War and peace: What to know about global security

J.P. Morgan Wealth Management

Market Update

U.S. large cap equities are still on pace to finish the week higher despite yesterday’s pullback.

The S&P 500 is higher by +0.1% this week, but the tech-oriented Nasdaq 100 (-0.2%) and small caps (-1.1%) are facing losses. European equities (Stoxx 50 -0.1%) are lagging their U.S. counterparts this week ahead of German general elections and Chinese equities (Hang Seng +3.8%) are heading towards their sixth week in a row of gains.

Investors are taking Walmart’s concerns regarding the uncertainty of consumer behavior as a warning sign. Consumers have been dealing with inflation and elevated borrowing costs and last month’s weaker-than-expected retail sales print is raising questions for the cohort.

Uncertainty has stretched beyond just the consumer this year. To name a few others, advancements in artificial intelligence (AI) challenged the status quo in the field, tariff threats are edging countries closer to trade wars and negotiations aimed at ending the war in Ukraine have highlighted Europe’s need for defense. We discuss the latter in today’s note below.

Global defense implications

This past week featured a flurry of geopolitical headlines which included negotiations between the U.S. and Russia regarding the war in Ukraine. While there is still a tremendous amount of uncertainty, it does seem clear that Europe may bear the price of any peace deal.

Both Vice President JD Vance and Defense Secretary Pete Hegseth suggested at the Munich conference last week that Europe should not rely on the U.S. for security, and President Donald Trump has expressed opposition to deploying U.S. troops as part of any security package for Kyiv. European leaders seem to be getting the message.

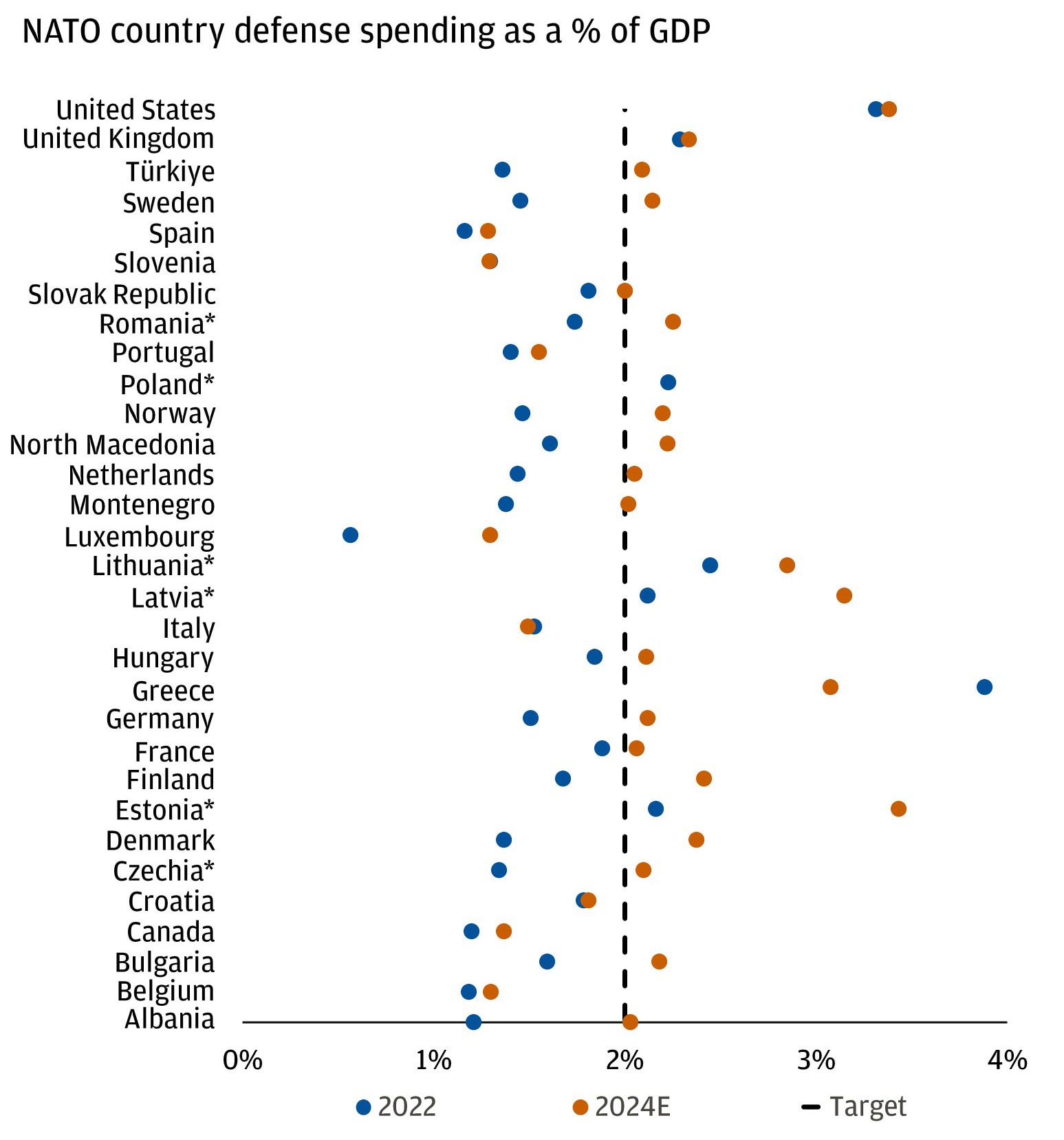

Europe has underinvested in defense (the cumulative gap between actual defense spending and the NATO target of 2% of gross domestic product) by approximately 1.8 trillion euros between 1990 and 2021. Notably, around one-third of this shortfall is solely due to Germany, which implemented more significant reductions in defense spending following the conclusion of the Cold War than any other major Western country.

European NATO members have attempted to close this gap and have been ramping up defense budgets, as highlighted in our 2025 Outlook: Building on Strength. Estimates suggest that 71% of NATO members will meet the 2% GDP defense spending target by 2024, up from just 22% in 2022.

NATO countries have been increasing their defense spending

But it seems likely that spending can ramp up further. A Bloomberg article suggested the ultimate price of peace for the EU could be over $3.1 trillion over the next decade. This situation reveals existing fractures within the EU and they face a critical decision: Act collectively with geopolitical influence or prioritize national interests as they navigate the complex dynamics of the Ukraine conflict and their relationship with the U.S.

Investors will get a gauge of how the German voters feel about the situation this weekend during the country’s general election. A key policy priority at stake in the election includes reforming the “debt brake,” which limits Germany’s budget deficit to 0.35% of its GDP. Reforming the debt brake could be critical to enable necessary defense spending. Parties in favor of reform only make up 40% of the current polls, but there could be scope for negotiations given the importance of defense spending.

Work with an advisor

Our advisors can provide ongoing financial advice on how your portfolio can adapt to the changes in the market, your life and your goals.

Election results aside, we anticipate that recent developments in Europe and on their borders will lead to increased investment in security across the region.

What it means for traditional defense: Global armed conflict is at an 80-year high and global trade uncertainty is at its highest level since the Covid-19 pandemic, necessitating resource allocation to traditional defense. In Europe, spending on defense could potentially rise to between 2.5% and 3% of GDP spending, which would likely support domestically produced defense systems and the European industrials sector.

In the U.S., GOP Chairman of the House Armed Services Committee, Mike Rogers, and Senate Armed Services Committee counterpart, Roger Wicker, requested significant defense spending increases. They foresee defense spending reaching 4% of U.S. GDP, up from roughly 3.2% in 2024. Outgoing Defense Secretary Lloyd Austin also proposed higher spending, with a $50 billion increase in 2026 and over $1 trillion by 2028. Given bipartisan support and the increasing global importance of security, defense spending in the U.S. is likely to gain approval, although current Defense Secretary Hegseth’s desire to cut spending at the Pentagon is at odds with the trend.

Security spending will likely extend beyond traditional military expenditures to include securing supply chains, especially for energy resources. Before the Ukraine war, Russia supplied the EU with 21 billion cubic meters of liquefied natural gas (LNG) and 40 billion cubic meters of natural gas through Ukrainian pipelines. That contract ended last year, halting pipeline flows.

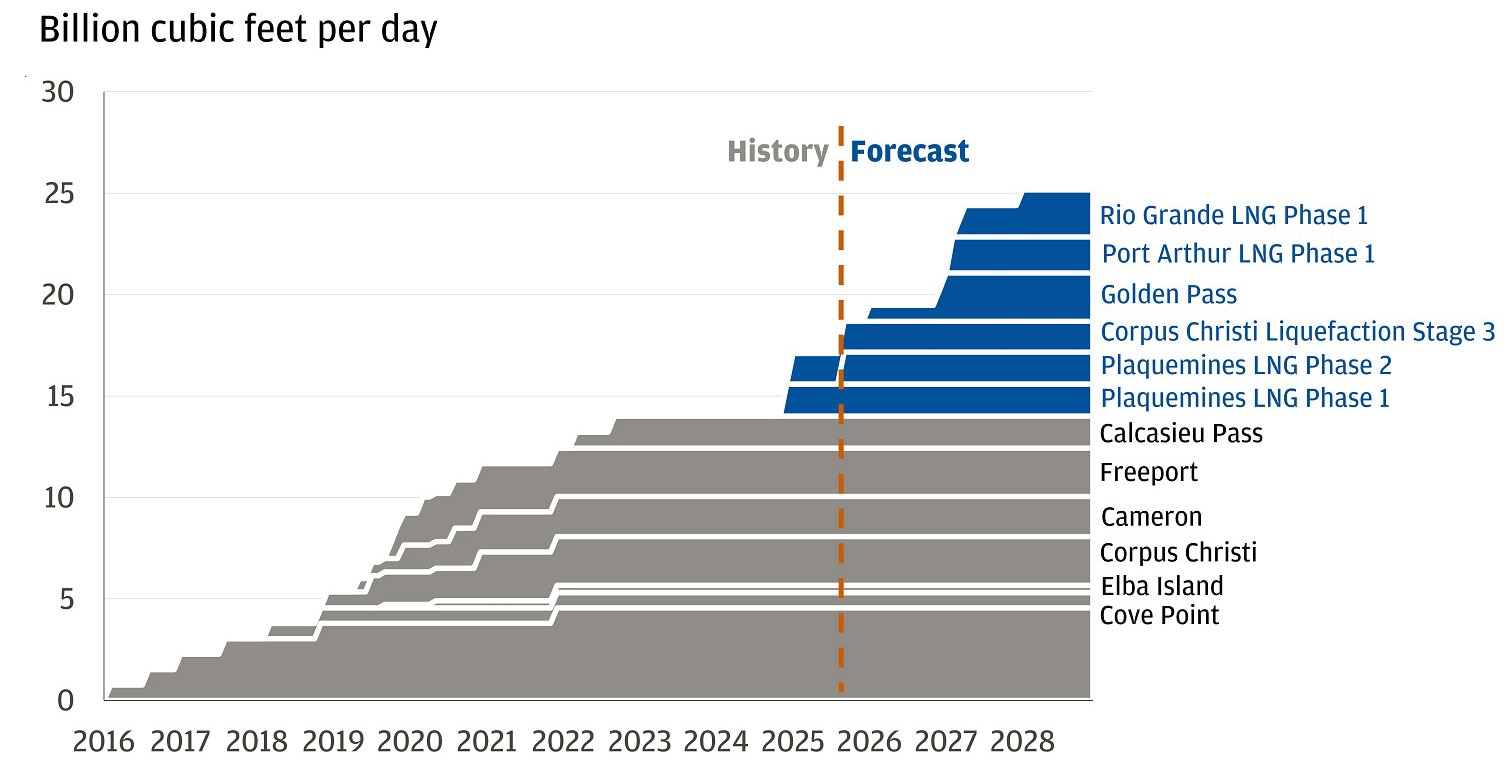

The outstanding question is how reliant Europeans will want to be on Russian natural gas if the war ends. Before the war, Russian energy accounted for 35% of the region’s energy imports. We believe the EU would likely cap this at 20%. The region has increased its LNG regasification capacity by 75 billion cubic meters since the war’s outbreak, while North American export capacity is set to double by 2028. European investment in domestic energy production should continue, but energy independence is unlikely in the near term. Thus, Europe will be focused on diversifying its sources of energy and could even go back to buying Russian gas.

North America liquefied natural gas exports expected to double by 2028

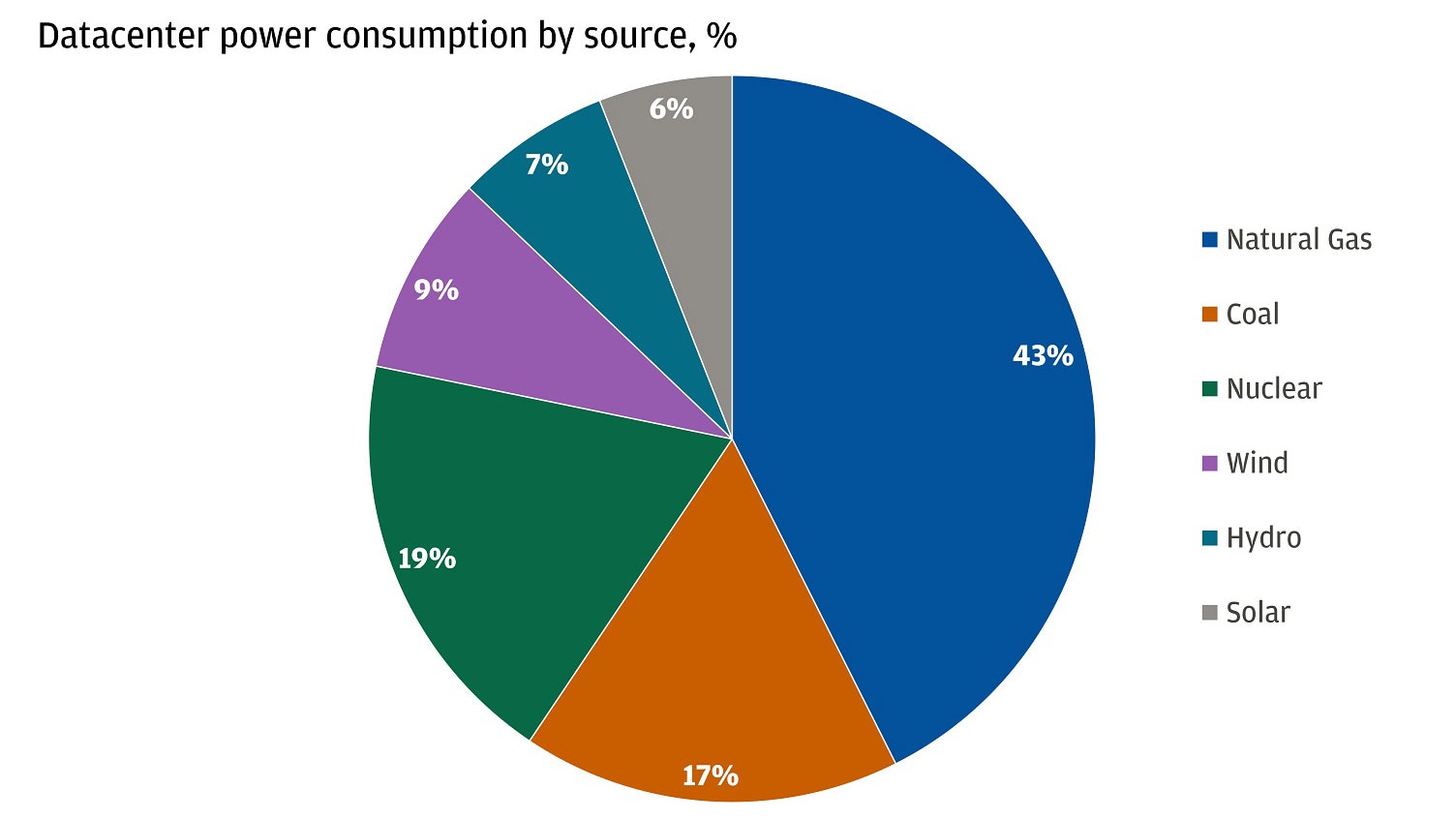

The U.S. is much more energy independent than Europe, but there is a clear need to close the energy gap to support the AI buildout. Our Chairman of Asset and Wealth Management, Michael Cembalest, noted in his outlook that hyperscalers will likely continue to rely on natural gas for power.

Natural gas accounts for over 40% of data center power consumption

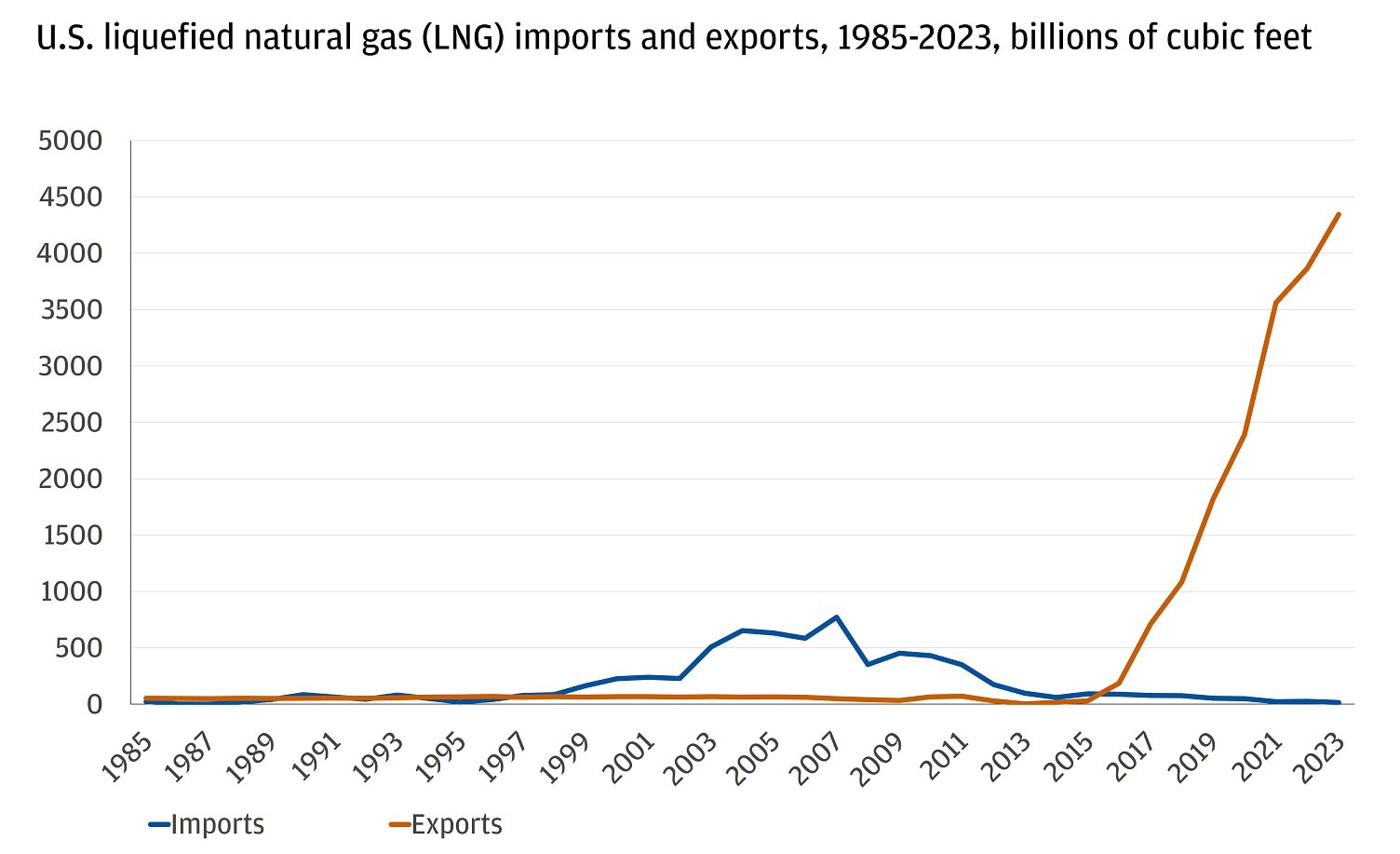

Nuclear projects are years away from providing incremental power and renewable energy (wind and solar) may lose subsidies under the current administration. However, U.S. natural gas production continues to grow and the U.S. has surpassed Qatar and Australia as the top LNG exporter in 2023. By 2030, the U.S. is projected to remain the top exporter, exceeding others by roughly 40%.

The U.S. has become a major exporter of LNG

What does that mean for portfolios? A continued impulse to spend on security supports select companies across the industrials, materials, energy and utilities sectors in the U.S. and Europe. Private infrastructure assets will also likely remain well supported given existing power demand gaps and a need to diversify energy sources.

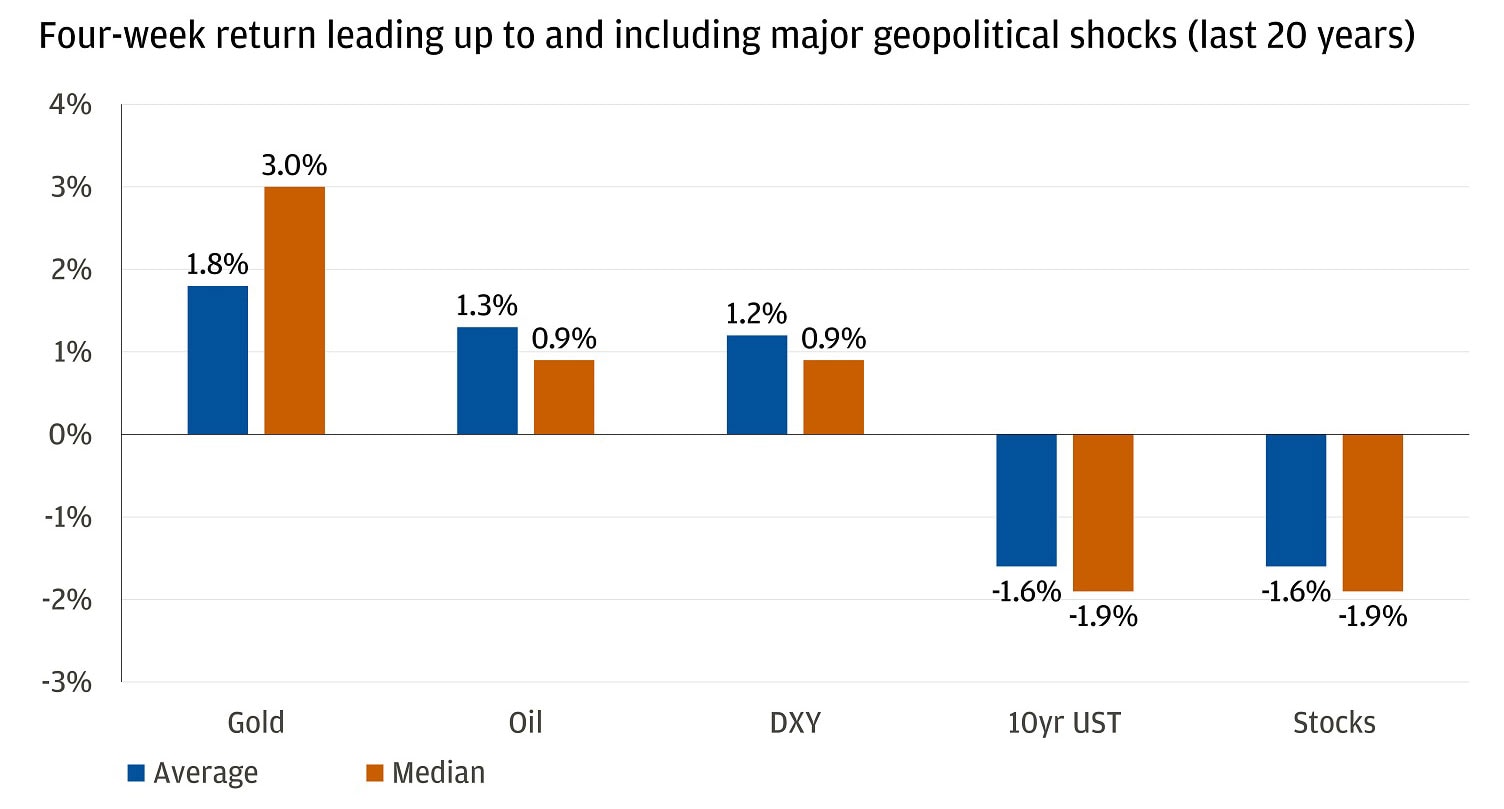

Our preferred hedge against increased geopolitical uncertainty is gold.

Gold is a top performer as a tactical portfolio hedge against geopolitical risk

We favor gold due to its limited supply (Current estimates, including underground reserves, total 244,040 tons of gold, enough to fill just over three Olympic-sized swimming pools) and continued demand from central banks (according to a 2024 survey by the World Gold Council, 81% of central banks plan to increase gold allocations over the next 12 months, with none planning to decrease).

Looking to lean into the increased security spend across traditional defense, infrastructure and energy? Reach out to your J.P. Morgan advisor to see how these sectors can best fit into your portfolio.

All market and economic data as of 02/21/25 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

Explore ways to invest

Take control of your finances with $0 commission online trades, intuitive investing tools and a range of advisor services.

J.P. Morgan Wealth Management