How a new Trump Account can fit into a long-term investing plan for your child

Editorial staff, J.P. Morgan Wealth Management

- A Trump Account is a type of individual, tax-advantaged investment account for U.S. children under age 18 who have a valid Social Security number.

- Babies born between January 1, 2025, and December 31, 2028, who are U.S. citizens with a valid Social Security number are also eligible for a $1,000 government “seed” deposit in their Trump Account.

- Trump Accounts allow for contributions of up to $5,000 per year (indexed after 2027) during the growth period, and contributions can be made by parents, family, other individuals and employers.

- Trump Accounts can be utilized as part of a broader investment strategy that includes other types of accounts, such as 529 plans, IRAs, savings accounts and custodial accounts.

If you’re a parent or guardian of a child under age 18, the U.S. government has a new investment account that may fit into your child’s financial plan. Trump Accounts are individual, tax-advantaged investment accounts for children under age 18 who have a valid Social Security number (SSN). You can elect to open a Trump Account for your child through IRS Form 4547Opens overlay or via TrumpAccounts.govOpens overlay. The accounts became available to fund and manage starting in July 2026.

Additionally, children born between January 1, 2025, and December 31, 2028, who are U.S. citizens with a valid SSN, are eligible to receive a $1,000 government seed deposit in their Trump Account to help them get started with lifelong savings.

Once the Trump Account is open, you, family, other individuals and even employers can contribute to the account up to an annual total of $5,000 (indexed after 2027) during the growth period (defined as ending December 31 of the year before the child turns 18), though contributions are not required.

If you're wondering how to integrate a Trump Account into a long-term investing plan for your child, here are some things you need to know.

Using a Trump Account to invest for your child’s future

Passed in July 2025, the One Big Beautiful Bill Act created Invest America Accounts (more commonly known as Trump Accounts), a new type of tax-advantaged investment account for U.S. children under age 18 with a valid SSN. You may be able to open a Trump Account for your child – the owner and beneficiary of the account – now through December 31 of the year before they turn 18. Trump Accounts became available to fund and manage starting in July 2026. To elect to open the account, you can fill out IRS Form 4547Opens overlay and file it with your tax return, or you can open it via TrumpAccounts.govOpens overlay.

While the account will be set up in your child’s name (they are the owner and beneficiary), you will be the custodian until your child assumes control of the account. At that point, the child will gain ownership and access to the account, and it will, generally speaking, follow the same rules as a traditional IRA.

The Trump Account is opened at a financial institution of the government’s choice, but you can transfer the money in your child’s Trump Account to another financial institution during the growth period. Trustee-to-trustee transfers (Trump Account “rollovers”) are allowed during the growth period when they are made to another Trump Account for the same beneficiary. The rollover must be a full transfer – partial transfers are not permitted, and only one funded Trump Account may be open for a child at any time. The trustee-to-trustee transfer is a non-taxable event.

How the money in your child’s Trump Account may grow over time

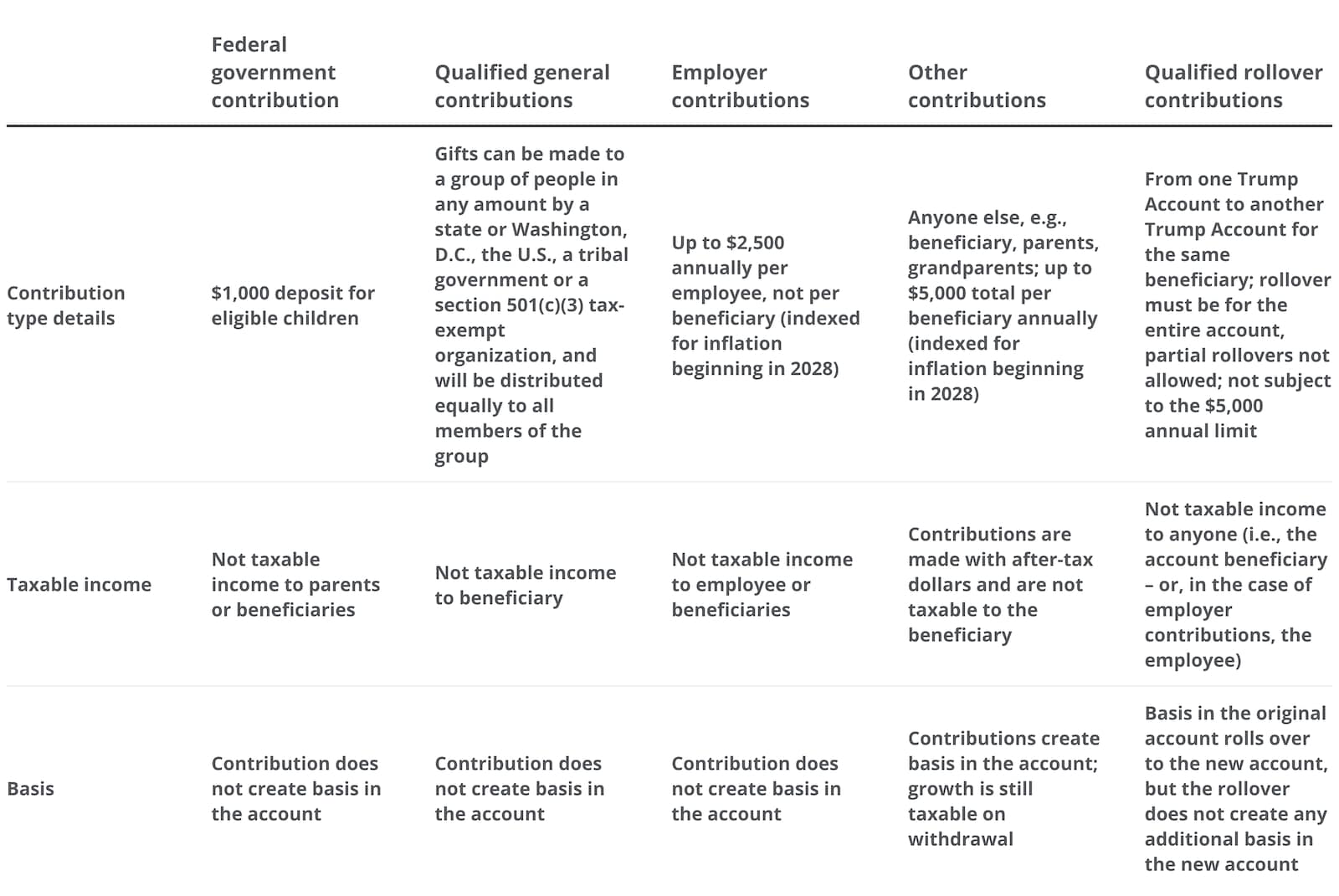

Trump Accounts can be funded during the growth period through annual contributions of up to $5,000 (indexed after 2027) from parents, family, other individuals and even employers.

Employers may contribute up to $2,500 annually (indexed after 2027) per employee (not per Trump Account) during the growth period. This amount counts against the $5,000 annual contribution limit but is not considered income to the employee.

Additionally, eligible children in certain ZIP codes or who meet other stipulated criteria may qualify for contributions from philanthropic donors or foundations, such as from the Michael & Susan Dell Foundation. These contributions are called “qualified general contributions” and are not counted against the $5,000 limit.

During the growth period, the money in your child’s Trump Account must be invested in broad U.S. equity index funds – such as mutual funds or exchange-traded funds (ETFs) that track a U.S. stock index, such as the S&P 500. The funds can't have leverage, and annual fees and expenses must be capped at 0.1%. Subject to limited exceptions for cash, no other investments are permitted, including sector-specific funds.

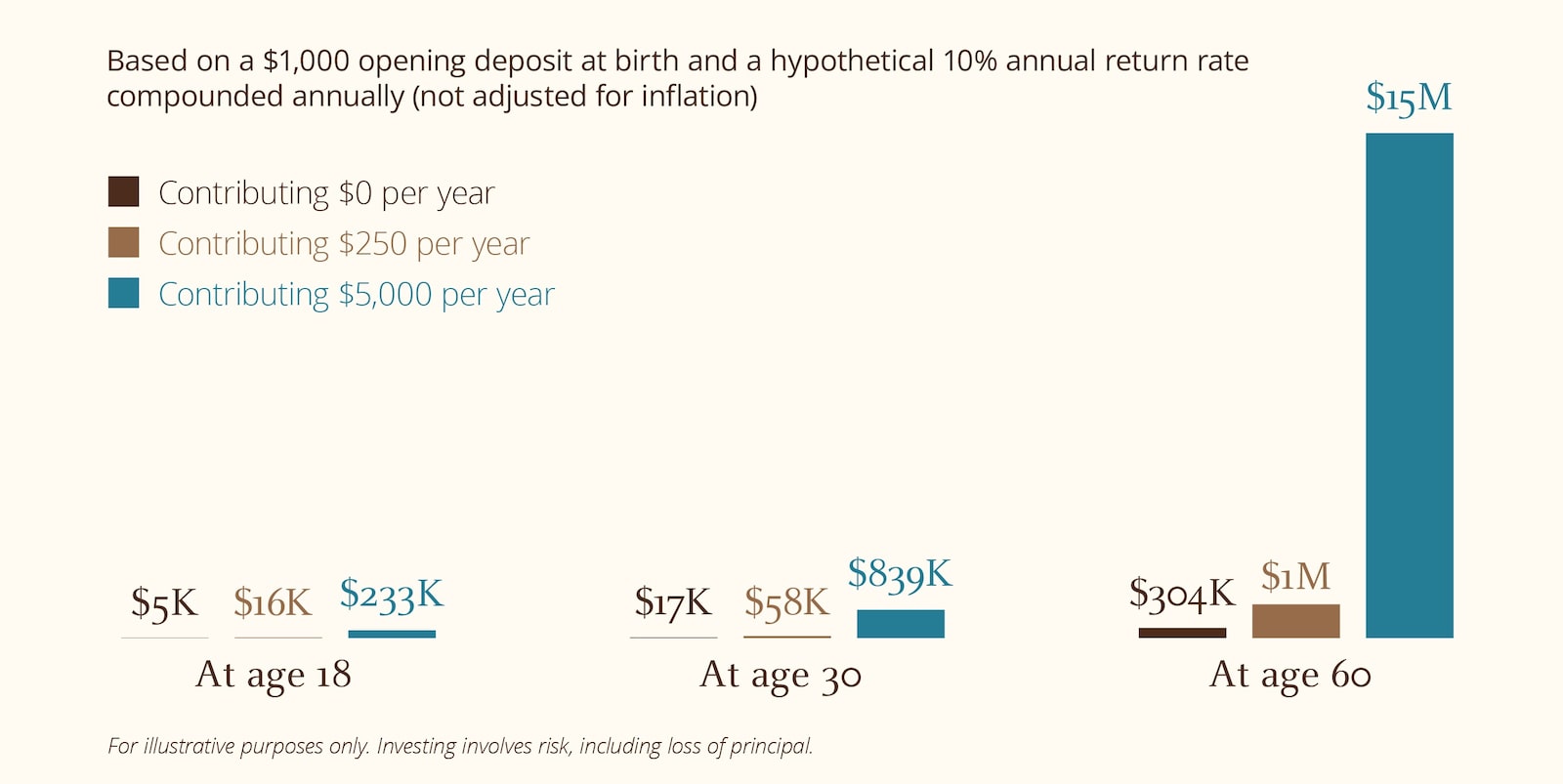

With time, an initial $1,000 opening deposit at birth could grow to a meaningful amount. Below you can see hypothetical situations based on different ages and contribution amounts. (Actual returns will vary based on market performance.)

Projected Growth of a Trump Account (Hypothetical)

The above is a hypothetical example for illustrative purposes only and should not be relied upon in making an investment decision. These examples do not reflect actual or future performance results of any specific vehicle, and are based solely on the hypothetical illustration cited. Assumed starting amount is $1,000 at birth. Assumed hypothetical annual rate of return is 10%, not adjusted for inflation, and compounded annually. Investing involves risk, including loss of principal.

Distribution rules for Trump Accounts

The primary purpose of a Trump Account is to give children a head start on their financial future. During the growth period, distributions generally are not allowed. After the growth period ends, Trump Accounts generally follow the distribution rules of traditional IRAs. That means that after the growth period ends and until the beneficiary (your child) is 59½ years old, distributions incur a 10% early withdrawal tax unless the distribution qualifies for an IRS exception such as college tuition, a first-time home purchase, or the birth or adoption of a child (see below). After age 59½, distributions are not subject to the early withdrawal tax.

Distributions that qualify for an IRS exception include, but are not limited to:

- Education: College tuition and other “qualified higher education expenses”

- Home: Buying, building or reconstruction expenses for “qualified first-time homebuyers,” up to $10,000 (lifetime limit)

- Birth or adoption of a child: Distributions of up to $5,000 per child for qualified birth or adoption expenses

- Death: Distributions after the death of the account owner

- Disability: Distributions due to the account owner suffering a total and permanent disability

- Disaster recovery: Distributions of up to $22,000 for qualifying individuals who suffer an economic loss due to a federally declared disaster where they live

- Domestic abuse: Distributions of up to $10,500 (as adjusted) or 50% of the account (whichever is less) to victims who suffer domestic abuse from a spouse or domestic partner

- Personal emergency: One distribution per calendar year of up to $1,000 or the amount of the account balance that exceeds $1,000 (whichever is less) for costs related to a personal or family emergency

- Medical expenses: Distributions equal to the amount of unreimbursed medical expenses (that would qualify for a deduction) that an account owner has (which are greater than 7.5% of their adjusted gross income) and/or certain health insurance premiums during a period of unemployment

- Military: Certain distributions to qualified military reservists who are called to active duty

These exceptions may be subject to additional and sometimes complex requirements; you should consult IRS Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs)Opens overlay or your tax professional to learn more about these exceptions, and with any questions you may have.

Tax treatment of Trump accounts

Contributions to a Trump Account during the growth period from the federal government, qualified general contributions and employer contributions do not create basis in the account and are taxable at withdrawal. Contributions from parents, family and other individuals create basis in the account, meaning they are not taxable at withdrawal, but any account growth will be taxable at withdrawal.

After the growth period, a Trump Account is generally subject to traditional IRA rules regarding contributions, withdrawals and taxation, including the potential for an early withdrawal tax before age 59½ unless an IRS exception applies.

Tax treatment of Trump Account contributions

Learn how Trump Accounts can support your child’s future

Build lasting financial security for your child with a tax-advantaged Trump Account and help them save for retirement and other future goals.

Other investment and savings accounts to consider opening for your child

While Trump Accounts can help set a child up for future financial security, they can play just one role in your child’s financial plan. Here are a few other common account types that you might consider as part of your child’s long-term investment strategy.

529 plans and other education savings accounts

A 529 plan is a state-sponsored, tax-advantaged investment account designed to help families save for their children’s future education costs. Compared to Trump Accounts, the main advantage of 529s is the tax-free withdrawal of earnings used to cover qualified education expenses. These plans also allow for larger contributions than Trump Accounts. Rather than an annual contribution limit, contributions to 529s are restricted by state-set lifetime maximums per beneficiary. Other factors that impose practical (but not legal) limits on contributions are the federal annual gift tax exclusion limit and state contribution deduction limits (when applicable). Because 529 accounts are usually owned by a parent or grandparent, they have less of an impact on financial aid qualification than a Trump Account, which counts as the child’s asset.

In addition to 529 plans, you may consider other education savings accounts like Coverdell accounts, which have very low annual contribution limits as well as income limits. You can use multiple accounts to save for your child’s future education, so it’s important to consider them all.

Custodial accounts

Custodial accounts can either be bank accounts or investment accounts that you can open and manage for a minor beneficiary, like your child. An adult is the custodian and manages the investments, but the assets legally belong to the child and must be managed and used for the minor child’s benefit. Custodial accounts are governed by the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA) and are commonly used to save for a child’s future. Control of the account passes to the child when they reach the age of majority, typically 18 or 21 – although under some circumstances it can be up to age 25 – depending on the state.

Custodial accounts differ from Trump Accounts in several ways. There is no government seed deposit into a custodial account. However, custodial accounts allow for wider investment options. They also don’t have annual contribution limits or an early withdrawal tax on distributions taken before 59½, though contributions to custodial accounts are subject to gift tax rules. Earnings are generally taxed annually, and if the child has enough unearned income, “kiddie tax” rules may apply, meaning part of the child’s unearned income is taxed at the parents’ higher marginal rate. Depending on how much the account earns, the child may also need to file a tax return. The custodian is responsible for ensuring proper tax reporting.

Savings accounts

A savings account is a type of deposit account where you can accumulate money for your child. While the other accounts on this list are accounts where the money belongs to your child, the money you move to a savings account that is in your name still belongs to you. The money you deposit in a Trump Account, custodial account or other education savings account may be a gift to your child, while the money in the savings account is not.

You can typically contribute as much as you want and withdraw funds whenever you want, though some banks have limits on how many withdrawals or transfers can be made per month to and from a savings account. You may not want to save more money in a savings account than is covered by FDIC (Federal Deposit Insurance Corporation) insurance – typically up to $250,000 per person, per institution. However, you can have accounts at multiple banking institutions.

Traditional and Roth IRAs

Both traditional and Roth IRAs can be opened for a minor who has earned income. A parent or guardian may need to open a custodial IRA on the child's behalf until the child reaches the age of majority in their state of residence. The child can contribute only up to the amount they earn in a year or the annual IRS contribution limit – whichever is less.

Traditional IRAs

Anyone with earned income can contribute to their traditional IRA. There are no annual income limits on contributions, though income may affect tax deductibility. Contributions are generally tax-deductible, and earnings grow on a tax-deferred basis until withdrawn. Deductibility may be limited if the IRA owner (or their spouse) is covered by a retirement plan at work and their income exceeds certain levels. Deductible contributions and any earnings are taxed as ordinary income upon withdrawal.

Unlike a Trump Account, which has restrictions on withdrawals during the growth period, withdrawals from a traditional IRA may be taken at any time for any reason; however, early withdrawals (prior to age 59½) are generally subject to a 10% early withdrawal tax unless certain exceptions apply (as described above).

Roth IRAs

Like a traditional IRA, individuals with earned income may be able to contribute to a Roth IRA, but contributions are potentially limited based on filing status and income. Contributions are not tax-deductible; however, earnings grow tax-deferred and “qualified distributions” (as defined by the Internal Revenue Code) are exempt from federal taxes.

Contributions to a Roth IRA can be withdrawn at any time without tax or penalty. A qualified distribution – one that is both tax-free and avoids the 10% early withdrawal tax – must meet these two requirements (per Internal Revenue Code § 408A and IRS Publication 590-B):

- Five-year holding period: The distribution occurs after the five-tax-year period beginning January 1 of the year for which the first contribution was made to a Roth IRA set up for your benefit, and

- Qualifying event: One of the following must apply:

- You are age 59½ or older;

- You have a total and permanent disability;

- The distribution is made to your beneficiary or estate after your death; or

- The distribution is used for a qualified first-time home purchase (up to a $10,000 lifetime limit).

If you receive a distribution from a Roth IRA that isn't a qualified distribution, part of it may be taxable and may also be subject to the 10% early withdrawal tax (unless an exception applies). Rollovers and conversions to Roth IRAs present additional and sometimes complex requirements.

A Roth IRA may be particularly attractive for a child because children typically have little or no taxable income. This means they forgo the minimal tax benefit from a deductible traditional IRA contribution. A Roth IRA, by contrast, allows decades of tax-free growth, and the five-year funding period clock starts early – potentially enabling tax-free qualified distributions well before retirement.

For more information on IRA contribution rules, refer to IRS Publication 590-A Contributions to Individual Retirement Arrangements (IRAs)Opens overlay. For distribution rules, refer to IRS Publication 590-BOpens overlay. Contact your legal or tax professional(s) with any questions you may have.

Building a long-term investment strategy with a Trump Account

As you plan for your family’s future, it’s worth considering how a Trump Account might fit into the broader investment strategy for your child or children. If you’ve given birth to a child since the start of 2025 or have a child by the end of 2028, they qualify for the $1,000 federal seed deposit as long as they are a U.S. citizen and have a valid SSN. From there, you can simply let the $1,000 seed money grow over time, or you can choose to contribute up to $5,000 per year (indexed after 2027) during the growth period.

The right contribution strategy for your unique situation depends not only on the goals you have for your child’s financial future but also on how a Trump Account might fit with other accounts you have in place. For example, do you want your contributions to jump-start a lifetime of compound growth and tax-deferred savings for your child’s retirement? Cover incidental costs encountered in life? Help fund a down payment on their first house? Understanding the end goal can help you target a specific balance and time frame, and then decide the right way to manage a Trump Account or other investment or savings account for your child.

It should be noted that while you are helping set your child up for the benefits of long-term investing, they may take distributions for any purpose under traditional IRA rules after assuming control of the account after the growth period.

The bottom line

Trump Accounts offer parents another way to save for their children’s future. While Trump Accounts aren’t necessarily the best option for every goal, such as paying for higher education expenses (which might be better taken care of by a 529 plan), they can be a beneficial part of a larger, long-term investment plan.

With time, the money in a Trump Account could grow to a meaningful amount. Further, the accounts offer distribution flexibility like with a traditional IRA after the growth period, giving your children a potential financial cushion for various life events.

Frequently asked questions about Trump Accounts

During the growth period, the money stays invested and distributions are generally not allowed. Once the growth period ends and your child assumes control of the account, they can take a distribution for any purpose (subject to ordinary income tax). They may be able to tap the funds without paying an early withdrawal tax if the money is used for meaningful life milestones recognized by the IRS, like paying for college tuition, buying a first home or welcoming a child through birth or adoption; otherwise, before age 59½, a 10% early withdrawal tax applies. After age 59½, distributions are only subject to ordinary income tax.

Yes, you can open both a Trump Account and a custodial account for the same child. They are not mutually exclusive and have different pros and cons. For example, your investment choices are far broader in a custodial account, and you can take withdrawals from custodial accounts while your child is a minor as long as the money is used for their benefit. Conversely, Trump Accounts offer tax-deferred investment growth, while earnings in custodial accounts are taxed on an annual basis.

The money in a Trump Account is generally not accessible until after the end of the growth period, defined as December 31 of the year before the child turns 18.

Yes, the Trump Accounts: Official App launched on May 28, 2026, and is available in app stores. You can also download the app from TrumpAccounts.gov. You must complete Form 4547 before you can sign up for the app. Once the form is complete, you can sign up with the email address you used to sign up for a Trump Account. Once you sign up with your email, a password and your phone number, you can sign up for notifications to get updates on your child’s Trump Account. The Treasury Department also indicated that parents who signed up for a Trump Account for their children will receive emails with steps for setting up the app.

Keep an eye out for emails from this address: no-reply@TrumpAccounts.Treasury.gov.

Invest your way

Not working with us yet? Find a J.P. Morgan Advisor or explore ways to invest online.

Editorial staff, J.P. Morgan Wealth Management