3 top-of-mind lessons in the current market environment

Market update

You might think that renewed tariff fears and the One Big Beautiful Bill Act (OBBBA) would have caused some volatility, but you’d be wrong. The S&P 500 reached new highs, U.S. Treasury yields stayed flat, Federal Reserve (Fed) cut expectations held steady and the U.S. Dollar (USD) gained slightly against major peers.

Even after President Donald Trump announced higher blanket tariffs at 15% to 20% and a potential 35% tariff rate for Canadian goods, United States-Mexico-Canada Agreement (USMCA) goods remaining exempt, markets stayed relatively muted; futures are down only about 60 basis points as of 5:30 a.m. ET.

Amid broader tariff announcements, copper tariffs serve as a good reminder of how markets are digesting the news: A 50% increase announcement for August 1 led to a 13% spike in prices before a 3.5% pullback. The U.S. imports about 45% of its copper and lacks the capacity to mine and smelt more. So why isn’t the impact larger? The move was somewhat anticipated, U.S. importers built ample inventory and expectations are for a resolution at a lower rate. Investors aren’t buying the 50% tariff rate. The administration’s aim is to encourage U.S. copper production. While not feasible now, it could be in three to five years with investment and faster permits.

On the flip side, the OBBBA introduces $4.5 trillion in tax cuts and $1.2 trillion in spending cuts while boosting military and immigration enforcement funding. Initially, fears arose about the impact on U.S. debt and the fiscal deficit, with spending cuts seen as insufficient to offset the accretive effect. However, it’s not as dire as it seems. Although the OBBBA raises the deficit, the $3.4 trillion estimate might be overstated. The Congressional Budget Office (CBO) estimate doesn’t account for tariff revenues, expected to mitigate some fiscal challenges. Our estimates suggest a modest reduction in the deficit (excluding interest servicing costs) as the likely combined net effect over time.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Our take: Investors are focusing on fundamentals over noise. The tariff headlines seem like more bark than bite and markets have become desensitized to the flurry of announcements. While the latest tariff news suggests an effective rate of 15% to 20%, we continue to believe some threats won’t stick. Our base case remains that effective tariff rates will fall between 10% to 15%. We expect a modest drag on growth, but investors believe the administration is determined to make deals. After all, this could be the final stage of negotiation. Whether these rates stick or not, we will at least gain clarity either way.

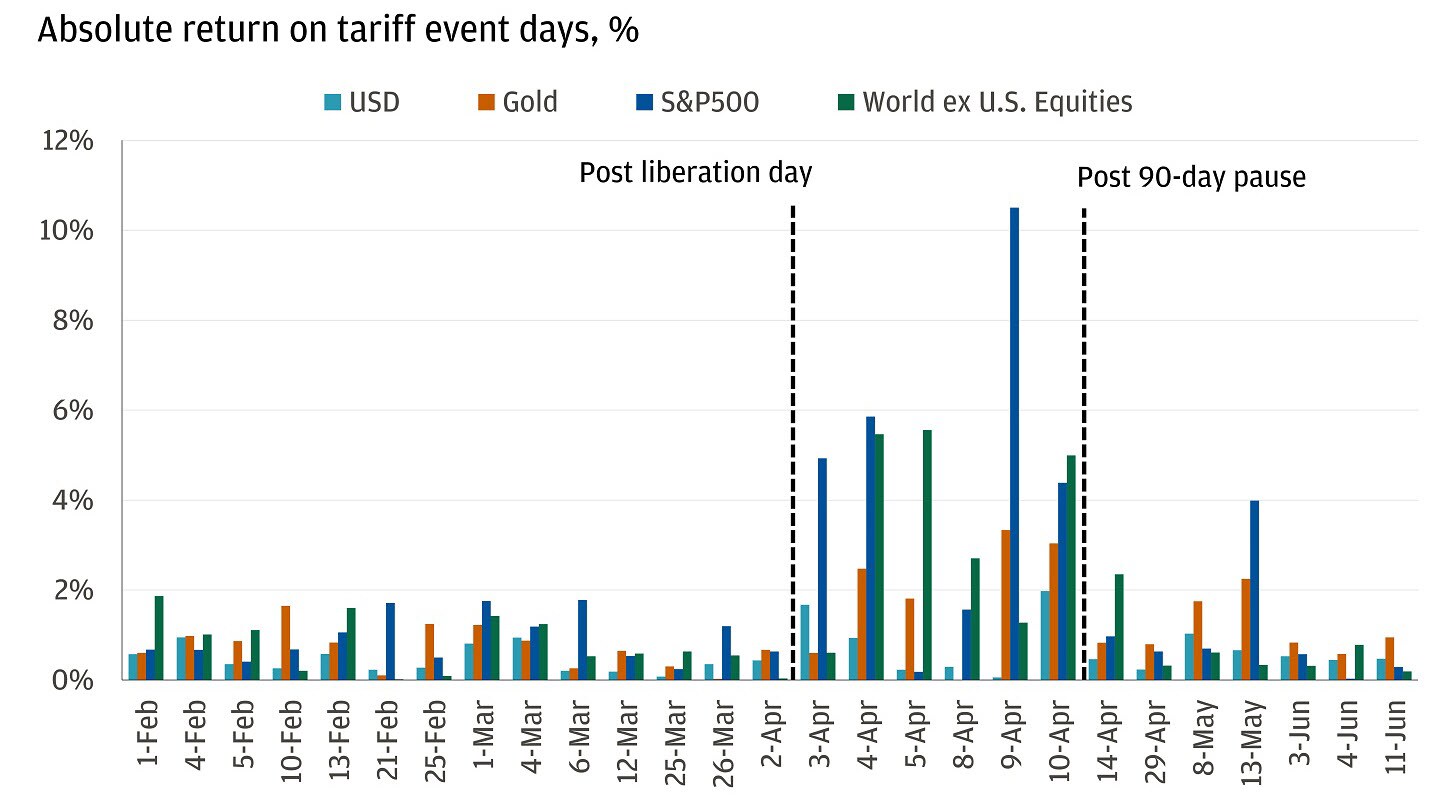

Markets have become desensitized to tariff announcements

Don’t get us wrong – there could be tail risks ahead. But the Fed is showing more willingness to ease financial conditions without significant labor market deterioration as long as inflation expectations remain anchored. A renewed rate cutting cycle without a recession would be a bullish outcome.

Investors are already looking ahead to Q2 2025 earnings season, which is shaping up to be stronger than expected. Some call it complacency, but if earnings come in like we expect them to it will become fact. And soon, expectations will shift to 2026.

Sometimes, all we need is to step back and gain perspective. Don’t miss the forest for the trees. To that end, we take a closer look at three lessons we’re keeping top-of-mind in the current market environment.

Spotlight

Lesson 1: Don’t get caught up in short-term headlines and sensationalism

Despite industry doomsayers’ warnings, historical data reveals that investors who shifted from equities to bonds based on these predictions faced significant losses. Even during the COVID-19 selloff in March 2020, these losses did not reverse and the market’s subsequent rally underscored the advantages of staying invested amid apocalyptic forecasts.

It’s crucial to keep a long-term investment horizon. History shows that recessions and bear markets occur and listening to perpetual pessimists can be costly compared to a balanced approach. This year’s volatility is a case in point: During the worst of the downturn, consumer sentiment plunged to 52.2 from 74 at the end of 2024, market recession odds hit 65% and the S&P 500 dropped 19%. Just three months later, sentiment rose to 60.7, recession odds fell to 22% and the S&P 500 surged +25% from its April 8 lows, hitting four new all-time highs after recovering all losses by June 26.

Lesson 2: Invest in innovation to drive the next revolution, paving the way for future productivity and earnings growth

Artificial intelligence (AI) capital spending is surging among hyperscalers like Meta, Microsoft, Alphabet and Amazon – a bold move with inherent risks. That said, Nvidia’s data center revenues as a share of total market capital spending are projected to hit levels reminiscent of past tech booms and investors are eager to see hyperscaler free cash flow margins reflect the benefits of this spending. Meanwhile, equity analysts are adjusting expectations for slower earnings growth due to the depreciation of new AI infrastructure.

As we’ve also discussed in our 2025 Mid-Year Outlook, the AI theme holds immense potential to disrupt industries. While we remain vigilant for any signs of wavering commitment or impacts on company decisions, recent developments reinforce our confidence in AI’s transformative potential:

- AI adoption on the rise. Census Bureau data shows AI adoption and expectations have doubled in the past year, driving significant market shifts. This surge in AI technologies has propelled Nvidia to become the first company to reach a $4 trillion market cap, underscoring the transformative impact of AI.

- Growing role in software. Microsoft’s strategic layoffs of 15,000 employees and the declining rate of software engineering hires reflect a shift towards AI automation, aiming to boost productivity and reduce the need for coders. Meta CEO Mark Zuckerberg even noted that he expects AI to write most of the code for LLama research within the next 12 to 18 months, underscoring AI’s growing role in software development.

- Investments are ramping up globally. China plans to use 115,000 Nvidia AI chips for Gobi desert data centers despite U.S. restrictions. Meanwhile, Meta is pouring over a billion dollars into Superintelligence Labs, recruiting top talent from OpenAI, DeepMind and Apple to enhance its AI capabilities.

Overall, it seems companies are fearing getting left behind in the AI race and are willing to put money to work for this goal.

Lesson 3: Embrace U.S. tech growth, but ensure balanced exposure to global markets for a well-rounded strategy

U.S. exceptionalism was evident in the sustained outperformance of U.S. equities and the resilience of the U.S. Dollar. Since 2010, U.S. equities have thrived, fueled by USD strength, sector weight differences and superior within-sector performance driven by higher returns on assets and equity.

While undisputed, the next decade likely won’t mirror the last. In 2025, USD investors in European equities have seen a 24% rise year-to-date, outpacing the 5.9% gain in U.S. equities. This shift hints at a narrowing gap between U.S. and European equities and offers growth opportunities in both regions fueled by evolving currency dynamics.

Although the U.S. exceptionalism narrative may be shifting, the U.S. remains the destination of choice, with higher gross domestic product (GDP) growth, productivity and earning potential. Additionally, sector composition has evolved, with growth sectors like technology, communication services and consumer discretionary now making up about half of the S&P 500 – historically demanding higher multiples.

That’s not to say Europe lacks new catalysts or that the gap isn’t closing, bolstered by a weaker USD driven by cyclical convergence, global asset reallocation and increased FX-hedge ratios among foreign investors. Considering all of this, the start of 2025 should be a wake-up call – not signaling the end of U.S. exceptionalism, but a return to balanced portfolios. After all, an MSCI world allocation is 70% U.S. and 30% ex-U.S.

Reach out to a J.P. Morgan advisor for more on how these insights could affect your investing portfolio.

All market and economic data as of 07/11/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.