A shortage of supply: The housing market explained

Equity markets remain resilient, despite multiple challenges

Artificial intelligence (AI) optimism drove markets this week, keeping the S&P 500 (+1.2%) and Nasdaq 100 (+1.8%) afloat despite regional bank stress, trade jitters and the U.S. government shutdown.

- AI isn’t just booming – it’s reshaping the entire economy. TSMC’s record Q3 earnings and increased AI capital expenditure guidance signal strong demand, while ASML’s robust orders highlight upstream strength in the semiconductor supply chain. Broadcom’s multiyear deal with OpenAI shows how AI is expanding beyond graphics processing units into new hardware and enterprise solutions. Reflecting this momentum, the International Monetary Fund sees AI investment as a key driver for the U.S. economy, boosting investor confidence in a sustainable growth cycle.

- The cracks in credit are showing up in regional banks – not the giants. Financials was the worst-performing sector this week after Zions Bancorp and Western Alliance disclosed credit issues tied to loan fraud misrepresentation. These disclosures have heightened concerns about deteriorating borrower creditworthiness, especially following recent bankruptcies at First Brands and Tricolor Holdings. Investors aren’t willing to wait and see if cracks continue to emerge elsewhere, and they are reducing exposure to regional banks, which tend to have greater exposure to subprime loans than the largest banks (Global Systematically Important Banks).

- Despite hints of negotiation, U.S.-China tensions are keeping markets on edge. Markets were unsettled early in the week by renewed U.S.-China tariff threats, as China’s new export controls on rare earths triggered global pushback. While conciliatory statements from both sides hinted at a willingness to negotiate, uncertainty persists ahead of a potential meeting between President Trump and President Xi at the Asia-Pacific Economic Cooperation (APEC) Summit.

- The U.S. government shutdown is entering its 17th day. The parties are fixed in position, there are no meaningful negotiations underway and the impasse looks set to stretch into at least late October.

Below, we discuss the state of the housing market.

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Deciphering the housing market

If buyers are on the sidelines, why aren’t home prices falling? It’s a top-of-mind question – and for good reason. The U.S. housing market is sending mixed signals: Few people are buying homes, yet prices remain stubbornly high.

The heart of the housing market’s resilience isn’t surging demand – it’s a shortage of supply

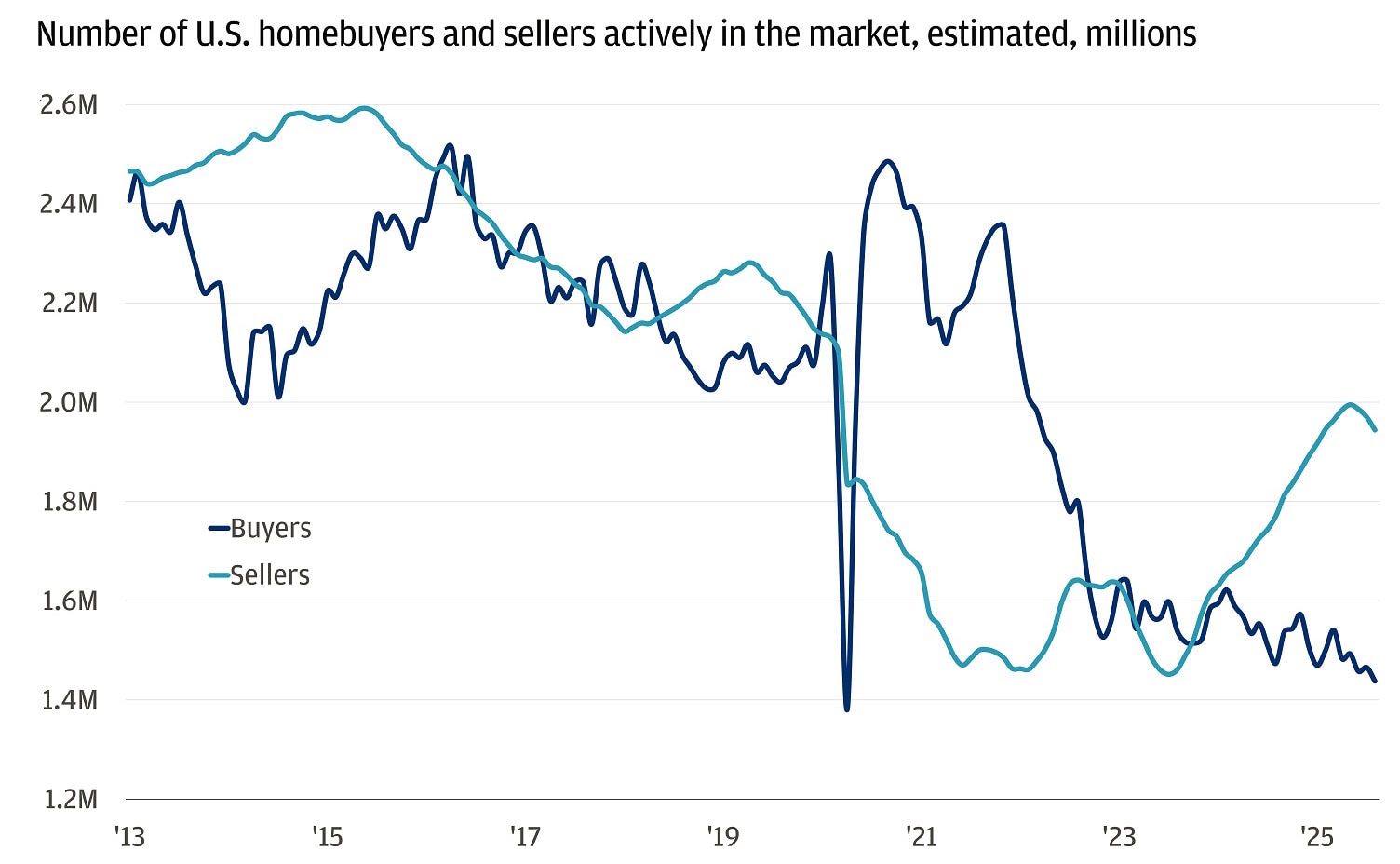

After two years of elevated mortgage rates, buyers have largely been on pause. Pending home sales, a key forward-looking indicator, have rebounded from their 2024 lows, with August posting a 4% monthly increase and September showing an even larger gain. But context matters: These upticks come off multi-decade lows, and overall activity remains well below the pandemic-era boom.

Mortgage rates have eased into the low-6% range, the lowest in about a year, but affordability is still a major hurdle. As of early 2025, prices are up 60% nationwide since 2019 and still rising at a rate of 3.9% year-over-year, according to the S&P CoreLogic Case-Shiller U.S. National Home Price Index. Even with rates off their highs, the monthly payment for a median-priced home is still out of reach for many households. For context, before the pandemic, the median home price was about $260,000, and the average 30-year mortgage rate was 3.8%, resulting in a monthly payment of roughly $1,000. Today, the median price has climbed to around $420,000, and rates are closer to 6.4%, pushing the monthly payment above $2,100. In other words, buying a typical home now costs more than twice as much per month as it did before the pandemic.

Homebuyers remain on pause

So, with demand so subdued, why aren’t prices correcting?

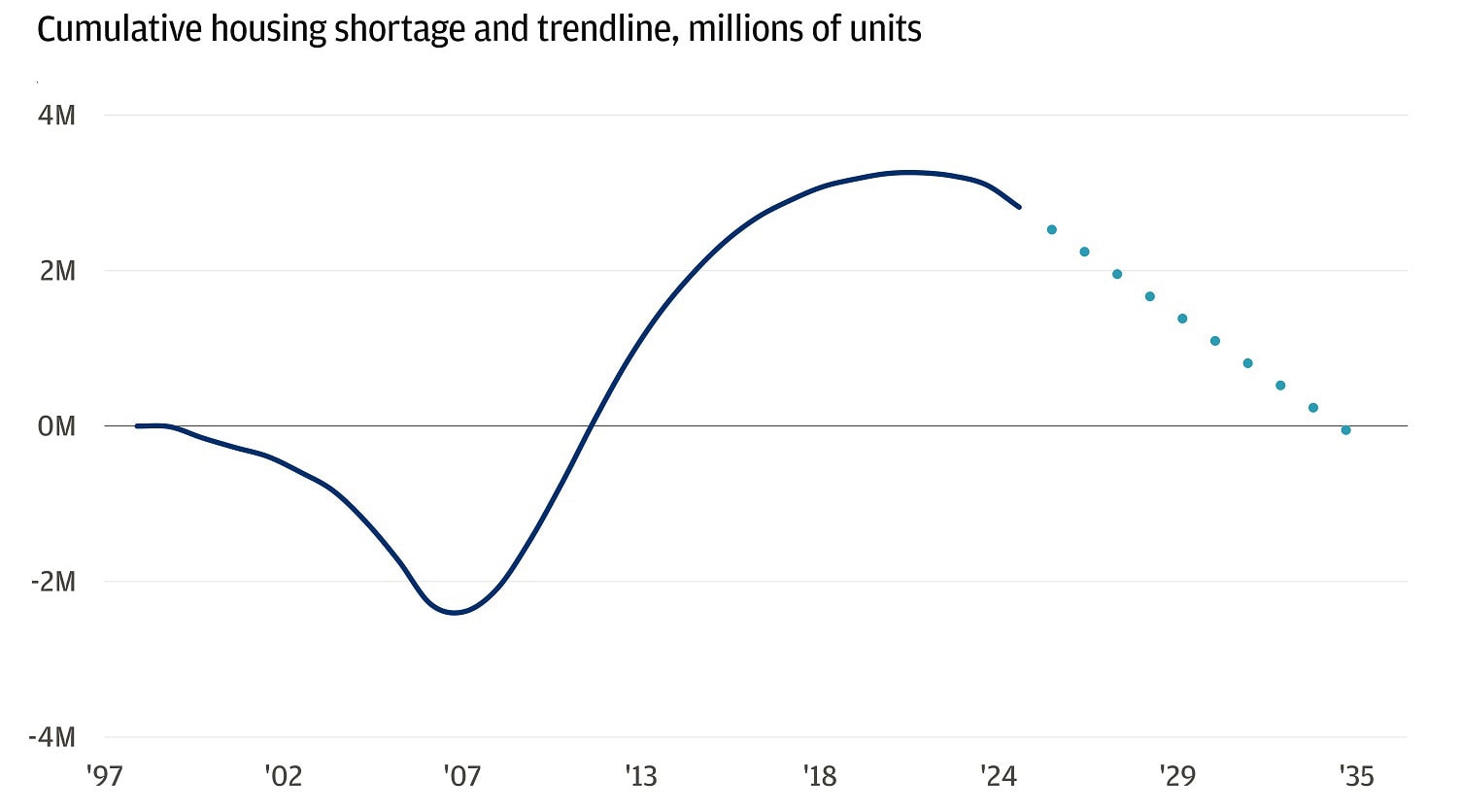

The answer lies in a persistent supply squeeze. About half of current U.S. mortgage borrowers are still enjoying sub-4% rates, and about 80% are paying under 6%, creating a “locked-in” effect – there’s little incentive to sell and take on a higher payment, keeping existing home inventory at historic lows. We estimate the current housing shortage at approximately 2.8 million units and believe it could take around 10 years to resolve. This figure is likely conservative, as it only reflects the physical shortfall and doesn’t account for the fact that many households haven’t been formed due to discouragement – such as individuals remaining in their parents’ homes longer. It’s important to note that the shortage isn’t uniform across the country; it’s most acute in coastal cities and much less severe in the middle of America.

Current housing shortage of ~2.8 million could take about 10 years to resolve

Compounding this is the legacy of underbuilding, especially in the years following the Global Financial Crisis. The U.S. has faced a structural housing deficit for over a decade. While new construction has picked up, it’s not enough to close the gap.

Even as supply is starting to outpace demand at the margin, the backlog is so large that it will take years to unwind. The result: a market where scarcity, not exuberance, is keeping prices elevated.

While it’s true that easing rates can help at the margin, they’re not a game-changer

As rates have started to dip, we’ve seen a modest uptick in contract activity. But unless rates fall dramatically, affordability will likely remain a challenge for most buyers.

There’s also the paradox of lower rates. If rates were to plunge (in the absence of a recession), it could actually reignite demand and push prices even higher, as more buyers chase limited inventory. In other words, lower rates might not improve affordability – they could just create bidding wars.

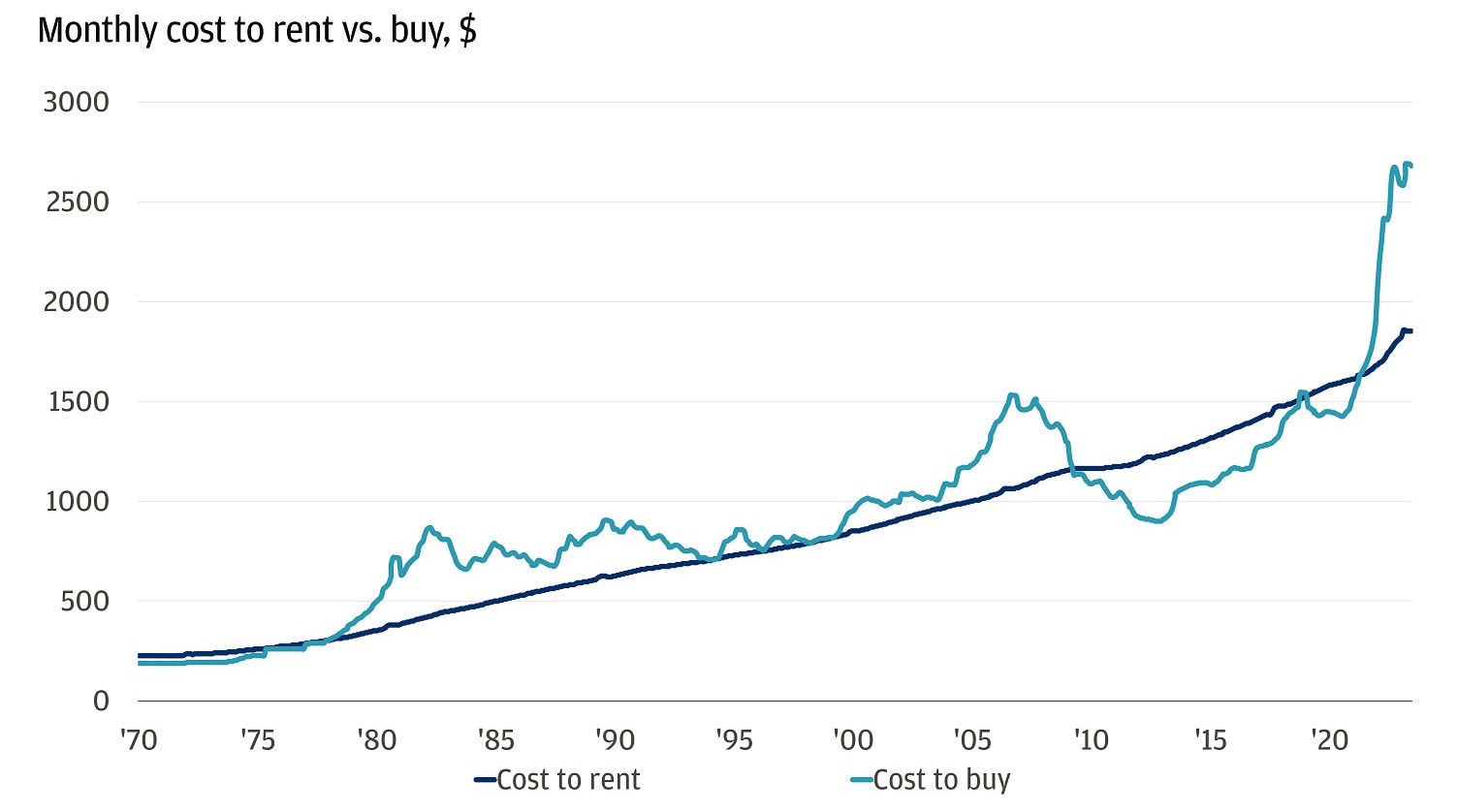

But we still see an opportunity. All of this sets the stage for what we see as the most attractive opportunity in U.S. housing: the rental market. Today, the cost of owning a home is roughly 40% higher than renting, and the average American needs more than eight years to save for a down payment, both of which drive a preference for renting, with median apartment rents relative to median weekly wages now falling below where they were pre-pandemic.

The cost of owning a home is roughly 40% higher than the cost of renting one in the U.S.

As homeownership becomes less attainable, rental demand is only strengthening. This affordability crisis has created a significant opportunity in single-family rental (SFR) assets, where resilient demand and demographic trends support long-term growth.

Is declining homeownership concerning?

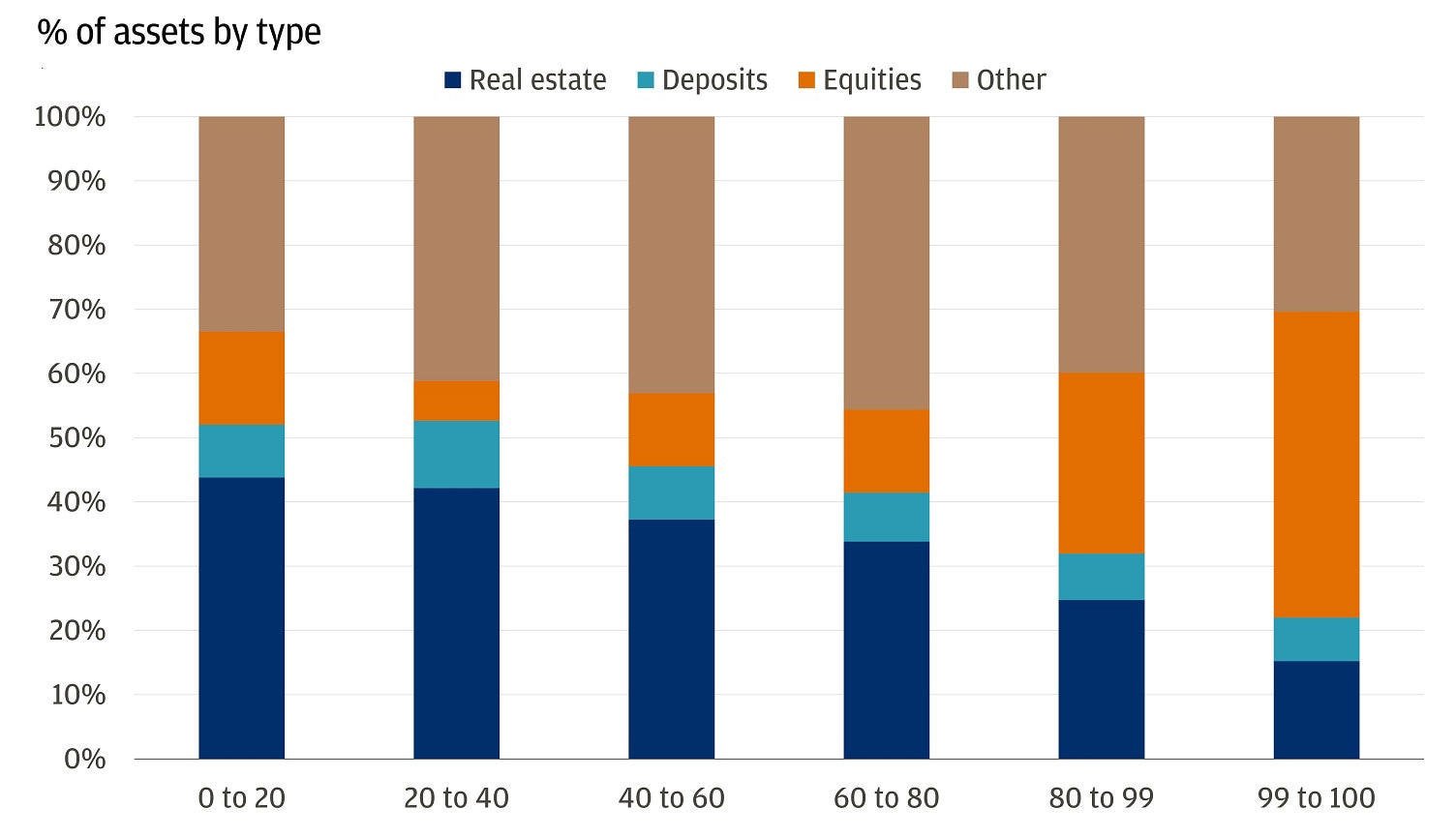

While falling homeownership rates might seem worrisome at first glance, the broader economic impact is far less significant than many might assume. In fact, global data show a negative correlation between homeownership rates and GDP per capita: Some of the world’s wealthiest countries have lower rates of homeownership, suggesting that high ownership isn’t a prerequisite for economic prosperity.

The wealth effect of homeownership is also less compelling than it once was. The current imbalance in the housing market has led to declining homeownership rates for all age groups under 70, while rates have actually increased for those over 70 – the ownership curve has steepened. While homeownership has traditionally been viewed as a cornerstone of wealth-building, history tells a different story. Over the past 15 years, U.S. house prices have consistently lagged the equity market, making housing a relatively inefficient way to build wealth compared to other investments.

Equities a much larger share of wealth for the top 1% of incomes

This shift further reinforces our constructive view on rentals. As homeownership becomes less attainable and less central to wealth creation, the rental market stands out as a resilient and attractive opportunity for investors. With durable demand, favorable demographic trends and the potential for strong risk-adjusted returns, rental assets – particularly single-family rentals – are well-positioned to benefit.

Overall, the decline in homeownership isn’t a problem for the economy or for investors because rent remains affordable, allowing households to avoid undue financial strain. This is a sign of changing preferences and market realities, and it highlights the growing appeal of rental assets as a component of a today’s investment strategy.

All market and economic data as of 10/17/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist