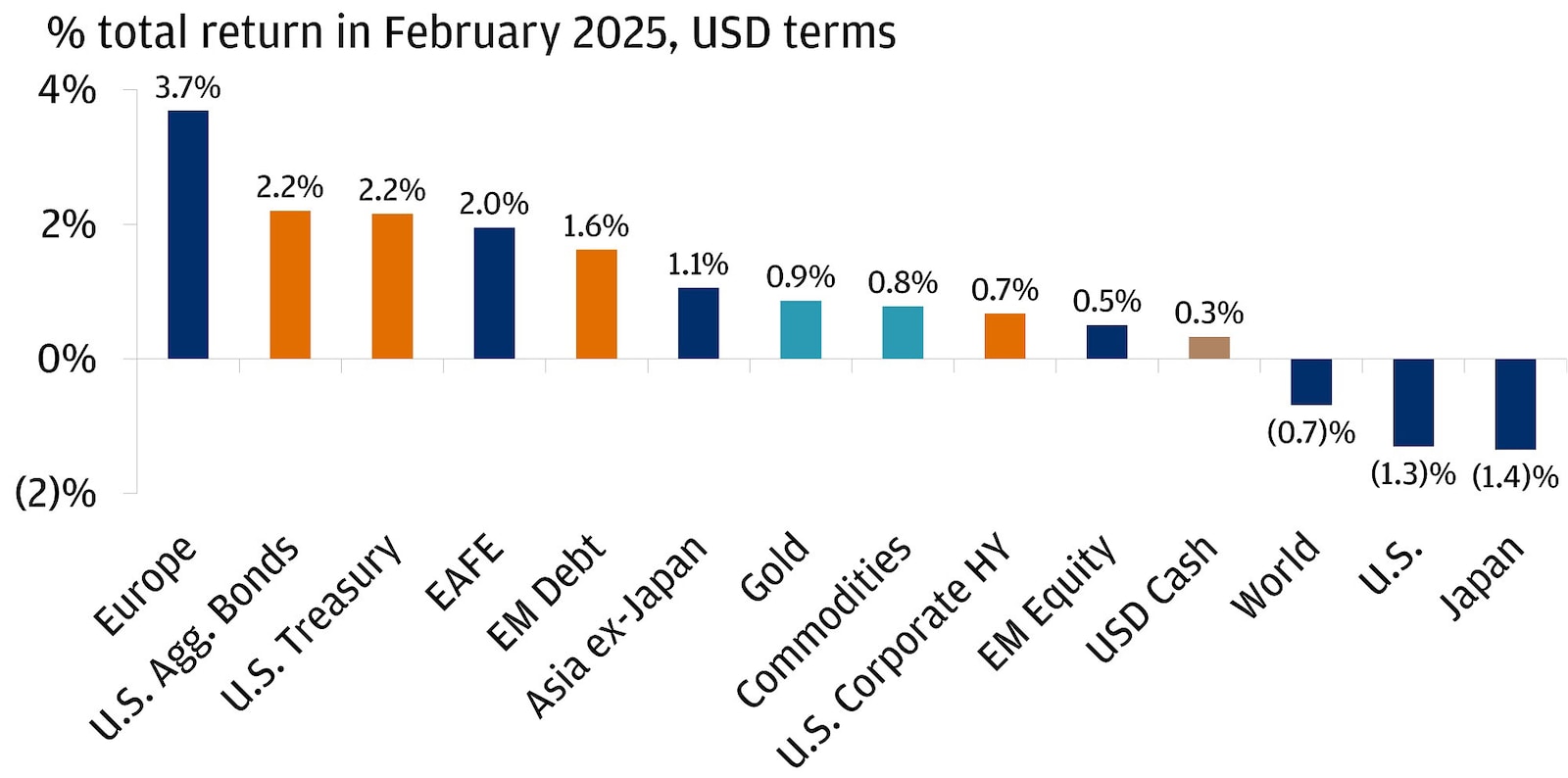

European equities and core bonds led in February

From potential ceasefire talks in Ukraine to mixed signals from sentiment surveys, inflation data and growth indicators, the markets navigated a complex landscape throughout the month. Below, we recap three of February’s defining dynamics: ongoing tariff talk, European equity outperformance and economic data signals.

Tariff talk

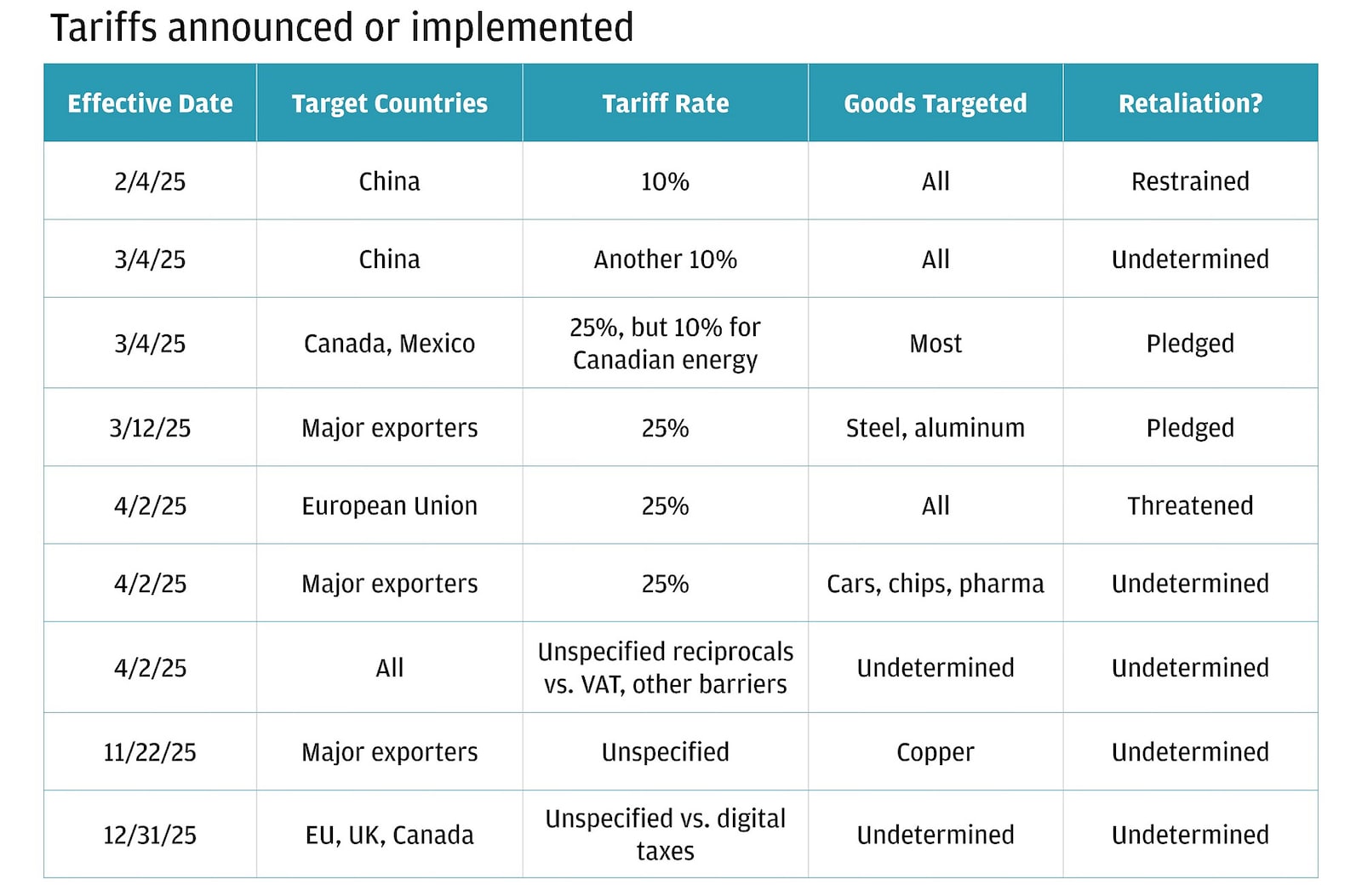

Tariffs stayed center stage in February, with the Trump administration proposing reciprocal tariffs on key trading partners. The aim seems to be establishing better balance in U.S. trade relations on a country-by-country basis, customizing import taxes to address not only tariffs imposed on imports from the U.S. but other barriers as well, like subsidies and value-added taxes.

It's important to acknowledge that many of the proposed elements of U.S. trade policy have yet to be implemented – the below table is helpful in seeing where things stand.

Tracking Trump’s trade actions

Negotiations between the U.S. and its trading partners could lead to different outcomes in the months ahead, and we’ll continue to monitor the developments. For now, investors should acknowledge that headlines could stoke volatility. And for what it’s worth, the initial market reaction to February’s tariff talk implied a degree of relief – after all, measures like reciprocal tariffs might be less impactful to economic growth and inflation than the flat 10% tariff on all imports discussed on the campaign trail.

Europe: 2025’s “Comeback Kid?”

The outperformance of European equities over their U.S. peers so far year-to-date represents a reversal of the momentum seen over the past couple of years. Potential for less-hawkish-than-feared U.S. trade policy is just one piece of the puzzle. The February news flow also featured rising hopes of a potential ceasefire in Ukraine, contributing an additional degree of optimism. With Europe’s equity market valuations having entered the year at low levels, the market was ripe for the rerating that underpinned February’s 3.7% gain.

Beyond the sentiment relief, investors latched onto positive earnings developments. Concerns around economic growth prospects and consumer demand – both domestically and in China – have been weighing on European earnings expectations, but the latest reporting season suggested that things may be turning around. A handful of notable companies in the technology, financials and luxury sectors delivered results above expectations, and broad-market future earnings expectations have been edging higher.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Questions remain, but softer U.S. trade policy posturing, potential for a ceasefire and/or a continued earnings recover could continue to support Europe’s recent rally. As for us, an actively managed approach to identifying the standout opportunities that can power through the uncertainties seems prudent from here.

Uncertainty is weighing on consumer sentiment

Before we wrap up, we would be remiss not to address the mixed bag of U.S. economic data released throughout February. Inflation data showed a larger-than-expected increase in economy-wide prices versus the prior month and prior year, which supports the case for the Federal Reserve to hold its policy rate steady coming out of its next meeting.

We still expect the Fed to deliver a couple of rate cuts later this year, but consumer expectations for inflation over the long term are worth monitoring. The University of Michigan’s latest consumer sentiment survey data showed that they moved higher in February, while overall confidence faltered – a sign that consumers might be feeling the pinch of policy uncertainties. This dip in consumer confidence could ultimately emerge as a headwind for consumer spending and economic growth, but we’re not seeing convincing signs that that’s the case yet.

Indeed, the resilience of consumption has supported corporate profits, with the S&P 500 looking likely to close its latest reporting season with roughly 18% year-over-year earnings growth on the books for the fourth quarter of 2024. As we work through separating the signal from the noise, we’re encouraged by this fundamental strength even as broader economic concerns persist.

Call it cautious optimism: We still see opportunities to capitalize on strong corporate performance. As investors pursue those opportunities, we encourage them to keep portfolio diversification in focus. February performance demonstrated that bonds can offset bumps in stock market performance, especially when growth concerns bubble up.

Final thoughts – and a bonus reflection on where we’ve been

As the calendar turns to March (already?), we can’t help but reflect on everything that’s happened over the past five years. The world shut down amid a once-in-a-lifetime pandemic, U.S. unemployment hit its highest level on record, inflation surged to a four-decade high, central banks pursued some of their most aggressive rate hiking campaigns in history to fight it, global armed conflict rose to an 80-plus-year high and various elections around the world brought plenty of drama.

In short, we’ve been through a lot since 2020. And still, over that stretch, the S&P 500 and MSCI World equity indices have returned nearly 100% and 120%, respectively; a passive blend of 60% global stocks and 40% global bonds is up 45%.

Uncertainty may be the clearest theme in 2025 so far, but don’t let it derail your plan. Remember that diversification and time in the market tend to reward investors, regardless of what comes their way.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

Head of Investment Strategy, J.P. Morgan Wealth Management