Is the DeepSeek drama a gamechanger for the AI trade?

J.P. Morgan Wealth Management

Market update

Tech-focused U.S. equities pulled back from all-time highs this week as tech and artificial intelligence (AI) names dragged performance.

Nasdaq 100 (-1.6%) was lower, but large caps (S&P 500 +0.4%), small caps (Solactive 2000 +0.3%) and European equities (+1.2%) gained.

In macro news, data showed the U.S. economy grew at 2.3% (annualized) in Q4 2024. In all, real GDP growth in 2024 came in at 2.8%, which is a full percentage point above economist estimates of 1.7% at the start of the year.

The biggest story in markets this week revolved around the shocking assessment of the DeepSeek release on the AI trade. Sectors levered to AI and its buildout (tech -3.8%, utilities -1.4%, industrials -1.2%) lagged. But what if DeepSeek’s breakthrough is a reason to be even more positive on AI? We provide our take below.

How will DeepSeek impact the AI trade?

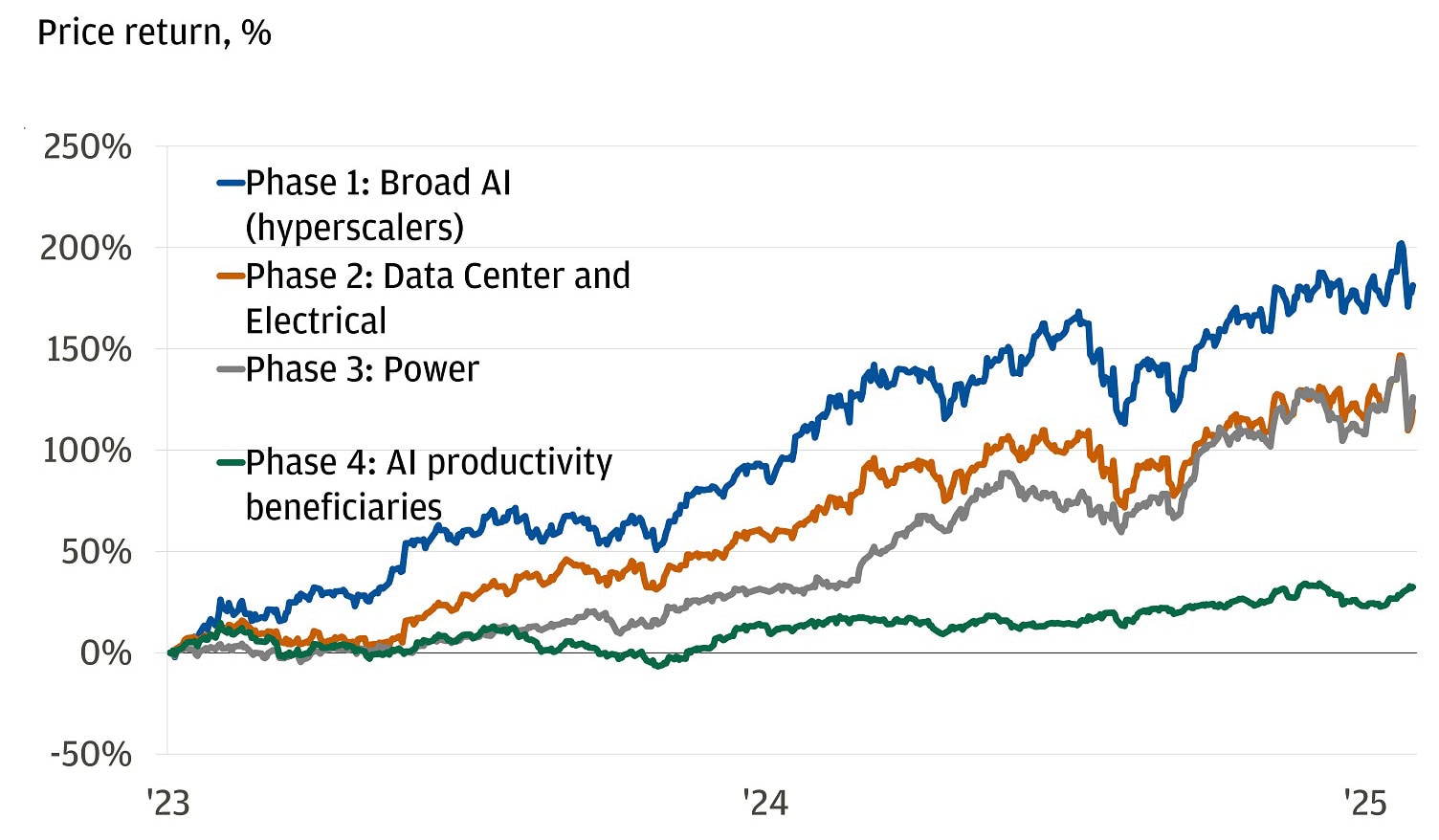

A brief history of the AI trade. Between November 2022 and January 2023, 100 million people started using OpenAI’s ChatGPT. It took Instagram two and a half years to hit the same milestone. Ever since, investors have been captivated by different phases of the AI trade.

- Phase 1 – Hyperscalers: The companies that provide cloud computing technology at scale.

- Phase 2 – Data center compute and infrastructure: The companies that produce inputs like hardware (chips) and electrical equipment that enable data centers.

- Phase 3 – Power and transmission: The companies that supply and transmit the electricity that data centers need.

- Phase 4 – Cross-sector beneficiaries: The companies that incorporate AI to add productivity and reap revenue benefits.

Rotating through the phases of AI

Since the launch of ChatGPT, investors have rewarded companies in phases one through three because hyperscalers have ramped up spending on data center infrastructure and power in the pursuit of AI generated revenue.

Enter DeepSeek, a China-based AI startup founded two years ago. Last Monday (on the eve of President Donald Trump’s inauguration), Deep Seek launched its full R1 model, an open reasoning large language model (LLM). The R1 model matches the performance of o1 (OpenAI’s frontier reasoning LLM) across math, coding and reasoning tasks. Yes, there is still speculation among experts in the industry and financial markets about the validity of DeepSeek’s claims. Regardless, the market believes that their breakthrough challenges the prevailing assumptions that have driven the AI trade.

As a result, AI companies suffered their largest one-day drawdown since the release of ChatGPT on Monday.

- The first assumption challenged is that hyperscalers must spend billions on advanced AI chips. DeepSeek claims that their model used Nvidia’s H800 chips, which have more constrained memory bandwith to comply with U.S. chip export controls than the more advanced H100s. Further, they claim that training took 2,788,000 graphic processing unit (GPU) hours at a cost of $2 per GPU hour. The total cost, therefore, is only $5.576 million for the final training run. The final training run for the latest Llama model from Meta was 10 times the cost. Investors immediately questioned Nvidia’s expected revenue and margins. Indeed, other chipmakers have posted blogs that instruct developers on how to run the DeepSeek model using their own chips. Nvidia lost $590 billion in market cap on Monday and is down -13% this week.

- The second challenged assumption is that AI’s future demands ever-increasing power and energy. DeepSeek’s breakthrough is in part reliant on their design which uses a “Mixture of Experts” (MoE) system (for more details on the technical aspects of the breakthrough, see Michael Cembalest’s latest Eye on the Market). In total, the model has a capacity of 671 billion parameters, but only 37 billion (less than 6%) are active at any given time. This reduces energy requirements along with overall costs. If AI models maintain efficacy without a commensurate increase in compute infrastructure and power, that may mean that data center driven power demand has been overestimated. Hence, many of the companies (e.g. Constellation, Vistra, Eaton and Digital Realty) that had soared based on bullish electricity demand estimates fell sharply on Monday.

- The third assumption questioned is the U.S.’s perceived lead in AI technology. DeepSeek demonstrated that heavy optimization can produce remarkable results on weaker hardware and with lower memory bandwidth. Meanwhile, U.S. labs have been investing heavily in leading edge technology and building an arsenal of the most advanced chips to gain an edge. The playing field is more level than previously assumed. However, DeepSeek used a U.S. model as its technical foundation (Llama), U.S. chips to run the model (Nvidia) and partnered with a U.S. institution to release their findings (MIT).

What does this mean for the AI trade and its adoption lifecycle?

We believe DeepSeek’s model represents a step function advancement in artificial intelligence technology. This is likely a positive for the broad market and the economy even if it marginally shifts value from semiconductors, data center infrastructure and power towards hyperscalers and revenue and productivity beneficiaries over the medium term. That is because more efficient models could further commoditize AI and exert downward pressure on capital spending and energy requirements.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

At the same time, less expensive models should drive adoption and demand from households and corporations. A key question remains: Will increased adoption offset reduced capital spending from cost and energy efficiencies?

Here’s how we would assess the state of the AI trade:

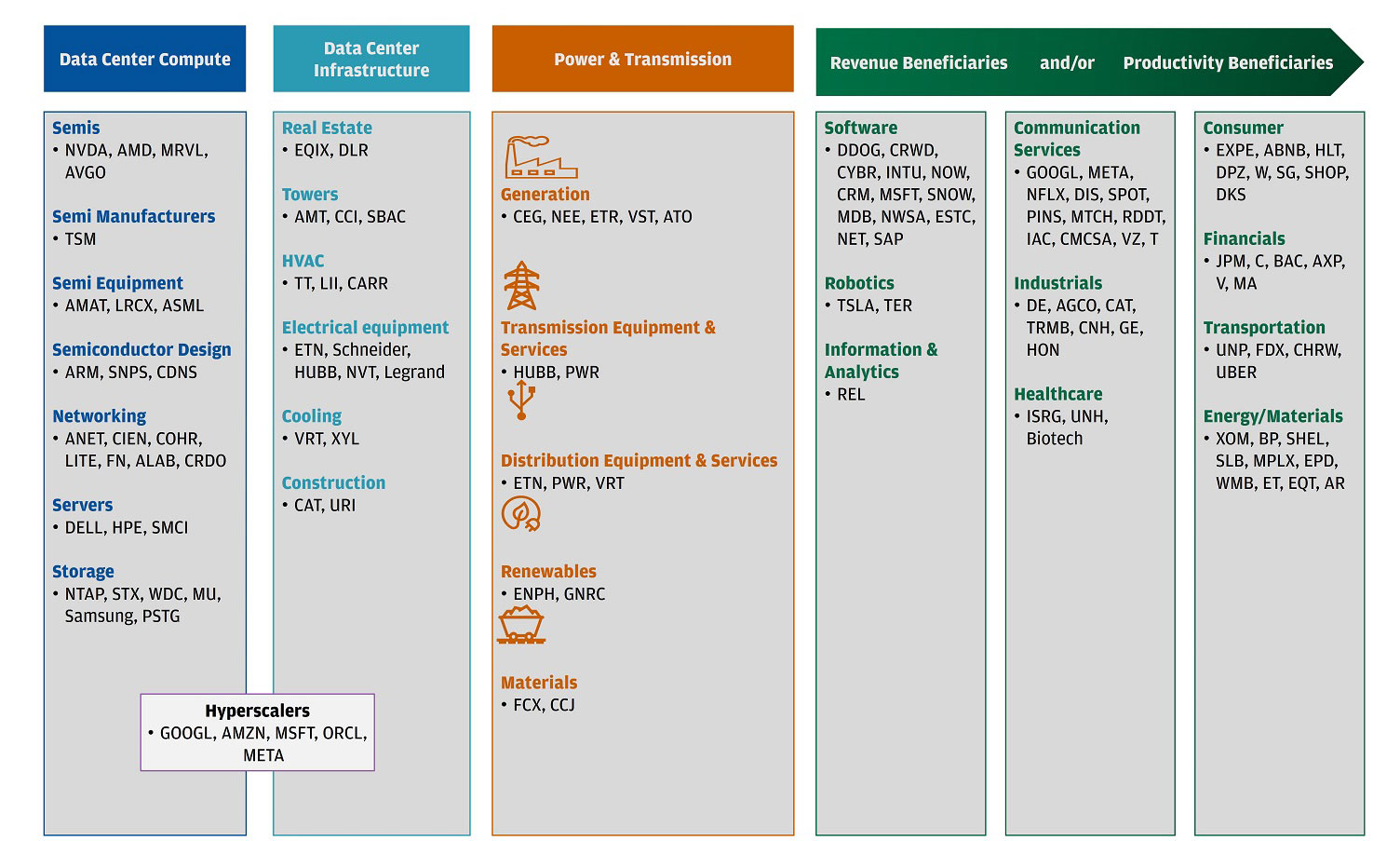

The state of the AI trade with illustrative examples

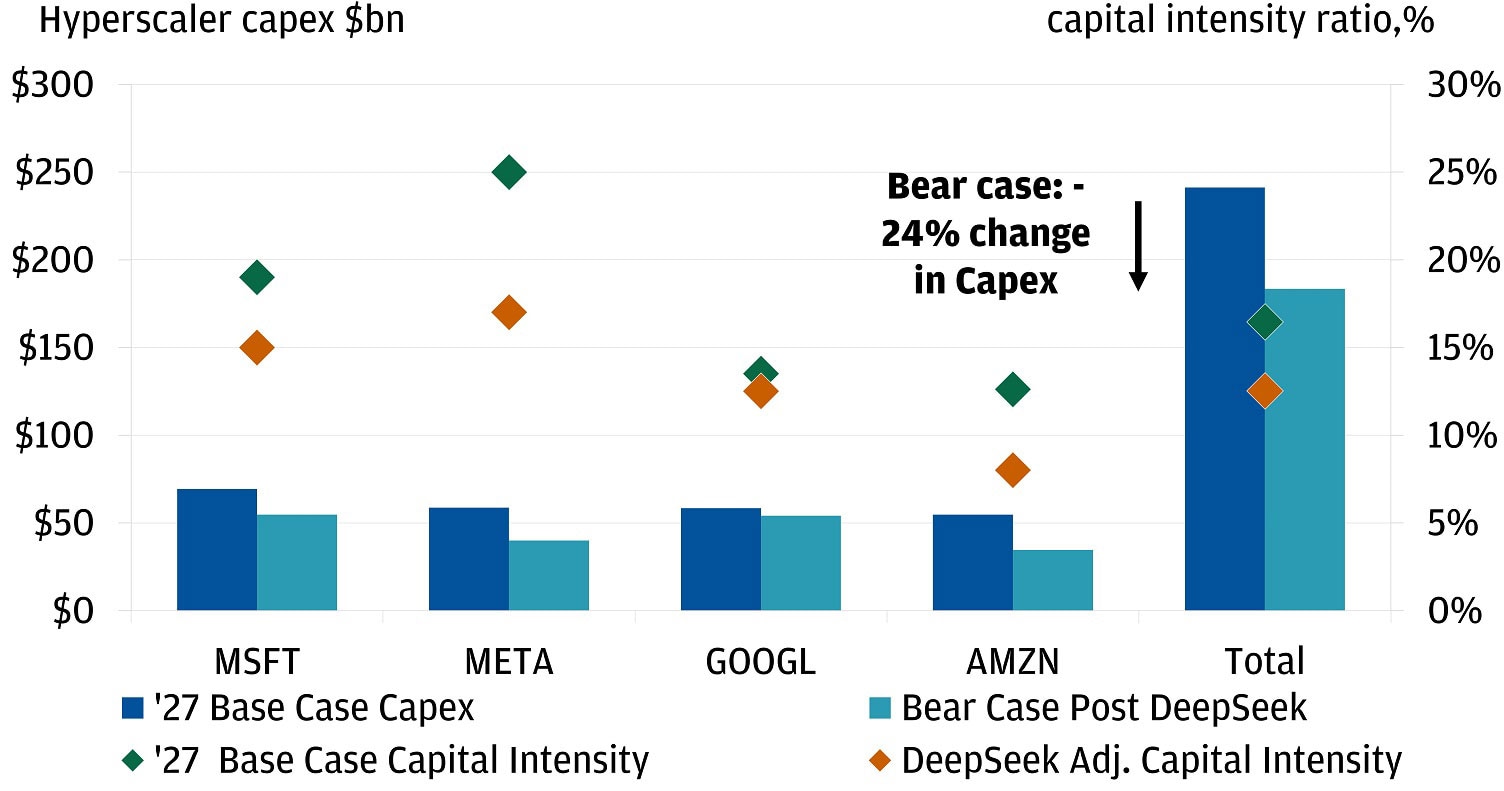

Phase 1 – Hyperscalers: Let’s assume the hyperscalers slash capital spending plans due to cost and energy efficiencies. In a bear case scenario, capital spending intensity (Capex/revenue) by hyperscalers could decrease back to 2015 to 2019 levels. This could lead to a decrease of nearly 24% in capex spend by these companies. This would clearly be a negative for the revenue of data center compute and infrastructure companies, but it could be a positive for hyperscaler stocks. Indeed, less capital spending frees up cash flow to return to shareholders, especially if you assume that AI innovations continues apace. However, this is not our base case.

Worst case scenario, we could see hyperscaler capex decrease by ~24% in 2027

This week, Microsoft and Meta reported earnings and confirmed continued spending intentions, primarily focused on building data centers for inference rather than training, aligning with the view that most AI investments are needed for inference. That said, as spending shifts towards Application Specific Integrated Circuits (ASICs), which combine hyperscalers’ intellectual property with a design platform, the traditional reliance on GPUs is expected to decrease.

Phase 2 – Data center compute and infrastructure: Decreased spending from hyperscalers could mean lower revenues for data center players. Analysts estimate data center revenues for chipmakers to grow 27% by 2028. We estimate that roughly 37.5 billion of that revenue is at risk amid shifting capex plans. That could translate to a decrease of almost seven percentage points for chipmaker data center revenues by 2028. However, as cost comes down, use cases could increase (elasticity), continuing to boost power demand. In fact, our investment bank noted that x86 virtualization (a technology developed in the mid-2000s that enabled multiple operating systems to run on a single physical machine) increased efficiency but also stimulated demand for semiconductor chips and memory. The transition to cloud computing likewise improved efficiency and drove demand for semiconductors.

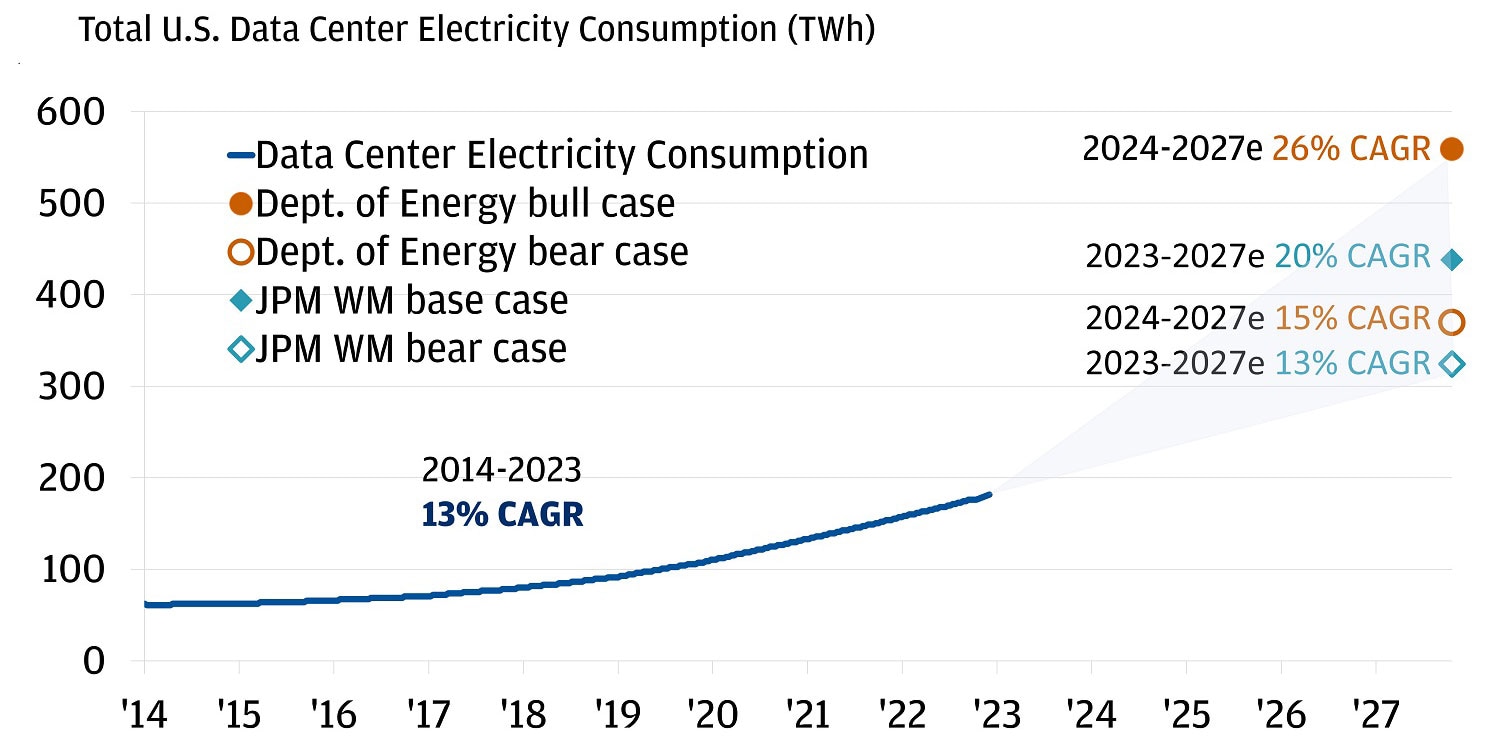

Phase 3 – Power and transmission: In 2023, electricity demand in the United States was approximately 4,200 Terawatt Hour (Twh), with data centers accounting for about 200 Twh. Earlier this year, the Department of Energy (DoE) released updated projections for data center electricity demand. The high end of the estimate assumed that AI workloads would drive a 26% compound annual growth rate (CAGR) over the next few years. At that rate, data center electricity demand would double roughly every 2.5 years. Our downside case is even more restrained than the DoE’s. If DeepSeek efficiencies lead to little incremental growth, we believe that data center electricity demand would return to the growth rate of 13% experienced from 2014 to 2023.

Our view is slightly more upbeat. We believe that data center electricity demand will grow at a 20% CAGR over that time horizon. Further, AI is not the only factor driving power demand. Indeed, we believe that electric vehicles and hybrids, industrialization and automation, and non-AI data centers will also contribute to a 2.5% CAGR in overall electricity demand growth over the next several years versus the paltry 0.7% CAGR witnessed over the last decade. This wide range in possible outcomes should lead to more volatility in this theme that tactical traders could use to their advantage. Even if the highest estimates of power demand seem less likely, we still believe that power is an investable trend.

There is a wide range of datacenters power estimates

Phase 4 – Cross-sector beneficiaries: Ultimately, the DeepSeek breakthrough may be most positive for the many potential productivity and revenue beneficiaries of AI technology that inhabit most sectors in the stock market. We see this reflected in the price action. Since Monday, the productivity beneficiaries have outperformed stage one to three companies by 7% on average. The software sector was a notable outperformer and we would expect that to continue.

We have embraced the AI trade, both in portfolios and within J.P. Morgan. We think the theme could drive outperformance over the next several years, but we would also advocate accessing the theme selectively through active management in both the public and private space while maintaining exposures that help ensure portfolio resilience.

For questions on how to implement these strategies effectively, reach out to your J.P. Morgan advisor.

All market and economic data as of 01/31/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

J.P. Morgan Wealth Management